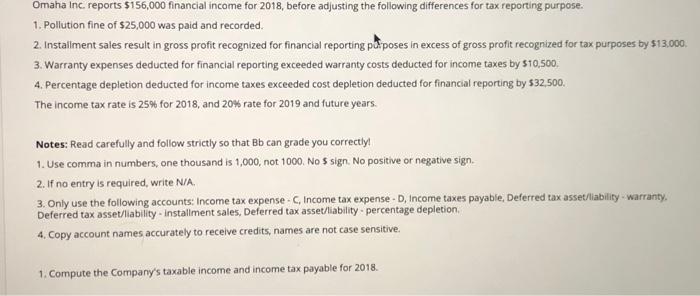

Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

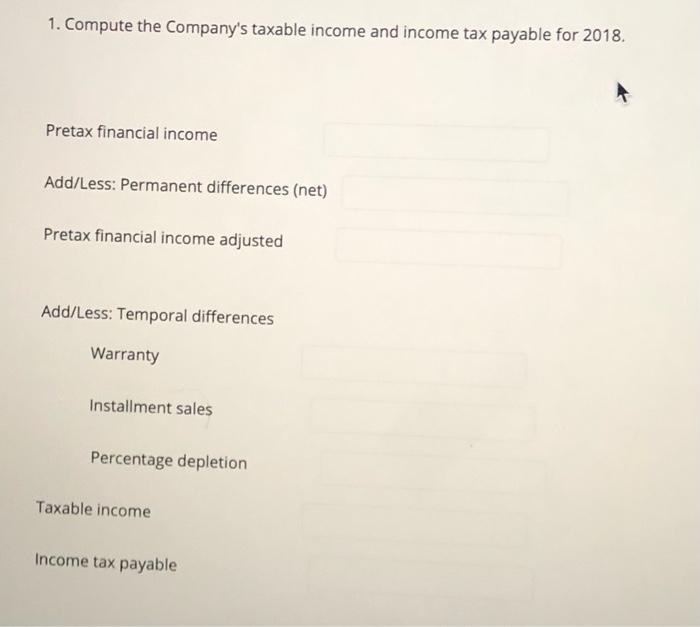

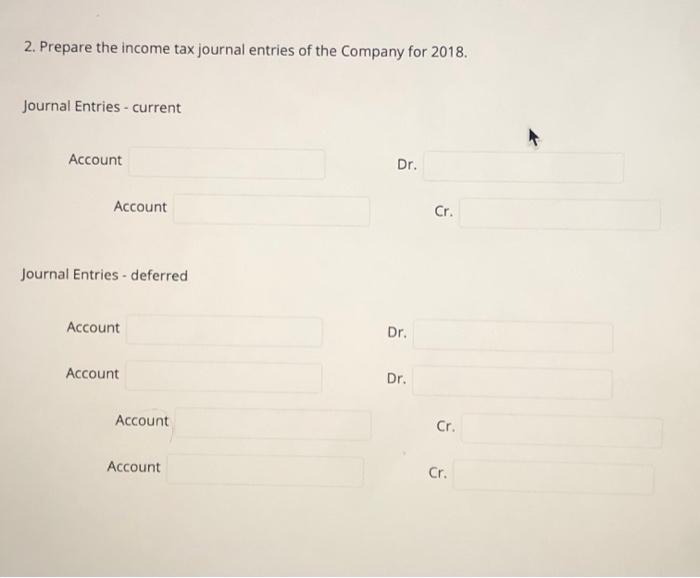

Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr. Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr. Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr. Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr. Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr. Omaha Inc. reports $156,000 financial income for 2018, before adjusting the following differences for tax reporting purpose. 1. Pollution fine of $25,000 was paid and recorded. 2. Instalment sales result in gross profit recognized for financial reporting parposes in excess of gross profit recognized for tax purposes by $13.000. 3. Warranty expenses deducted for financial reporting exceeded warranty costs deducted for income taxes by $10,500. 4. Percentage depletion deducted for income taxes exceeded cost depletion deducted for financial reporting by $32,500. The income tax rate is 25% for 2018, and 20% rate for 2019 and future years. Notes: Read carefully and follow strictly so that Bb can grade you correctly! 1. Use comma in numbers, one thousand is 1,000, not 1000. No $ sign. No positive or negative sign. 2. If no entry is required, write N/A. 3. Only use the following accounts: Income tax expense - C, Income tax expense - D, Income taxes payable, Deferred tax asset/liability warranty. Deferred tax asset/liability - installment sales, Deferred tax asset/liability - percentage depletion. 4. Copy account names accurately to receive credits, names are not case sensitive. 1. Compute the Company's taxable income and income tax payable for 2018. 1. Compute the Company's taxable income and income tax payable for 2018. Pretax financial income Add/Less: Permanent differences (net) Pretax financial income adjusted Add/Less: Temporal differences Warranty Installment sales Percentage depletion Taxable income Income tax payable 2. Prepare the income tax journal entries of the Company for 2018. Journal Entries - current Account Dr. Account Cr. Journal Entries - deferred Account Dr. Account Dr. Account Cr. Account Cr.

Expert Answer:

Answer rating: 100% (QA)

Answer1 Calculation of Companys Taxable Income and Income tax Payab... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0077400163

6th edition

Authors: J. David Spiceland, James Sepe, Mark Nelson

Posted Date:

Students also viewed these accounting questions

-

1.1. 1.2. 1.3. 1.4. Consider the following four bonds given in the table below, where coupons are paid out once per year: Bond A B C D Maturity 1 2 3 4 Coupon Rate 1% 5% 0% 10% Price, $ 926.6055...

-

Account No Account Titles Dr Cr Dr Cr 101Cash8840 112Accounts Receivable10989 130Prepaid Insurance2828 157Equipment23599 167Accumulated DepreciationEquip4394 201Accounts Payable9150 212Salaries and...

-

Taxable income and pretax financial income would be identical for Huber Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income...

-

Determine the range of the 2x function y = 3 sec 3

-

a) Prove that if k=1 ak converges, then its partial sums sn are bounded. b) Show that the converse of part a) is false. Namely, show that a series k=1 ak may have bounded partial sums and still...

-

In Exercises 1 through 16, use the method of Lagrange multipliers to find the indicated extremum. You may assume the extremum exists. Let f(x, y, z) = x + 2y + 3z. Find the maximum and minimum values...

-

Which form of financing requires repayment, regardless of whether the company receiving the funds does well or not? a. A loan b. An investment c. Both a loan and an investment d. Neither a loan nor...

-

Review this chapters opening feature involving Arynetta Floyzelle and her Girl Team Mobile business. 1. Explain how a classified balance sheet can help Arynetta Floyzelle know what bills are due when...

-

Company X planned normal operation level ( 1 0 , 0 0 0 h ) sales revenues and costs for the 3 rd quarter of 2 0 2 3 are as follows: Total | Product 1 | Product 2 Sales Revenues | 4 0 0 , 0 0 0 | ...

-

In spring 2021, Amir Nathoo was at the helm of one of the most talked-about startups in the massive and fragmented educational technology (EdTech) industry. Just six years earlier, Nathoo and his...

-

Which of the following statements are TRUE? Multiple answers:Multiple answers are accepted for this question PLEASE SHOW WORK FOR EACH PART AND EXPLAIN WHY EACH ANSWER CHOICE IS WRONG OR RIGHT a The...

-

What is your leadership plan? When and which responsibilities will you delegate? How will you promote people in your organization? When might you need to go outside to hire?

-

What kind of controls can you establish early in your ventures life? How will these help you manage cash and other key components of your business?

-

What are your organizations key resources and capabilities? What should they be in the future? How do you build toward those resources and capabilities?

-

Construct a data file about the purchasing behavior of four customers, described below, who visit a shopping mall. Enter the purchase amounts each spent on clothes, sporting goods, books, and food....

-

Identify each of the following variables as nominal, ordinal, or neither. a. Gender (with categories female, male, nonbinary, other) b. Favorite color c. Pain as measured on the 11-point pain scale,...

-

What is the eumber of ights needed to purchafe one thinevsshare? Venture Berhad plans to raise RM20 million from a rights issue to fund a new business expansion. The company will issue 8 million new...

-

Explain how the graph of each function can be obtained from the graph of y = 1/x or y = 1/x 2 . Then graph f and give the (a) Domain (b) Range. Determine the largest open intervals of the domain over...

-

Sometimes a temporary difference will produce future deductible amounts. Explain what is meant by future deductible amounts. Describe two general situations that have this effect. How are such...

-

I thought I understood earnings per share, lamented Brad Dawson, but you're telling me we need to pretend our convertible bonds have been converted! Or maybe not? Dawson, your boss, is the new...

-

Kandon Enterprises, Inc. has two operating divisions; one manufactures machinery and the other breeds and sells horses. Both divisions are considered separate components as defined by generally...

-

Consider an experiment that selects a cell phone camera and records the recycle time of a flash (the time taken to ready the camera for another flash). The possible values for this time depend on the...

-

Suppose that the recycle times of two cameras are recorded. The extension of the positive real line \(R\) is to take the sample space to be the positive quadrant of the plane \[ S=R^{+} \times R^{+}...

-

Consider the sample space \(S=\{y y, y n, n y, n n\}\) in Example 2.2. Suppose that the subset of outcomes for which at least one camera conforms is denoted as \(E_{1}\). Then, \[ E_{1}=\{y y, y n, n...

Study smarter with the SolutionInn App