Nciba CC is a business entity founded and registered as a close corporation by the two...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

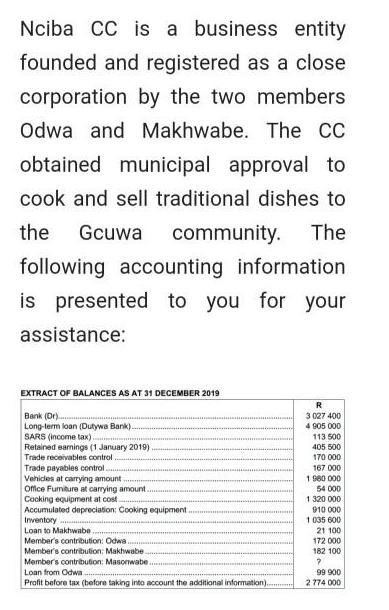

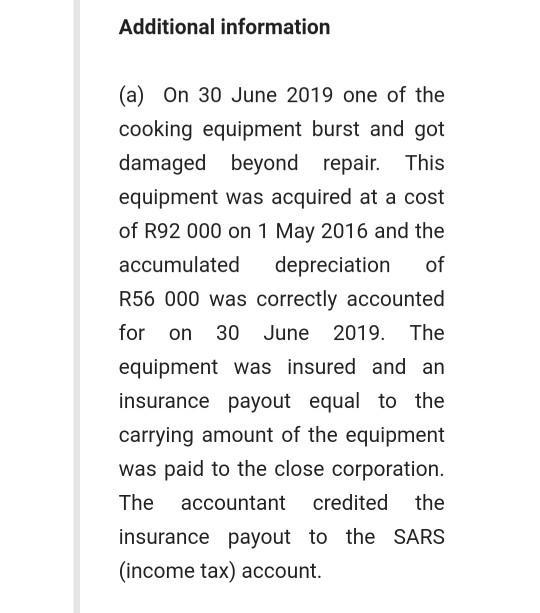

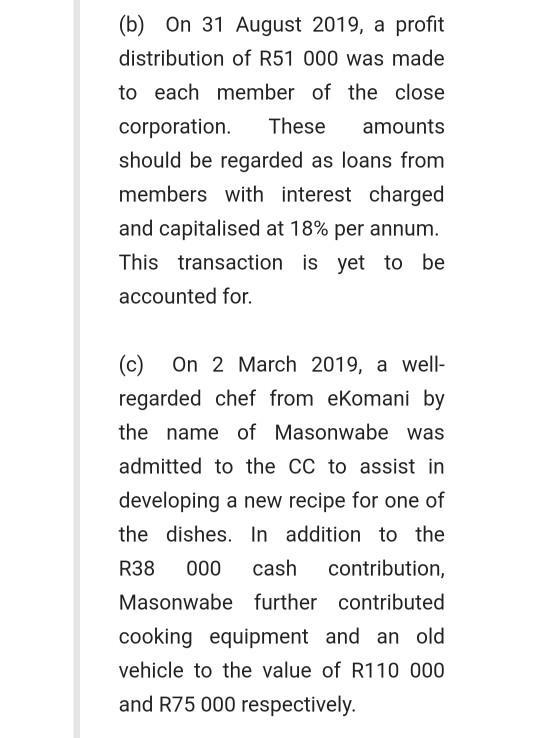

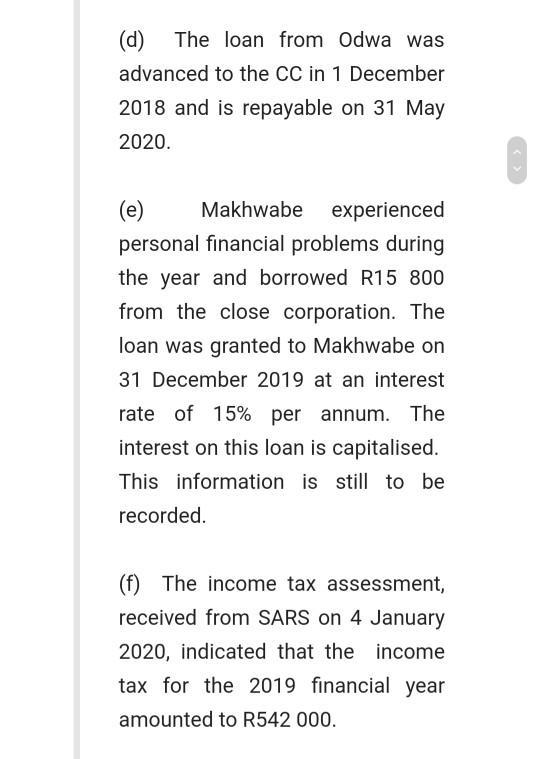

Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900 Nciba CC is a business entity founded and registered as a close corporation by the two members Odwa and Makhwabe. The CC obtained municipal approval to cook and sell traditional dishes to the Gcuwa community. The following accounting information is presented to you for your assistance: EXTRACT OF BALANCES AS AT 31 DECEMBER 2019 Bank (Dr) Long-term loan (Dutywa Bank). SARS (income tax). Retained earnings (1 January 2019) Trade receivables control. Trade payables control.. Vehicles at carrying amount. Office Fumiture at carrying amount Cooking equipment at cost. Accumulated depreciation: Cooking equipment Inventory Loan to Makhwabe.. Member's contribution: Odwa Member's contribution: Makhwabe. Member's contribution: Masonwabe. Loan from Odwa Profit before tax (before taking into account the additional information). R 3027 400 4 905 000 113 500 405 500 170 000 167 000 1 980 000 54 000 1 320 000 910 000 1 035 600 21 100 172 000 182 100 ? 99 900 2 774 000 Additional information (a) On 30 June 2019 one of the cooking equipment burst and got damaged beyond repair. This equipment was acquired at a cost of R92 000 on 1 May 2016 and the accumulated depreciation of R56 000 was correctly accounted for on 30 June 2019. The equipment was insured and an insurance payout equal to the carrying amount of the equipment was paid to the close corporation. The accountant credited the insurance payout to the SARS (income tax) account. (b) On 31 August 2019, a profit distribution of R51 000 was made to each member of the close corporation. These amounts should be regarded as loans from members with interest charged and capitalised at 18% per annum. This transaction is yet to be accounted for. (c) On 2 March 2019, a well- regarded chef from eKomani by the name of Masonwabe was admitted to the CC to assist in developing a new recipe for one of the dishes. In addition to the R38 000 cash contribution, Masonwabe further contributed cooking equipment and an old vehicle to the value of R110 000 and R75 000 respectively. (d) The loan from Odwa was advanced to the CC in 1 December 2018 and is repayable on 31 May 2020. (e) Makhwabe experienced personal financial problems during the year and borrowed R15 800 from the close corporation. The loan was granted to Makhwabe on 31 December 2019 at an interest rate of 15% per annum. The interest on this loan is capitalised. This information is still to be recorded. (f) The income tax assessment, received from SARS on 4 January 2020, indicated that the income tax for the 2019 financial year amounted to R542 000. QUESTION 7 Which one of the following alternatives represents the correct loans from members to be presented in the statement of changes in net investments of members of Nciba CC for the year ended 31 December 2019? A. R 262 080 B. R 99 900 C. R 162 180 D. R 257 600 E. R 252 900

Expert Answer:

Answer rating: 100% (QA)

The detailed answer for the above question is provided below Answer A R 26... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these finance questions

-

Cyclops Company manufactures kinetic torches. Based on market research, Cyclops decides on a target cost of $3.5 for its "Omega Red" model. They expect to sell 15000 units of Omega Reds in the next...

-

The following information relates to Loveland Company: Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $600,000 Cost of...

-

Show how the following mass motion equation is derived, and then solve for displacement. www. Mass-spring-damper system The mass motion is described by the differential equation: where: x + 2z. k =...

-

The combined sewer system in city ABC is comprised of two parallel interceptors referred to as "North" and "South" lines. The southern line is connected to a newly built wastewater treatment plant....

-

An inventor claims to have built a device that will take 0.001 kg/s of water from the faucet at 10C, 100 kPa, and produce separate streams of hydrogen and oxygen gas, each at 400 K, 175 kPa. It is...

-

If an interest rate is currently 6% and a lending institution announces a 25 basis point increase, what percentage increase does this represent?

-

Explain the main features of volute type and vortex type centrifugal pumps.

-

1. Create a service blueprint of the refinancing process. Why do you think the bank organized its process this way? What problems have ensued? 2. Examine the process carefully. Look at customer/...

-

1. Analyze and explain the theoretical concepts related to the balance of payments of a country. A country has exports of $20 billion, imports of $25 billion, net transfers from abroad of $1 billion,...

-

What characterizes someone who views shopping as a form of entertainment (Tables 1B through 7B)? Which factors contribute most? How do your findings relate to the information presented in Consumer...

-

The paint and coatings industry in Australia contributes approx. $3.2 billion in revenue and employ over 6,505 people according to IBIS World. Just like other industries, COVID-19 has had an impact...

-

A thin disk of radius \(R\) carries a uniformly distributed charge. The surface charge density on the disk is \(\sigma\). What is the electric field at a point \(\mathrm{P}\) along the perpendicular...

-

In 2001, the Fed pursued an expansionary monetary policy and reduced interest rates. At the same time, President George W. Bush pushed through legislation that lowered income taxes. a. Illustrate the...

-

Particle A carrying a \(4.0-\mu \mathrm{C}\) charge is located at \(y=3.0 \mathrm{~m}\) on the \(y\) axis of an \(x y\) coordinate system, and particle B carrying a \(6.0-\mu \mathrm{C}\) charge is...

-

Sustainability a. cannot be achieved without dropping our standard of living. b. strives to improve our quality of life but also protect the earth. c. is achieved when a company practices ethical...

-

A thin rod of length \(\ell\) carries a uniformly distributed charge \(q\). What is the electric field at a point \(\mathrm{P}\) along a line that is perpendicular to the long axis of the rod and...

-

An inlined function is a function augmented with the keyword inline. The keyword inline is a directive to the compiler to insert the function's code body in place of any call to the function. An...

-

Borrowing costs should be recognised as an expense and charged to the profit and loss account of the period in which they are incurred : A. If the borrowing costs relate to qualifying asset B. If the...

-

Summer plc acquired 60% of the common shares of Winter Ltd on 30 September 20X1 and gained control. At the date of acquisition, the balance of retained earnings of Winter was 35,000. At 31 December...

-

Forest plc acquired 80% of the ordinary shares of Bulwell plc some years ago. At acquisition, the fair values of the assets of Bulwell plc were the same as their carrying value. Bulwell plc...

-

The following is an extract from the Financial Reporting Review Panel website relating to the Wiggins Group showing the restated financial results. Revenue recognition The 1999 accounts contained an...

-

Someone who exposes the ethical misdeeds of others in an organization is usually called a/an _________. (a) whistleblower (b) ethics advocate (c) ombudsman (d) stakeholder

-

If a manager fails to enforce a late-to-work policy for all workersthat is, by allowing some favored employees to arrive late without penaltiesthis would be considered a violation of _________. (a)...

-

According to research on ethics in the workplace, _________ is/are often a major and frequent source of pressures that create ethical dilemmas for people in their jobs. (a) declining morals in...

Study smarter with the SolutionInn App