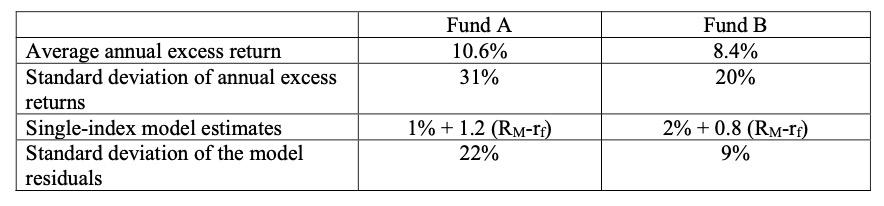

An investor is evaluating the performance of two actively managed mutual funds, A and B. The annual

Fantastic news! We've Found the answer you've been seeking!

Question:

An investor is evaluating the performance of two actively managed mutual funds, A and B. The annual risk-free rate of return over the period was 4%, and the average annual return of the market portfolio was 12%. The standard deviation of the market portfolio returns was 20%. The table below reports the statistics and the regression estimation results of the single- index model for annual excess returns of the two funds. The investor is choosing fund A or fund B to become part of his actively managed stock portfolio. Which fund should he choose?

The investor is choosing fund A or fund B to become part of his actively managed stock portfolio. Which fund should he choose?

Expert Answer:

To determine which fund the investor should choose for his actively managed stock portfolio lets co... View the full answer

Related Book For

Posted Date: