Assuming Dash Spencer LLP owed a duty of care to the Booster Bank, did Dash Spencer,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

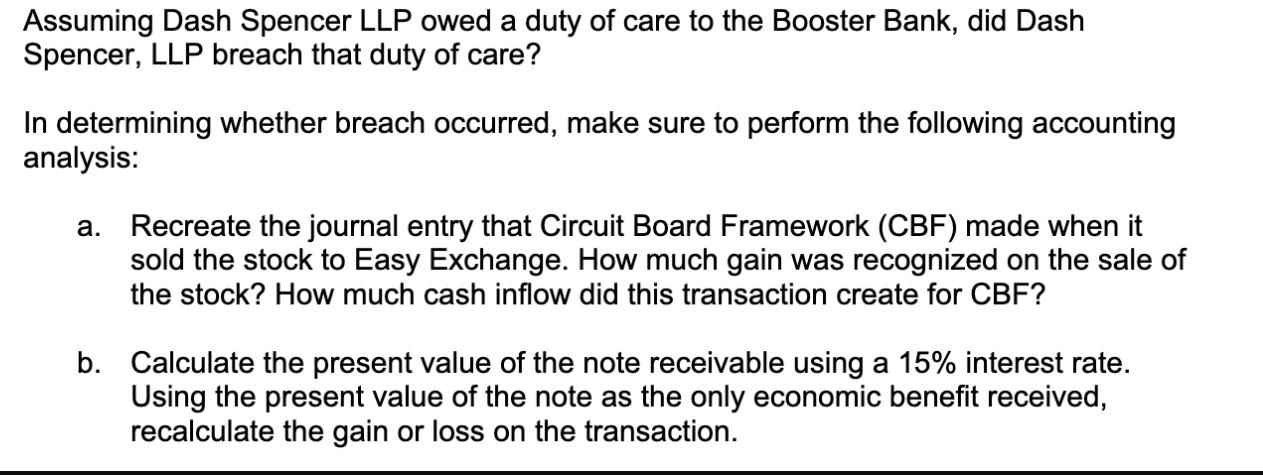

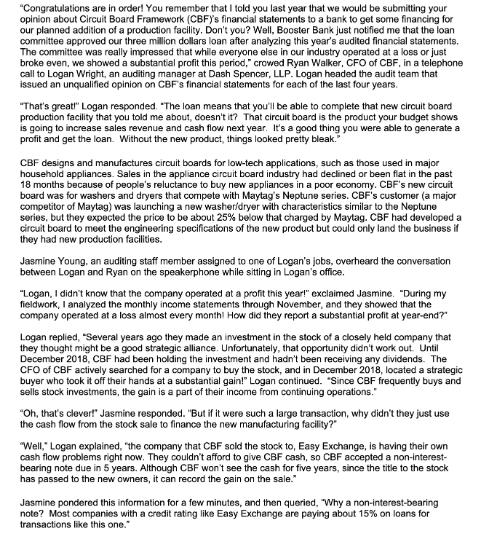

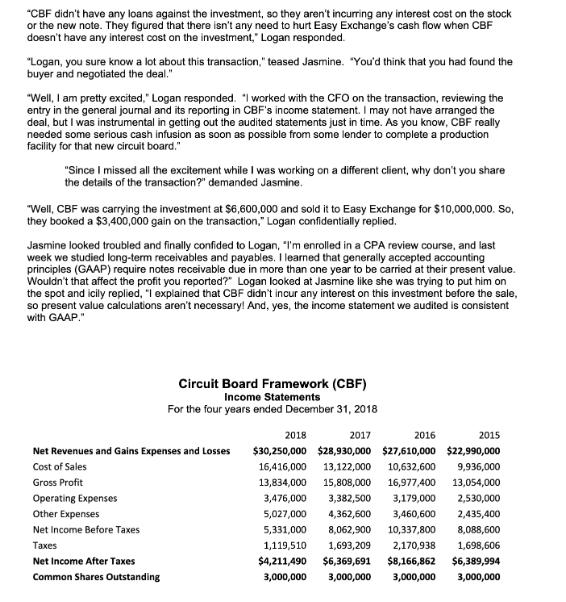

Assuming Dash Spencer LLP owed a duty of care to the Booster Bank, did Dash Spencer, LLP breach that duty of care? In determining whether breach occurred, make sure to perform the following accounting analysis: a. Recreate the journal entry that Circuit Board Framework (CBF) made when it sold the stock to Easy Exchange. How much gain was recognized on the sale of the stock? How much cash inflow did this transaction create for CBF? b. Calculate the present value of the note receivable using a 15% interest rate. Using the present value of the note as the only economic benefit received, recalculate the gain or loss on the transaction. "Congratulations are in order! You remember that I told you last year that we would be submitting your opinion about Circuit Board Framework (CBFY's financial statements to a bank to get some financing for our planned addition of a production facility. Don't you? Well, Booster Bank just notified me that the loan committee approved our three million dollars loan after analyzing this year's audited financial statements. The committee was really impressed that while everyone else in cur industry operated at a loss or just broke even, we showed a substantial profit this period," crowed Ryan Walker, CFO of CBF, in a telephone call to Logan Wright, an auditing manager at Dash Spencer, LLP. Logan headed the audit team that issued an unqualified opinion on CBF's financial statements for each of the last four years. "That's great!" Logan responded. "The loan means that you'll be able to complete that new circuit board production facility that you told me about, doesn't it? That circuit board is the product your budget shows is going to increase sales revenue and cash flow next year. It's a good thing you were able to generate a profit and get the loan. Without the new product, things looked pretty bleak." CBF designs and manufactures circuit boards for low-tech applications, such as those used in major household appliances. Sales in the appliance circuit board industry had declined or been flat in the past 18 months because of people's reluctance to buy new appliances in a poor economy. CBF's new circuit board was for washers and dryers that compete with Maytag's Neptune series. CBF's customer (a major competitor of Maytag) was launching a new washer/dryer with characteristics similar to the Neptune series, but they expected the price to be about 25% below that charged by Maytag. CBF had developed a circuit board to meet the engineering specifications of the new product but could only land the business if they had new production facilities. Jasmine Young, an auditing staff member assigned to one of Logan's jobs, overheard the conversation between Logan and Ryan on the speakerphone while sitting in Logan's office. "Logan, I didn't know that the company operated at a profit this year!" exclaimed Jasmine. "During my fieldwork, I analyzed the monthly income statements through November, and they showed that the company operated at a loss almost every month! How did they report a substantial profit at year-end?" Logan replied, "Several years ago they made an investment in the stock of a closely held company that they thought might be a good strategic alliance. Unfortunately, that opportunity didn't work out. Until December 2018, CBF had been holding the investment and hadn't been receiving any dividends. The CFO of CBF actively searched for a company to buy the stock, and in December 2018, located a strategic buyer who took it off their hands at a substantial gain!" Logan continued. "Since CBF frequently buys and sells stock investments, the gain is a part of their income from continuing operations." "Oh, that's clever!" Jasmine responded. "But if it were such a large transaction, why didn't they just use the cash flow from the stock sale to finance the new manufacturing facility?" "Well," Logan explained, "the company that CBF sold the stock to, Easy Exchange, is having their own cash flow problems right now. They couldn't afford to give CBF cash, so CBF accepted a non-interest- bearing note due in 5 years. Although CBF won't see the cash for five years, since the title to the stock has passed to the new owners, it can record the gain on the sale." Jasmine pondered this information for a few minutes, and then queried, "Why a non-interest-bearing note? Most companies with a credit rating like Easy Exchange are paying about 15% on loans for transactions like this one." "CBF didn't have any loans against the investment, so they aren't incurring any interest cost on the stock or the new note. They figured that there isn't any need to hurt Easy Exchange's cash flow when CBF doesn't have any interest cost on the investment, Logan responded. "Logan, you sure know a lot about this transaction," teased Jasmine. "You'd think that you had found the buyer and negotiated the deal." "Well, I am pretty excited," Logan responded. "I worked with the CFO on the transaction, reviewing the entry in the general journal and its reporting in CBF's income statement. I may not have arranged the deal, but I was instrumental in getting out the audited statements just in time. As you know, CBF really needed some serious cash infusion as soon as possible from some lender to complete a production facility for that new circuit board." "Since I missed all the excitement while I was working on a different client, why don't you share the details of the transaction?" demanded Jasmine. "Well, CBF was carrying the investment at $6,600,000 and sold it to Easy Exchange for $10,000,000. So, they booked a $3,400,000 gain on the transaction," Logan confidentially replied. Jasmine looked troubled and finally confided to Logan, "I'm enrolled in a CPA review course, and last week we studied long-term receivables and payables. I learned that generally accepted accounting principles (GAAP) require notes receivable due in more than one year to be carried at their present value. Wouldn't that affect the profit you reported?" Logan looked at Jasmine like she was trying to put him on the spot and icily replied, "I explained that CBF didn't incur any interest on this investment before the sale, so present value calculations aren't necessary! And, yes, the income statement we audited is consistent with GAAP." Circuit Board Framework (CBF) Income Statements For the four years ended December 31, 2018 Net Revenues and Gains Expenses and Losses Cost of Sales Gross Profit Operating Expenses Other Expenses Net Income Before Taxes Taxes Net Income After Taxes Common Shares Outstanding 2018 2016 $30,250,000 $28,930,000 $27,610,000 $22,990,000 16,416,000 13,122,000 10,632,600 9,936,000 13,834,000 15,808,000 16,977,400 13,054,000 3,476,000 3,382,500 3,179,000 2,530,000 2,435,400 5,027,000 4,362,600 3,460,600 5,331,000 8,062,900 10,337,800 8,088,600 