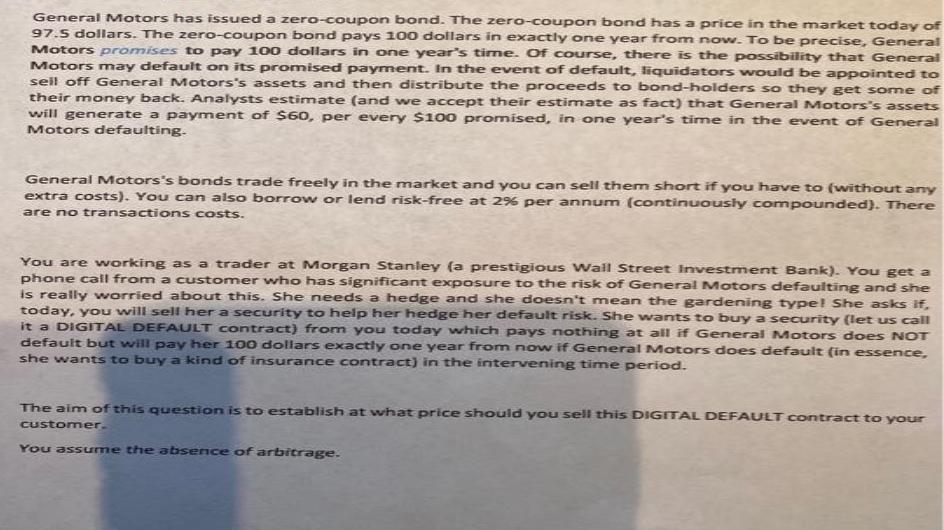

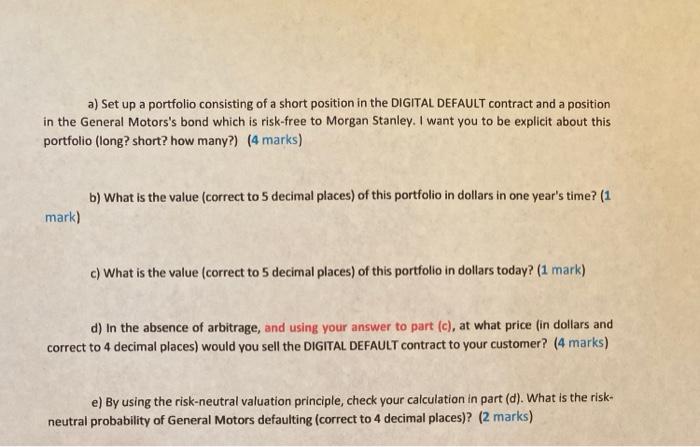

General Motors has isued a zero-coupon bond. The zero-coupon bond has a price in the market...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a From the question we must determine the probability of default However we are not provided with so ... View the full answer

Related Book For

Auditing a business risk appraoch

ISBN: 978-0324375589

6th Edition

Authors: larry e. rittenberg, bradley j. schwieger, karla m. johnston

Posted Date: