WRITTEN ASSIGNMENT 3D PrintHub Ltd, is a one stop shop for 3D prints and consumables in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

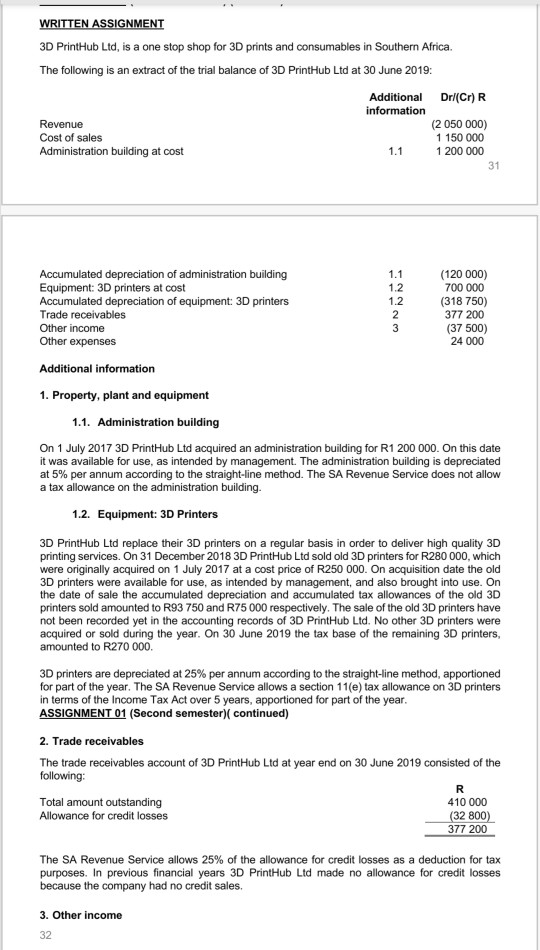

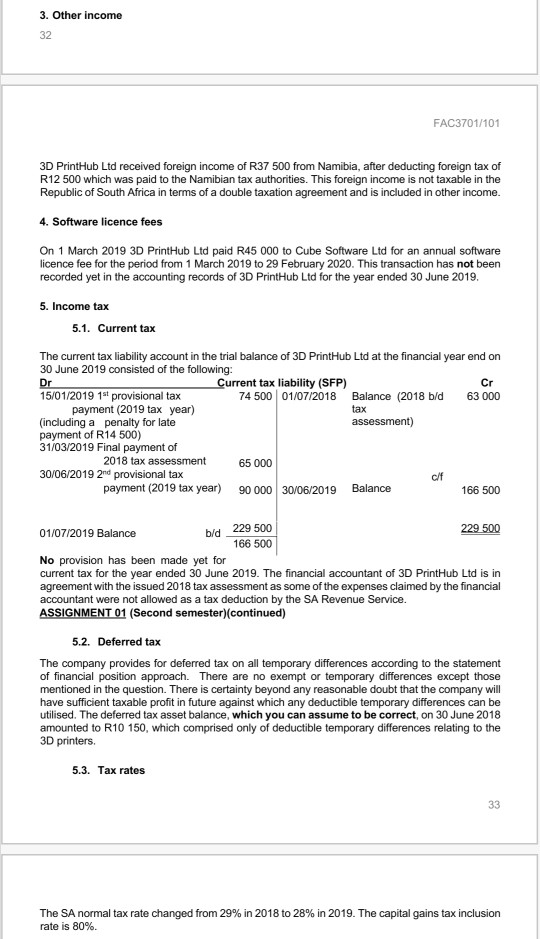

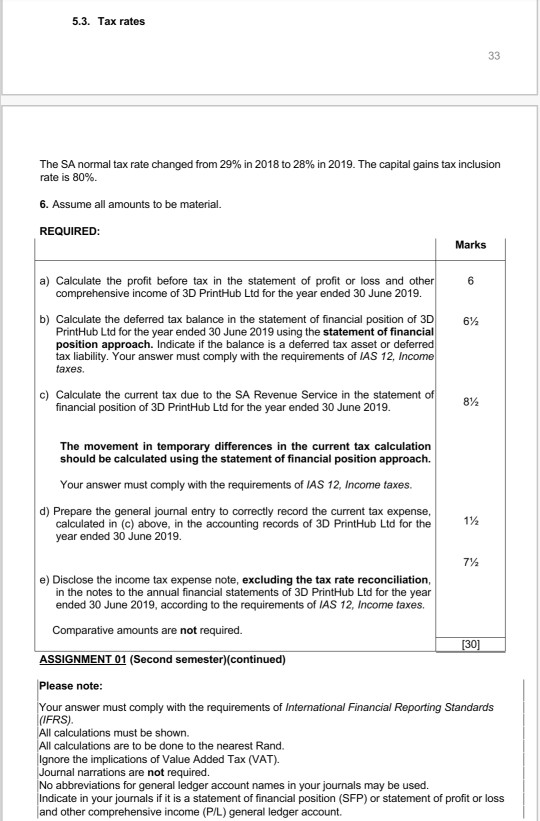

WRITTEN ASSIGNMENT 3D PrintHub Ltd, is a one stop shop for 3D prints and consumables in Southern Africa. The following is an extract of the trial balance of 3D PrintHub Ltd at 30 June 2019: Revenue Cost of sales Administration building at cost Additional information 1.1 Accumulated depreciation of administration building Equipment: 3D printers at cost Accumulated depreciation of equipment: 3D printers Trade receivables Other income Other expenses Additional information 1. Property, plant and equipment 1.1. Administration building On 1 July 2017 3D PrintHub Ltd acquired an administration building for R1 200 000. On this date it was available for use, as intended by management. The administration building is depreciated at 5% per annum according to the straight-line method. The SA Revenue Service does not allow a tax allowance on the administration building. 1.2. Equipment: 3D Printers 1.1 1.2 Total amount outstanding Allowance for credit losses Dr/(Cr) R (2 050 000) 1 150 000 1 200 000 1.2 2 3 3. Other income 32 31 (120 000) 700 000 (318 750) 377 200 (37 500) 24 000 3D PrintHub Ltd replace their 3D printers on a regular basis in order to deliver high quality 3D printing services. On 31 December 2018 3D PrintHub Ltd sold old 3D printers for R280 000, which were originally acquired on 1 July 2017 at a cost price of R250 000. On acquisition date the old 3D printers were available for use, as intended by management, and also brought into use. On the date of sale the accumulated depreciation and accumulated tax allowances of the old 3D printers sold amounted to R93 750 and R75 000 respectively. The sale of the old 3D printers have not been recorded yet in the accounting records of 3D PrintHub Ltd. No other 3D printers were acquired or sold during the year. On 30 June 2019 the tax base of the remaining 3D printers, amounted to R270 000. 3D printers are depreciated at 25% per annum according to the straight-line method, apportioned for part of the year. The SA Revenue Service allows a section 11(e) tax allowance on 3D printers in terms of the Income Tax Act over 5 years, apportioned for part of the year. ASSIGNMENT 01 (Second semester)( continued) 2. Trade receivables The trade receivables account of 3D PrintHub Ltd at year end on 30 June 2019 consisted of the following: R 410 000 (32 800) 377 200 The SA Revenue Service allows 25% of the allowance for credit losses as a deduction for tax purposes. In previous financial years 3D PrintHub Ltd made no allowance for credit losses because the company had no credit sales. 3. Other income 32 3D PrintHub Ltd received foreign income of R37 500 from Namibia, after deducting foreign tax of R12 500 which was paid to the Namibian tax authorities. This foreign income is not taxable in the Republic of South Africa in terms of a double taxation agreement and is included in other income. 4. Software licence fees On 1 March 2019 3D PrintHub Ltd paid R45 000 to Cube Software Ltd for an annual software licence fee for the period from 1 March 2019 to 29 February 2020. This transaction has not been recorded yet in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. 5. Income tax 5.1. Current tax The current tax liability account in the trial balance of 3D PrintHub Ltd at the financial year end on 30 June 2019 consisted of the following: Dr 15/01/2019 1st provisional tax payment (2019 tax year) (including a penalty for late payment of R14 500) 31/03/2019 Final payment of Current tax liability (SFP) 74 500 01/07/2018 2018 tax assessment 30/06/2019 2nd provisional tax payment (2019 tax year) 65 000 90 000 30/06/2019 FAC3701/101 229 500 166 500 Balance (2018 b/d tax assessment) Balance c/f Cr 63 000 166 500 229 500 01/07/2019 Balance b/d No provision has been made yet for current tax for the year ended 30 June 2019. The financial accountant of 3D PrintHub Ltd is in agreement with the issued 2018 tax assessment as some of the expenses claimed by the financial accountant were not allowed as a tax deduction by the SA Revenue Service. ASSIGNMENT 01 (Second semester) (continued) 5.2. Deferred tax The company provides for deferred tax on all temporary differences according to the statement of financial position approach. There are no exempt or temporary differences except those mentioned in the question. There is certainty beyond any reasonable doubt that the company will have sufficient taxable profit in future against which any deductible temporary differences can be utilised. The deferred tax asset balance, which you can assume to be correct, on 30 June 2018 amounted to R10 150, which comprised only of deductible temporary differences relating to the 3D printers. 5.3. Tax rates 33 The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 5.3. Tax rates The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 6. Assume all amounts to be material. REQUIRED: a) Calculate the profit before tax in the statement of profit or loss and other comprehensive income of 3D PrintHub Ltd for the year ended 30 June 2019. b) Calculate the deferred tax balance in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019 using the statement of financial position approach. Indicate if the balance is a deferred tax asset or deferred tax liability. Your answer must comply with the requirements of IAS 12, Income taxes. c) Calculate the current tax due to the SA Revenue Service in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019. The movement in temporary differences in the current tax calculation should be calculated using the statement of financial position approach. Your answer must comply with the requirements of IAS 12, Income taxes. d) Prepare the general journal entry to correctly record the current tax expense, calculated in (c) above, in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. Marks 6 6½ 8½ 1½ 7½ 33 e) Disclose the income tax expense note, excluding the tax rate reconciliation, in the notes to the annual financial statements of 3D PrintHub Ltd for the year ended 30 June 2019, according to the requirements of IAS 12, Income taxes. Comparative amounts are not required. ASSIGNMENT 01 (Second semester) (continued) Please note: Your answer must comply with the requirements of International Financial Reporting Standards (IFRS). [30] All calculations must be shown. All calculations are to be done to the nearest Rand. Ignore the implications of Value Added Tax (VAT). Journal narrations are not required. No abbreviations for general ledger account names in your journals may be used. Indicate in your journals if it is a statement of financial position (SFP) or statement of profit or loss and other comprehensive income (P/L) general ledger account. WRITTEN ASSIGNMENT 3D PrintHub Ltd, is a one stop shop for 3D prints and consumables in Southern Africa. The following is an extract of the trial balance of 3D PrintHub Ltd at 30 June 2019: Revenue Cost of sales Administration building at cost Additional information 1.1 Accumulated depreciation of administration building Equipment: 3D printers at cost Accumulated depreciation of equipment: 3D printers Trade receivables Other income Other expenses Additional information 1. Property, plant and equipment 1.1. Administration building On 1 July 2017 3D PrintHub Ltd acquired an administration building for R1 200 000. On this date it was available for use, as intended by management. The administration building is depreciated at 5% per annum according to the straight-line method. The SA Revenue Service does not allow a tax allowance on the administration building. 1.2. Equipment: 3D Printers 1.1 1.2 Total amount outstanding Allowance for credit losses Dr/(Cr) R (2 050 000) 1 150 000 1 200 000 1.2 2 3 3. Other income 32 31 (120 000) 700 000 (318 750) 377 200 (37 500) 24 000 3D PrintHub Ltd replace their 3D printers on a regular basis in order to deliver high quality 3D printing services. On 31 December 2018 3D PrintHub Ltd sold old 3D printers for R280 000, which were originally acquired on 1 July 2017 at a cost price of R250 000. On acquisition date the old 3D printers were available for use, as intended by management, and also brought into use. On the date of sale the accumulated depreciation and accumulated tax allowances of the old 3D printers sold amounted to R93 750 and R75 000 respectively. The sale of the old 3D printers have not been recorded yet in the accounting records of 3D PrintHub Ltd. No other 3D printers were acquired or sold during the year. On 30 June 2019 the tax base of the remaining 3D printers, amounted to R270 000. 3D printers are depreciated at 25% per annum according to the straight-line method, apportioned for part of the year. The SA Revenue Service allows a section 11(e) tax allowance on 3D printers in terms of the Income Tax Act over 5 years, apportioned for part of the year. ASSIGNMENT 01 (Second semester)( continued) 2. Trade receivables The trade receivables account of 3D PrintHub Ltd at year end on 30 June 2019 consisted of the following: R 410 000 (32 800) 377 200 The SA Revenue Service allows 25% of the allowance for credit losses as a deduction for tax purposes. In previous financial years 3D PrintHub Ltd made no allowance for credit losses because the company had no credit sales. 3. Other income 32 3D PrintHub Ltd received foreign income of R37 500 from Namibia, after deducting foreign tax of R12 500 which was paid to the Namibian tax authorities. This foreign income is not taxable in the Republic of South Africa in terms of a double taxation agreement and is included in other income. 4. Software licence fees On 1 March 2019 3D PrintHub Ltd paid R45 000 to Cube Software Ltd for an annual software licence fee for the period from 1 March 2019 to 29 February 2020. This transaction has not been recorded yet in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. 5. Income tax 5.1. Current tax The current tax liability account in the trial balance of 3D PrintHub Ltd at the financial year end on 30 June 2019 consisted of the following: Dr 15/01/2019 1st provisional tax payment (2019 tax year) (including a penalty for late payment of R14 500) 31/03/2019 Final payment of Current tax liability (SFP) 74 500 01/07/2018 2018 tax assessment 30/06/2019 2nd provisional tax payment (2019 tax year) 65 000 90 000 30/06/2019 FAC3701/101 229 500 166 500 Balance (2018 b/d tax assessment) Balance c/f Cr 63 000 166 500 229 500 01/07/2019 Balance b/d No provision has been made yet for current tax for the year ended 30 June 2019. The financial accountant of 3D PrintHub Ltd is in agreement with the issued 2018 tax assessment as some of the expenses claimed by the financial accountant were not allowed as a tax deduction by the SA Revenue Service. ASSIGNMENT 01 (Second semester) (continued) 5.2. Deferred tax The company provides for deferred tax on all temporary differences according to the statement of financial position approach. There are no exempt or temporary differences except those mentioned in the question. There is certainty beyond any reasonable doubt that the company will have sufficient taxable profit in future against which any deductible temporary differences can be utilised. The deferred tax asset balance, which you can assume to be correct, on 30 June 2018 amounted to R10 150, which comprised only of deductible temporary differences relating to the 3D printers. 5.3. Tax rates 33 The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 5.3. Tax rates The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 6. Assume all amounts to be material. REQUIRED: a) Calculate the profit before tax in the statement of profit or loss and other comprehensive income of 3D PrintHub Ltd for the year ended 30 June 2019. b) Calculate the deferred tax balance in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019 using the statement of financial position approach. Indicate if the balance is a deferred tax asset or deferred tax liability. Your answer must comply with the requirements of IAS 12, Income taxes. c) Calculate the current tax due to the SA Revenue Service in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019. The movement in temporary differences in the current tax calculation should be calculated using the statement of financial position approach. Your answer must comply with the requirements of IAS 12, Income taxes. d) Prepare the general journal entry to correctly record the current tax expense, calculated in (c) above, in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. Marks 6 6½ 8½ 1½ 7½ 33 e) Disclose the income tax expense note, excluding the tax rate reconciliation, in the notes to the annual financial statements of 3D PrintHub Ltd for the year ended 30 June 2019, according to the requirements of IAS 12, Income taxes. Comparative amounts are not required. ASSIGNMENT 01 (Second semester) (continued) Please note: Your answer must comply with the requirements of International Financial Reporting Standards (IFRS). [30] All calculations must be shown. All calculations are to be done to the nearest Rand. Ignore the implications of Value Added Tax (VAT). Journal narrations are not required. No abbreviations for general ledger account names in your journals may be used. Indicate in your journals if it is a statement of financial position (SFP) or statement of profit or loss and other comprehensive income (P/L) general ledger account.

Expert Answer:

Answer rating: 100% (QA)

Working Note Calculation of dep for PPE Administration building co... View the full answer

Related Book For

Accounting

ISBN: 978-1118608227

9th edition

Authors: Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett

Posted Date:

Students also viewed these accounting questions

-

The following is an extract from Accountancy Age, 25 January 2001. A powerful and shadowy group of senior partners from the seven largest firms has emerged to move closer to edging control of...

-

The following is an extract of an article discussing the importance of companies disclosing information in annual reports. Companies are still failing to provide a full and clear picture of their...

-

The following is an extract of Errsea's balances of property, plant and equipment and related government grants at 1 April 2006. Details including purchases and disposals of plant and related...

-

Following the example from the picture below, do the same for tryptophan and aspartate, consider pk1, pkR and pk2. COOH HSCH Net charge: PH H CH COOH +1 10 8 6 4 2 COOH 0 Glutamate Jpk 2.19 pk 4.25 ...

-

To obtain person analysis data, why not just use the performance appraisal completed by the supervisor? How can you obtain the best information possible if performance appraisal must be used? How do...

-

A company seeking a line of credit at a bank was turned down. Among other things, the bank stated that the company's 2 to 1 current ratio was not adequate. Give reasons why a 2 to 1 current ratio...

-

Define hardness.

-

After the success of the company's first two months, Santana Rey continues to operate Business Solutions. (Transactions for the first two months are described in the Chapter 2 serial problem.) The...

-

Cost of a Fixed Asset Borges Inc. recently purchased land to use for the construction of its new manufacturing facility and incurred the following costs: purchase price, $83,000; interest charges,...

-

On January 1, 20X5, Piper Ltd. purchased 100% of the shares of Sutton Ltd. for $ 1,085,000. At that time Sutton Ltd. had the following SFP: The bonds were issued at par and will mature in 10 years....

-

ALGEBRAIC EXPRESSIONS In algebra, a term is an individual part of an algebraic expression. Terms are separated by addition (+) or subtraction (-) signs, and can consist of numbers, variables...

-

What is the cost of translation hedging when currency options are used?

-

Why is it important to first forecast the projects local currency cash flows?

-

How can a company alter its translation exposure?

-

What does it mean to describe financing as a global procurement decision?

-

When evaluating foreign projects, why is discounting residual cash flows to equity holders at the equity cost of capital preferable to discounting free cash flows at the weighted cost of capital?

-

Project A is selected because it has a low cost of $2,000, it gives a rate of return of 8%, Project B was not selected, it needs a higher cost of $5,000, it is projected to give a rate of return of...

-

By referring to Figure 13.18, determine the mass of each of the following salts required to form a saturated solution in 250 g of water at 30 oC: (a) KClO3, (b) Pb(NO3)2, (c) Ce2(SO4)3.

-

The accounting treatment of a partners drawings differs when separate Retained Earnings accounts are kept for each partner as opposed to not having Retained Earnings accounts. Choice of method is...

-

Using the periodic inventory system, prepare general journal entries for the following transactions of Heidelberg Housewares (assume no GST): 1. Purchased inventory on credit for $58 200. 2. Sold...

-

Fly Fast Ltd operates a small charter plane operation in South West Queensland. The airline provides a fly in fly out service to mining operations in this area. Currently Fly Fast operates one plane...

-

Determine the longitudinal tensile strength of the hybrid carbon/aramid/ epoxy composite described in Problem 3.4 and Figure 3.10 of Chapter 3 if the fiber packing array is square with the closest...

-

For the IM-9/8551-7 carbon/epoxy composite rod design of Problem 3.3 in Chapter 3, what would be the increase in the longitudinal tensile strength compared with that of the original 6061-T6 aluminum...

-

Assuming that the failure mode for longitudinal compression of unidirectional E-glass/epoxy with fiber volume fraction \(v_{\mathrm{f}}=0.6\) is a transverse tensile rupture due to Poisson strains,...

Study smarter with the SolutionInn App