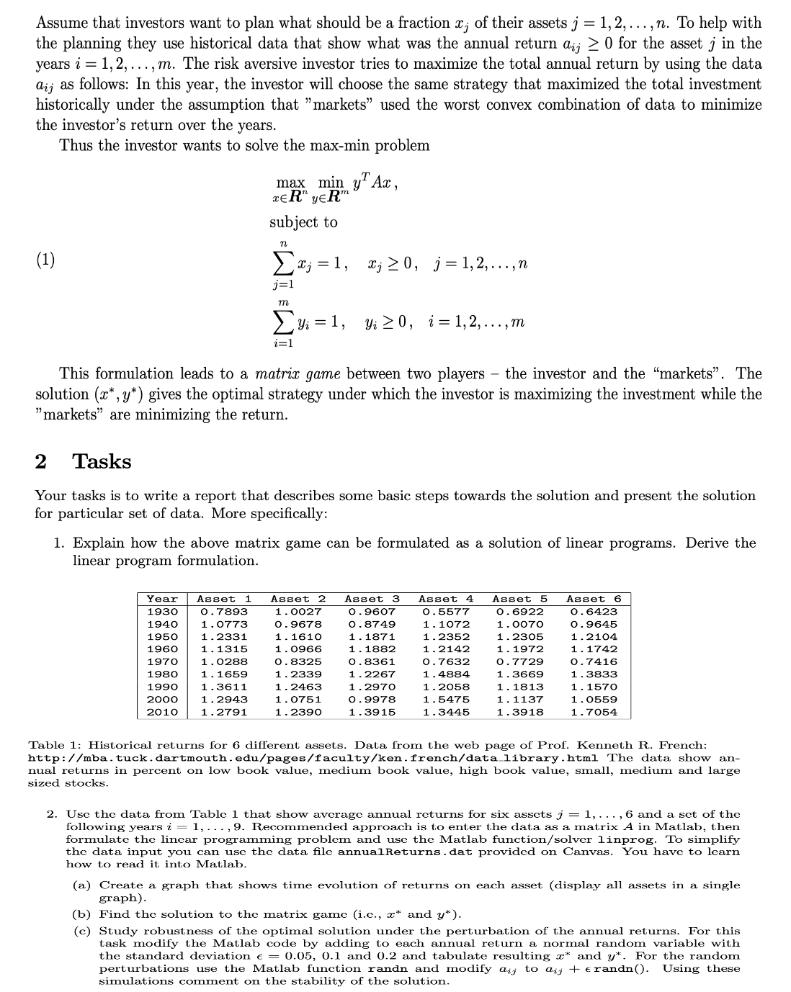

Assume that investors want to plan what should be a fraction x; of their assets j...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To formulate the matrix game as a linear programming problem we need to define the decision variables and the objective function as well as the constraints Decision Variables x A vector of fractions r... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: