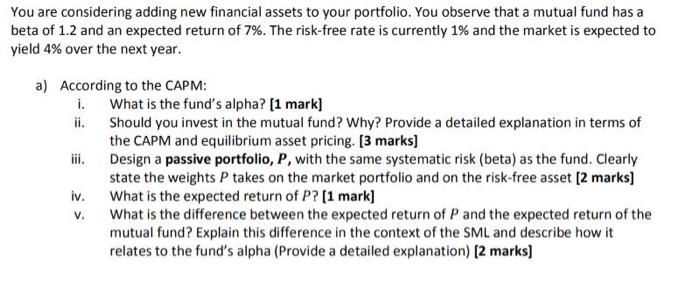

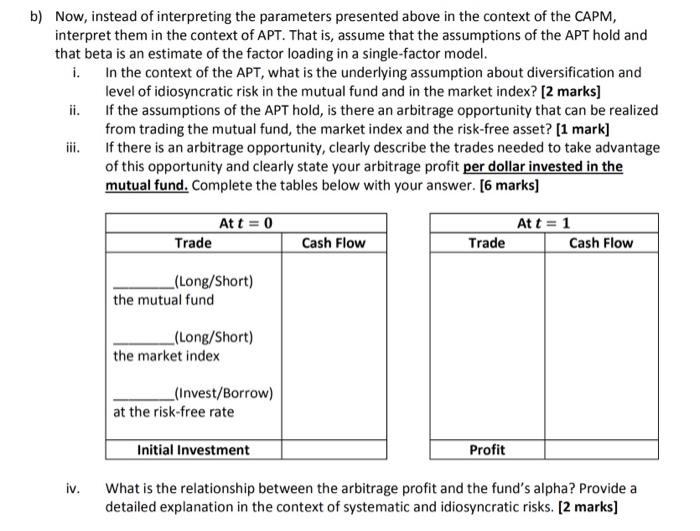

You are considering adding new financial assets to your portfolio. You observe that a mutual fund...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a i What is the funds alpha The alpha of the mutual fund is 5 This can be calculated by subtracting the expected return of the fund 7 from the expected return of the market portfolio 4 adjusted for th... View the full answer

Related Book For

Posted Date: