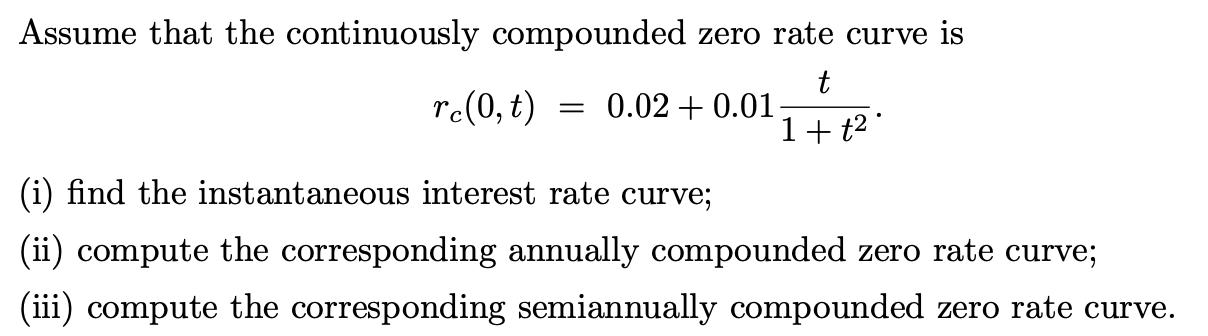

Assume that the continuously compounded zero rate curve is t re(0, t) = 0.02 +0.01- 1...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To solve the problem well follow the given information and formulas to find the instantaneous intere... View the full answer

Related Book For

Posted Date: