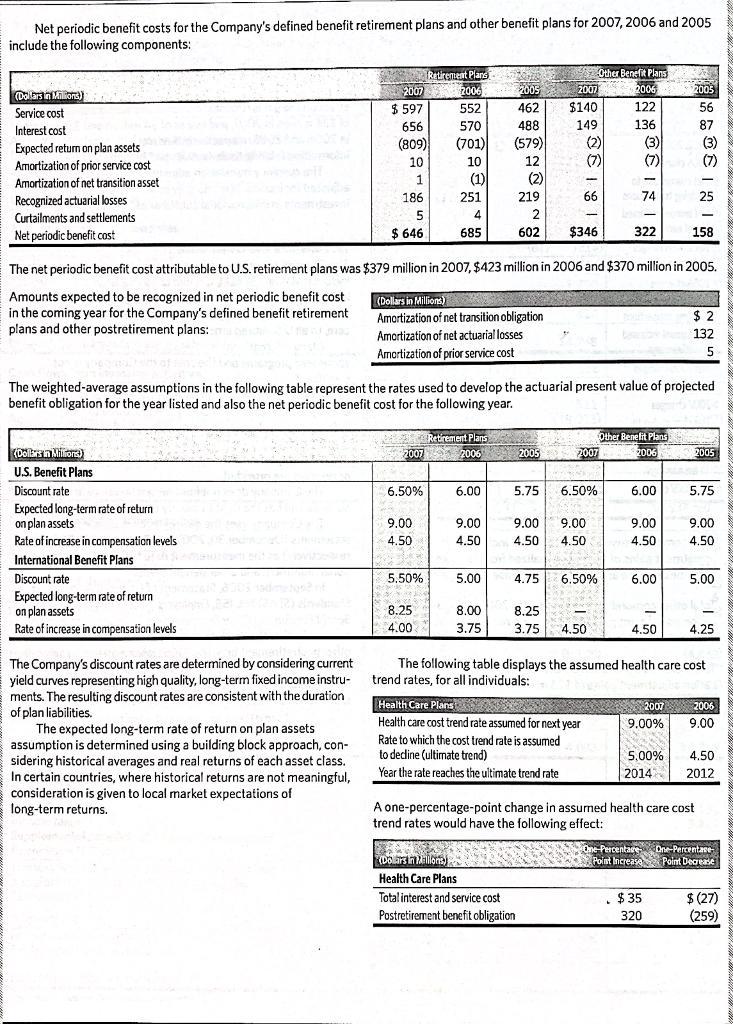

L. Calculate the combined retirement and other benefits expense over the past three years. (See page 61).

Fantastic news! We've Found the answer you've been seeking!

Question:

L. Calculate the combined retirement and other benefits expense over the past three years. (See page 61).

i. What general trend do you notice? Do you consider this trend persistent? That is, do you expect it to continue?

ii. Retirement and other benefits expense includes an operating component and a non-operating component. Calculate both components for each of the three years. What trends do you notice in the components? Do you consider these trends persistent?

Expert Answer:

i The combined retirement and other benefits expense over the past three years has increased from 2049 million in 2017 to 2233 million in 2018 and the... View the full answer

Related Book For

Human Resource Management

ISBN: 978-0078029127

12th edition

Authors: John Ivancevich, Robert Konopaske

Posted Date: