Another method of measuring interest-rate risk is the duration gap analysis, examines the sensitivity of the market

Question:

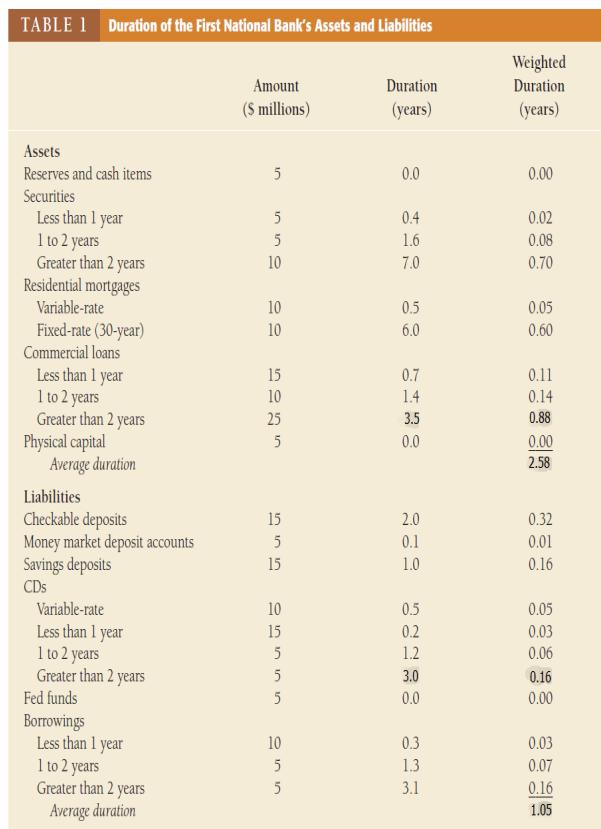

Another method of measuring interest-rate risk is the duration gap analysis, examines the sensitivity of the market value of the financial institution’s net worth to changes in interest rates. Duration analysis is based on Macaulay’s concept of duration, which measures the average lifetime of a security’s stream of payments. Duration is a useful concept, because it provides a good approximation, particularly when interest-rate changes are small, of the sensitivity of a security’s market value to a change in its interest rate. Bank managers can figure out the effect of interest-rate changes on the market value of net worth by calculating the average duration for assets and for liabilities. These durations are then used to estimate the effects of interest-rate changes. Table 1 shows the balance sheet of the First National Bank. The bank manager has already calculated the duration of each assets and liabilities, as listed in the last column of the table.

Q1 The bank manager wants to know what happens when the interest rate rises from 10% to 11%. The total asset value is $100 million, and the total liability value is $95 million. Calculate the change in the market value of the assets and liabilities.

Q2 Based on the Q1, calculate the duration gap for the First National Bank.

Q3 What is the change in the market value of net worth as a percentage of assets if interest rates rise from 10% to 11%?

Expert Answer:

To calculate the changes in market values of assets and liabilities and the duration gap we will use the concept of duration and the formula for estim... View the full answer

Financial Markets and Institutions

ISBN: 978-0077861667

6th edition

Authors: Anthony Saunders, Marcia Cornett