Assume that your firm is successful in gaining the audit of Air New Zealand Limited. You are

Question:

Assume that your firm is successful in gaining the audit of Air New Zealand Limited. You are asked by the audit engagement partner to plan the audit, in particular determine areas of risk, materiality and assertions to be examined. As always you wish to keep your detection risk to a minimum.

NOTE: You are not expected to assess control risks as this would require having access to this entity, which is not permitted for the purposes of this presentation workshop.

Questions to be addressed by those presenting (and for those not presenting, in bullet-point summaries) are:

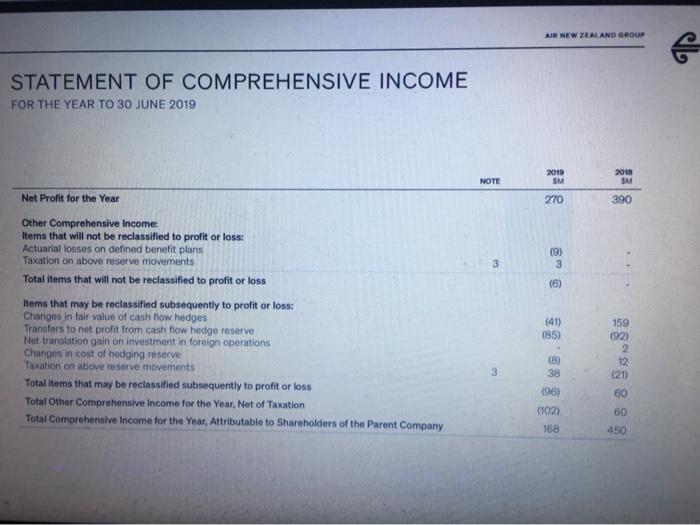

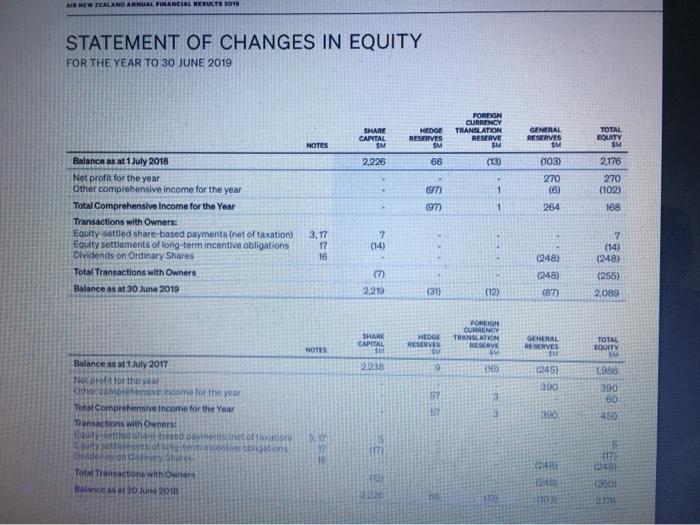

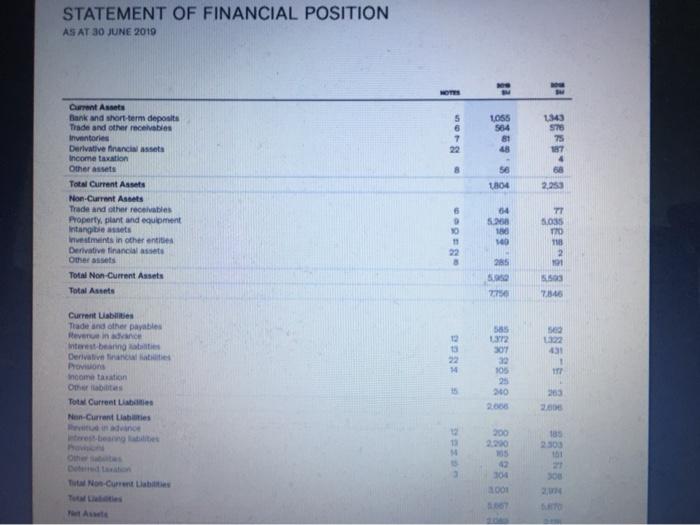

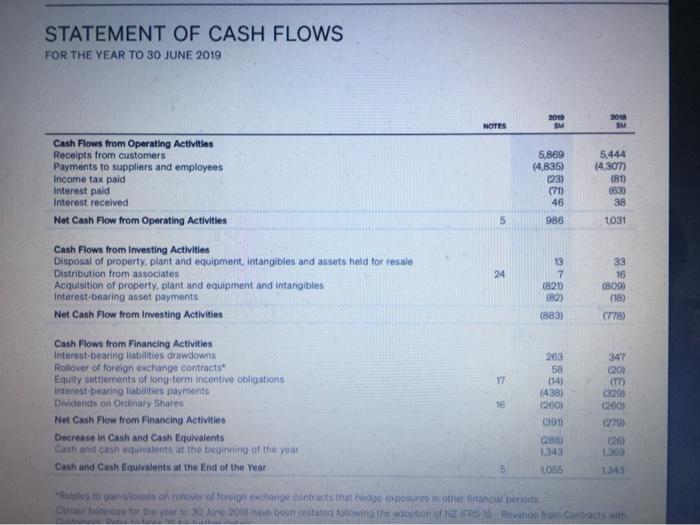

a) Carry out a preliminary analytical procedure to review the Air New Zealand annual financial statements as these are appropriate for the client. Explain the reason for choosing selected ratios, what you found and, how the results will influence your planning of the audit.

b) Based on the ‘business risk’ and ‘industry risk’ identified (in workshop 1) for Air New Zealand, what assertions over account balances and other disclosures in the financial statements will these risks impact and how? Identify key assertions that you think need to be tested and explain the audit objective behind these tests.

c) Using your judgment, identify a ‘base’ and select a materiality level for Air New Zealand’s (Group) balance sheet. Justify y o u r decision. Allocate that amount to the balance sheet accounts in proportion to their $ size and assess the results. Consider what would have occurred if you had chosen a larger or a smaller ‘materiality’ amount, or if you had allocated them differently

Please answer the questions which you are able to answer.

Expert Answer:

AGross Profit Margin Gross profit x 100 NZ000 Revenue 2019 251890 x 100 266361 x 100 276183 x 100 409372 425593 445348 6153 625 62 Return on Equity Ne... View the full answer

Auditing and Assurance Services A Systematic Approach

ISBN: 978-1259162343

9th edition

Authors: William Messier, Steven Glover, Douglas Prawitt