Assume that the risk-free rate is rf = 4% and the investor's risk aversion coefficient is A

Question:

Assume that the risk-free rate isrf= 4% and the investor's risk aversion coefficient is

A= 4.

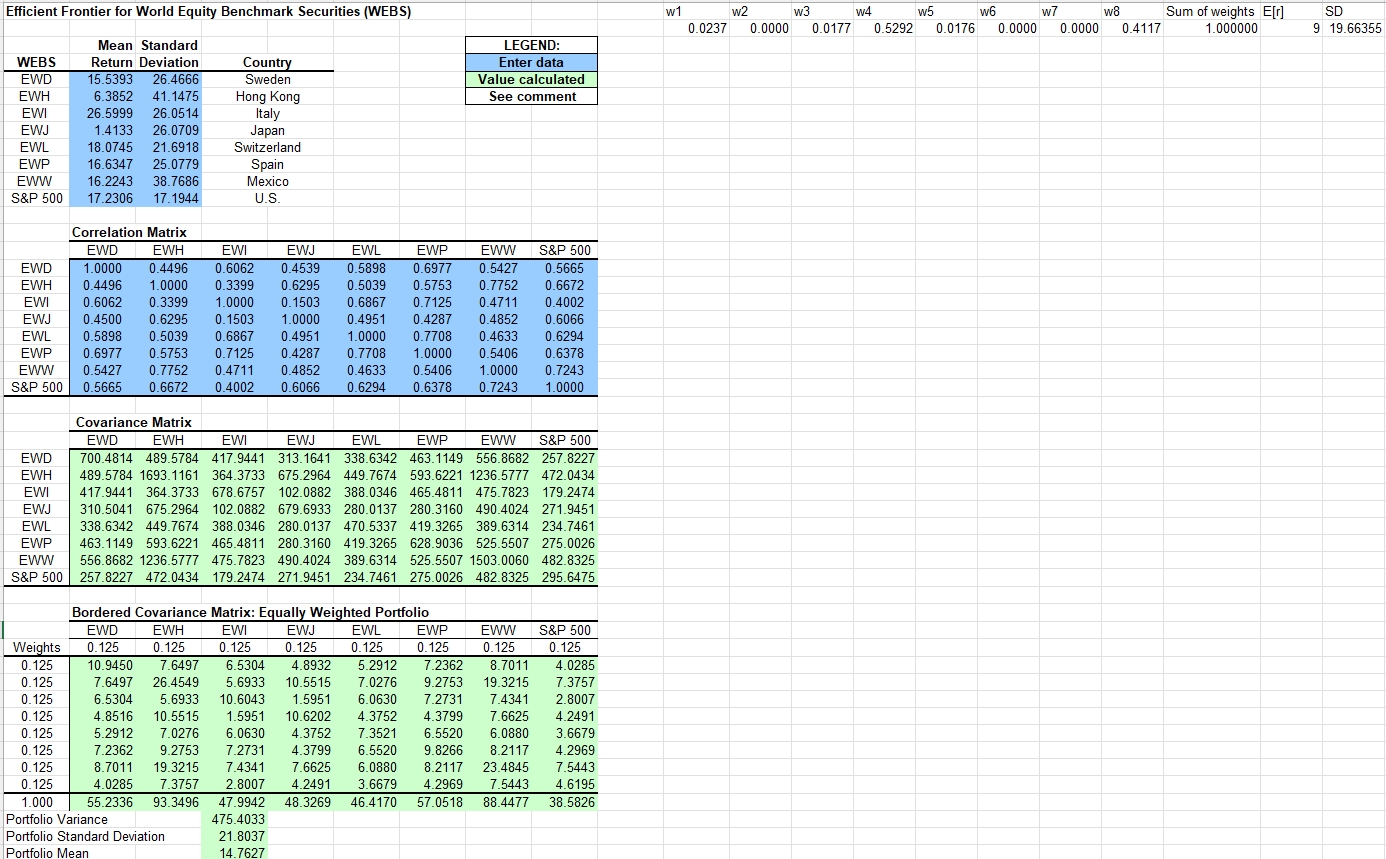

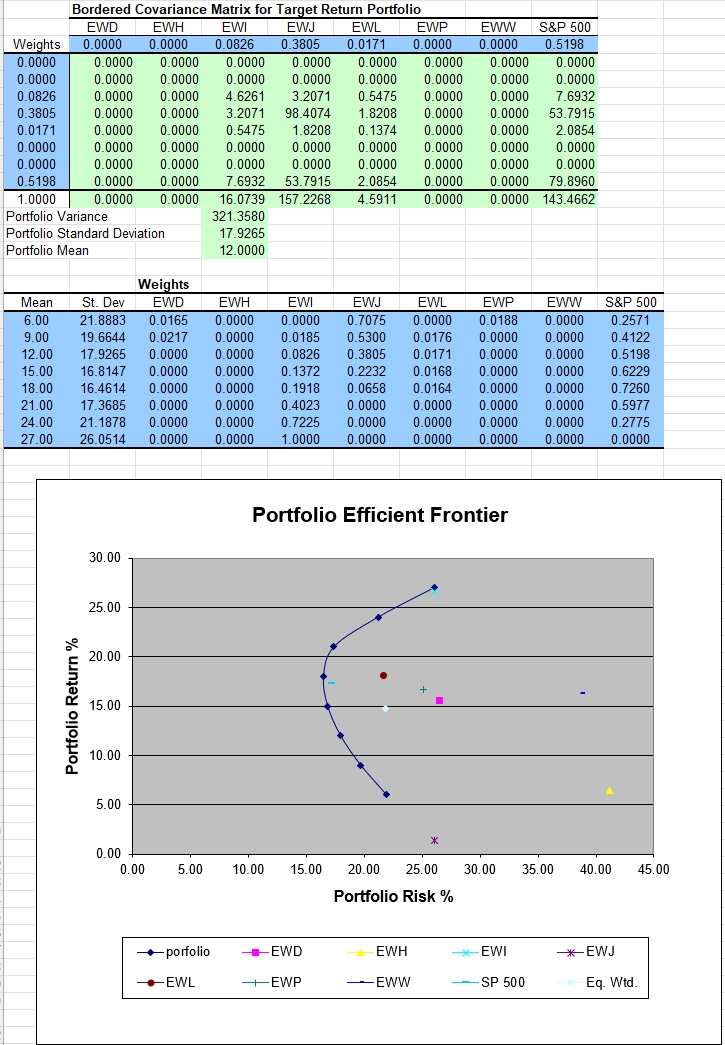

1. Consider return targets ranging from 6% to 26% (in increments of 2%). For each return

target, solve for the portfolio that yields this expected return and that has the smallest

standard deviation of returns possible. Plot the efficient frontier.

2. Solve for the Tangency portfolio's weights. Report the expected return and standard

deviation of this portfolio. Plot the tangency line. What is the maximum Sharpe ratio

possible?

3. Consider a portfolio with a weight ofy(%) on the Tangency portfolio and 1? yon

the risk free bond. Find the valuey ?that maximizes the investor's expected utility.

Use the weights of the Tangency portfolio found in question 2., find the weight of each

individual asset in the optimal portfolio.

4. Solve the utility maximization problem directly (that is, find the set of weights that

maximize the expected utility functionU=E[r]?1

2A?V ar(r)). Verify if these weights

are the same as the ones found in question 3.

5. Suppose that you're not allowed to short any assets. Does this change the optimal

portfolio? How much (in percentage) expected utility is lost because of this restriction?

Expert Answer:

Financial reporting, financial statement analysis and valuation a strategic perspective

ISBN: 978-0324789416

7th Edition

Authors: James M Wahlen, Stephen P Baginskl, Mark T Bradshaw