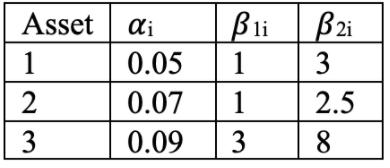

It is believed that three assets, A1, A2 and A3 are following a two-factor model. the model

Fantastic news! We've Found the answer you've been seeking!

Question:

It is believed that three assets, A1, A2 and A3 are following a two-factor model. the model parameters are estimated as follows

Assume E[f] = e1 = e2 = e3 = 0

Construct a zero-beta portfolio from these risky assets. What is the weighting of A1, A2 and A3 in this portfolio?

Expert Answer:

Related Book For

Mathematical Statistics with Applications in R

ISBN: 978-0124171138

2nd edition

Authors: Chris P. Tsokos, K.M. Ramachandran

Posted Date: