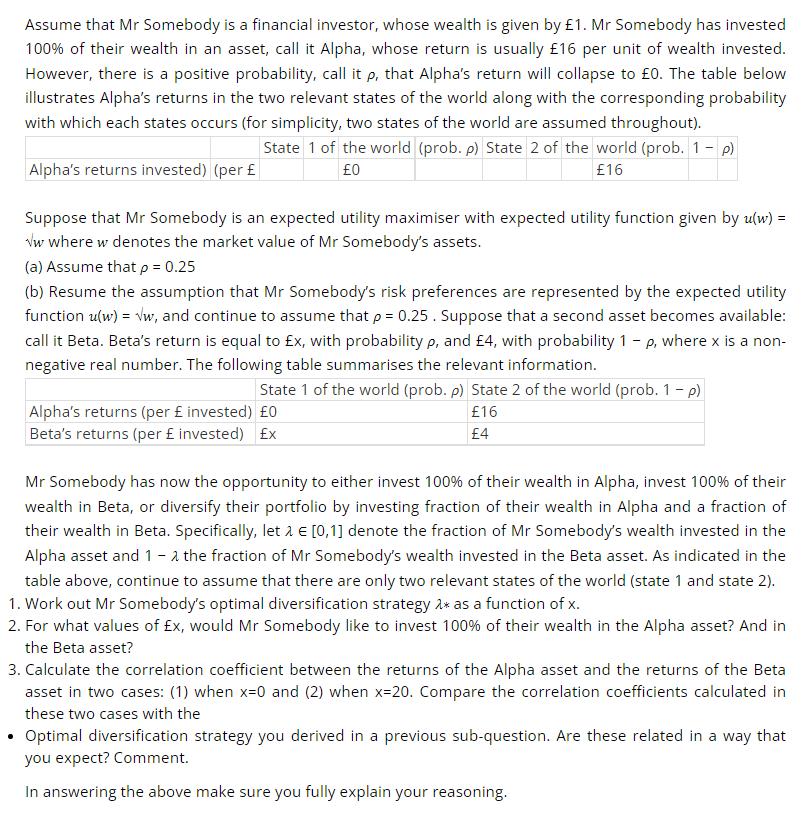

Assume that Mr Somebody is a financial investor, whose wealth is given by 1. Mr Somebody...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Assume that Mr Somebody is a financial investor, whose wealth is given by £1. Mr Somebody has invested 100% of their wealth in an asset, call it Alpha, whose return is usually £16 per unit of wealth invested. However, there is a positive probability, call it p, that Alpha's return will collapse to £0. The table below illustrates Alpha's returns in the two relevant states of the world along with the corresponding probability with which each states occurs (for simplicity, two states of the world are assumed throughout). State 1 of the world (prob. p) State 2 of the world (prob. 1 - p) Alpha's returns invested) (per £ £0 £16 Suppose that Mr Somebody is an expected utility maximiser with expected utility function given by u(w) = ww where w denotes the market value of Mr Somebody's assets. (a) Assume that p = 0.25 . (b) Resume the assumption that Mr Somebody's risk preferences are represented by the expected utility function u(w) = √w, and continue to assume that p = 0.25. Suppose that a second asset becomes available: call it Beta. Beta's return is equal to £x, with probability p, and £4, with probability 1 - p, where x is a non- negative real number. The following table summarises the relevant information. State 1 of the world (prob. p) State 2 of the world (prob. 1 - p) £16 £4 Alpha's returns (per £ invested) £0 Beta's returns (per £ invested) Ex Mr Somebody has now the opportunity to either invest 100% of their wealth in Alpha, invest 100% of their wealth in Beta, or diversify their portfolio by investing fraction of their wealth in Alpha and a fraction of their wealth in Beta. Specifically, let & € [0,1] denote the fraction of Mr Somebody's wealth invested in the Alpha asset and 1 - 2 the fraction of Mr Somebody's wealth invested in the Beta asset. As indicated in the table above, continue to assume that there are only two relevant states of the world (state 1 and state 2). 1. Work out Mr Somebody's optimal diversification strategy 2* as a function of x. 2. For what values of Ex, would Mr Somebody like to invest 100% of their wealth in the Alpha asset? And in the Beta asset? 3. Calculate the correlation coefficient between the returns of the Alpha asset and the returns of the Beta asset in two cases: (1) when x=0 and (2) when x=20. Compare the correlation coefficients calculated in these two cases with the Optimal diversification strategy you derived in a previous sub-question. Are these related in a way that you expect? Comment. In answering the above make sure you fully explain your reasoning. Assume that Mr Somebody is a financial investor, whose wealth is given by £1. Mr Somebody has invested 100% of their wealth in an asset, call it Alpha, whose return is usually £16 per unit of wealth invested. However, there is a positive probability, call it p, that Alpha's return will collapse to £0. The table below illustrates Alpha's returns in the two relevant states of the world along with the corresponding probability with which each states occurs (for simplicity, two states of the world are assumed throughout). State 1 of the world (prob. p) State 2 of the world (prob. 1 - p) Alpha's returns invested) (per £ £0 £16 Suppose that Mr Somebody is an expected utility maximiser with expected utility function given by u(w) = ww where w denotes the market value of Mr Somebody's assets. (a) Assume that p = 0.25 . (b) Resume the assumption that Mr Somebody's risk preferences are represented by the expected utility function u(w) = √w, and continue to assume that p = 0.25. Suppose that a second asset becomes available: call it Beta. Beta's return is equal to £x, with probability p, and £4, with probability 1 - p, where x is a non- negative real number. The following table summarises the relevant information. State 1 of the world (prob. p) State 2 of the world (prob. 1 - p) £16 £4 Alpha's returns (per £ invested) £0 Beta's returns (per £ invested) Ex Mr Somebody has now the opportunity to either invest 100% of their wealth in Alpha, invest 100% of their wealth in Beta, or diversify their portfolio by investing fraction of their wealth in Alpha and a fraction of their wealth in Beta. Specifically, let & € [0,1] denote the fraction of Mr Somebody's wealth invested in the Alpha asset and 1 - 2 the fraction of Mr Somebody's wealth invested in the Beta asset. As indicated in the table above, continue to assume that there are only two relevant states of the world (state 1 and state 2). 1. Work out Mr Somebody's optimal diversification strategy 2* as a function of x. 2. For what values of Ex, would Mr Somebody like to invest 100% of their wealth in the Alpha asset? And in the Beta asset? 3. Calculate the correlation coefficient between the returns of the Alpha asset and the returns of the Beta asset in two cases: (1) when x=0 and (2) when x=20. Compare the correlation coefficients calculated in these two cases with the Optimal diversification strategy you derived in a previous sub-question. Are these related in a way that you expect? Comment. In answering the above make sure you fully explain your reasoning.

Expert Answer:

Answer rating: 100% (QA)

1 Work out Mr Somebodys optimal diversification strategy 2 as a function of x ANSWER Mr Somebodys optimal diversification strategy would be to invest ... View the full answer

Posted Date:

Students also viewed these economics questions

-

The table below illustrates the growth in worldwide Internet use. Year, x Number of Internet Users Worldwide, y (in millions) 2001, 0 ............................................... 495 2002, 1...

-

The table below illustrates the upward trend in America to choose cremation. Year, x Percentage of Deaths Followed by Cremation, y 2005, 0 .............................................. 32.3% 2006, 1...

-

Anne is a financial investor who actively buys and sells in the securities market. Now she has a portfolio of all blue chips, including: $13,500 of Share A, $7,600 of Share B, $14,700 of Share C, and...

-

In a study it is observed that the right ovary ovulates more than the left, all are possible explanation for the cause except a) Anatomical difference between right and left side b) Difference in...

-

How do organizational differences relate to strategies and business processes?

-

Reporting marketable securities available for sale at fair value on the balance sheet but not including the unrealized holding gains and losses in income is inconsistent and provides an opportunity...

-

Explain monetary base, required reserves and excess reserves.

-

Perez, CPA, has been asked by a nonpublic company audit entity to perform a nonrecurring engagement involving implementing an IT information and control system. The entity requests that, in setting...

-

An annuity provides for 20 annual payments. The first payment in one year is $500 and each successive payment increases by 5%. Find the present value of this annuity at an annual effective rate of...

-

You work for the 3T company, which expects to earn at least 18 percent on its investments. You have to choose between two similar projects. Below is the cash information for each project. Your...

-

In the Quality of GPS network what is the meaning that the normalized or standardized residuals have a value 1.0? Select one: a. The residuals are less than expected b. The residuals are large as...

-

A ship sailing in the Gulf Stream is heading 25.5 west of north at a speed of 4.05 m/s relative to the water. Its velocity relative to the Earth is 4.60 m/s 5.30 west of north. What is the velocity...

-

What are sequence numbers and why are they used? Describe an attack that uses sequence numbers? Why do you think the he numbering system is desired for use by technologists and hackers alike?

-

A gas has volume of 4 . 0 0 \ times 1 0 4 m 3 mol 1 , temperature of 2 8 8 K and pressure of 4 . 0 MPa. Justify whether the gas behaves as an ideal / perfect gas.

-

West Partners manufactures metal fixtures. Each fitting requires both steel and an alloy that can withstand extreme temperatures. The following data apply to the production of the fittings for year...

-

What is classful addressing? Why it is not used anymore? Discuss class B address in brief.

-

A. Kirchhoff's Law BNewton's Law of Cooling represents how fast heat diffuses through a material. A. Thermal Conductivity B. Conductivity A. Radiation given temperature and wavelength are equal. D....

-

Provide a draft/outline of legal research involving an indigenous Canadian woman charged with assault causing bodily harm under (Sec 267b) of the Criminal Code, where the crown wants a 12-month jail...

-

How does an individual know if all cash transactions have been properly accounted for on the statement of cash flows?

-

How are the cash flows originating from a company's financing activities identified?

-

Although physically counting a businesss inventory is integral to the periodic system of inventory recordkeeping, it is not an explicit component of the perpetual system. Nonetheless, most well-run...

Study smarter with the SolutionInn App