1,119,510 1,693,209 2,170,938 1,698,606 $4,211,490 $6,369,691 $8,166,862 $6,389,994 3,000,000 3,000,000 3,000,000 3,000,000 2017 2015 Assuming Dash Spencer LLP owed a duty of care to the Booster Bank, did Dash Spencer, LLP breach that duty of care? In determining whether breach occurred, make sure to perform the following accounting analysis: a. Recreate the journal entry that Circuit Board Framework (CBF) made when it sold the stock to Easy Exchange. How much gain was recognized on the sale of the stock? How much cash inflow did this transaction create for CBF? b. Calculate the present value of the note receivable using a 15% interest rate. Using the present value of the note as the only economic benefit received, recalculate the gain or loss on the transaction. "Congratulations are in order! You remember that I told you last year that we would be submitting your opinion about Circuit Board Framework (CBFY's financial statements to a bank to get some financing for our planned addition of a production facility. Don't you? Well, Booster Bank just notified me that the loan committee approved our three million dollars loan after analyzing this year's audited financial statements. The committee was really impressed that while everyone else in cur industry operated at a loss or just broke even, we showed a substantial profit this period," crowed Ryan Walker, CFO of CBF, in a telephone call to Logan Wright, an auditing manager at Dash Spencer, LLP. Logan headed the audit team that issued an unqualified opinion on CBF's financial statements for each of the last four years. "That's great!" Logan responded. "The loan means that you'll be able to complete that new circuit board production facility that you told me about, doesn't it? That circuit board is the product your budget shows is going to increase sales revenue and cash flow next year. It's a good thing you were able to generate a profit and get the loan. Without the new product, things looked pretty bleak." CBF designs and manufactures circuit boards for low-tech applications, such as those used in major household appliances. Sales in the appliance circuit board industry had declined or been flat in the past 18 months because of people's reluctance to buy new appliances in a poor economy. CBF's new circuit board was for washers and dryers that compete with Maytag's Neptune series. CBF's customer (a major competitor of Maytag) was launching a new washer/dryer with characteristics similar to the Neptune series, but they expected the price to be about 25% below that charged by Maytag. CBF had developed a circuit board to meet the engineering specifications of the new product but could only land the business if they had new production facilities. Jasmine Young, an auditing staff member assigned to one of Logan's jobs, overheard the conversation between Logan and Ryan on the speakerphone while sitting in Logan's office. "Logan, I didn't know that the company operated at a profit this year!" exclaimed Jasmine. "During my fieldwork, I analyzed the monthly income statements through November, and they showed that the company operated at a loss almost every month! How did they report a substantial profit at year-end?" Logan replied, "Several years ago they made an investment in the stock of a closely held company that they thought might be a good strategic alliance. Unfortunately, that opportunity didn't work out. Until December 2018, CBF had been holding the investment and hadn't been receiving any dividends. The CFO of CBF actively searched for a company to buy the stock, and in December 2018, located a strategic buyer who took it off their hands at a substantial gain!" Logan continued. "Since CBF frequently buys and sells stock investments, the gain is a part of their income from continuing operations." "Oh, that's clever!" Jasmine responded. "But if it were such a large transaction, why didn't they just use the cash flow from the stock sale to finance the new manufacturing facility?" "Well," Logan explained, "the company that CBF sold the stock to, Easy Exchange, is having their own cash flow problems right now. They couldn't afford to give CBF cash, so CBF accepted a non-interest- bearing note due in 5 years. Although CBF won't see the cash for five years, since the title to the stock has passed to the new owners, it can record the gain on the sale." Jasmine pondered this information for a few minutes, and then queried, "Why a non-interest-bearing note? Most companies with a credit rating like Easy Exchange are paying about 15% on loans for transactions like this one." "CBF didn't have any loans against the investment, so they aren't incurring any interest cost on the stock or the new note. They figured that there isn't any need to hurt Easy Exchange's cash flow when CBF doesn't have any interest cost on the investment, Logan responded. "Logan, you sure know a lot about this transaction," teased Jasmine. "You'd think that you had found the buyer and negotiated the deal." "Well, I am pretty excited," Logan responded. "I worked with the CFO on the transaction, reviewing the entry in the general journal and its reporting in CBF's income statement. I may not have arranged the deal, but I was instrumental in getting out the audited statements just in time. As you know, CBF really needed some serious cash infusion as soon as possible from some lender to complete a production facility for that new circuit board." "Since I missed all the excitement while I was working on a different client, why don't you share the details of the transaction?" demanded Jasmine. "Well, CBF was carrying the investment at $6,600,000 and sold it to Easy Exchange for $10,000,000. So, they booked a $3,400,000 gain on the transaction," Logan confidentially replied. Jasmine looked troubled and finally confided to Logan, "I'm enrolled in a CPA review course, and last week we studied long-term receivables and payables. I learned that generally accepted accounting principles (GAAP) require notes receivable due in more than one year to be carried at their present value. Wouldn't that affect the profit you reported?" Logan looked at Jasmine like she was trying to put him on the spot and icily replied, "I explained that CBF didn't incur any interest on this investment before the sale, so present value calculations aren't necessary! And, yes, the income statement we audited is consistent with GAAP." Circuit Board Framework (CBF) Income Statements For the four years ended December 31, 2018 Net Revenues and Gains Expenses and Losses Cost of Sales Gross Profit Operating Expenses Other Expenses Net Income Before Taxes Taxes Net Income After Taxes Common Shares Outstanding 2018 2016 $30,250,000 $28,930,000 $27,610,000 $22,990,000 16,416,000 13,122,000 10,632,600 9,936,000 13,834,000 15,808,000 16,977,400 13,054,000 3,476,000 3,382,500 3,179,000 2,530,000 2,435,400 5,027,000 4,362,600 3,460,600 5,331,000 8,062,900 10,337,800 8,088,600 1,119,510 1,693,209 2,170,938 1,698,606 $4,211,490 $6,369,691 $8,166,862 $6,389,994 3,000,000 3,000,000 3,000,000 3,000,000 2017 2015

Expert Answer:

Answer rating: 100% (QA)

To determine whether Dash Spencer LLP breached its duty of care we need to analyze the accounting treatment of Circuit Board Framework CBFs stock sale ... View the full answer

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date:

Students also viewed these accounting questions

-

Which subject does Corporate social responsibility belong to?

-

The shoes on the brake depicted in the figure subtend a 90 arc on the drum of this external pivoted-shoe brake. The actuation force P is applied to the lever. The rotation direction of the drum is...

-

Greish Inc. is preparing its annual budgets for the year ending December 31, 2012. Accounting assistants have provided the following data: An accounting assistant has prepared the detailed...

-

Brooke Young runs Young Yachting Pty Ltd. Brooke is a graduate of a tourism and hospitality degree and offers a luxury fully catered yachting holiday experience that includes scuba diving, swimming...

-

Assume that you have been hired as a consultant by CGT, a major producer of chemicals and plastics, including plastic grocery bags, styrofoam cups, and fertilizers, to estimate the firms weighted...

-

How might they explain what they observed? https://www.youtube.com/watch?v=BoeDI-YkzI0 Construct an explanation for the investigation of sound and vibration shown in the video. You can make your own...

-

Capstone Case: Sunrise Bakery Expansion The Sunrise Bakery Corporation was originally founded in Houston, TX in 1991 by Griffin Harris, who currently serves as the company's Chief Executive Officer....

-

ARM assembly language to convert Integer, 1194684 to hexadecimal. The signature of the routine is char*int2hex(int convert) where: int convert = 1194684; The output must be in the format OXdddddddd I...

-

Boron trifluoride gas is collected at 8.0C in an evacuated flask with a measured volume of 40.0%. When all the gas has been collected, the pressure in the flask is measured to be 0.190atm. Calculate...

-

The Demand function for a product is given by: D(q)=0.0003q2 -0.04q + 23.56 where q is the number of units sold and D(q) is the corresponding price per unit, in dollars. A) What is the average rate...

-

Warnerwoods Company uses a perpetual inventory system. It entered into the following purchases and sales transactions for March. Date Activities Units Acquired at Cost Units Sold at Retail March 1...

-

The observation of a client s physical inventory is a mandatory auditing procedure when possible for the auditors to carry out and when inventories are material. Required: 1 - a . Why is the...

-

The University of Malaya Engineering Students Society is planning a six day trip to the national conference in Penang. For transportation, the group will rent a car from either the Motor Pool or a...

-

The following table summarizes the results of a study on SAT prep courses, comparing SAT scores of students in a private preparation class, a high school preparation class, and no preparation class....

-

Ball bearings are widely used in industrial applications. You work for an industrial food machinery manufacturer and your role is to design the driveshaft assembly on a new type of equipment that...

-

On April 30, 2010, Barack and George entered into a bet on the outcome of the 2010 Kentucky Derby. On January 28, 2011, Barack, who bet on the winner, approached George, seeking to collect the $3,000...

-

On December 2, 2010, Miles executed and delivered to Proctor a negotiable promissory note for $10,000, payable to Proctor or order, due March 2, 2011, with interest at 6 percent from maturity, in...

-

Hines stored her furniture, including a grand piano, in Arnetts warehouse. Needing more space, Arnett stored Hiness piano in Butlers warehouse next door. As a result of a fire, which occurred without...

-

For many years, womens professional basketball struggled for consistency in the United States. Since 1978, when the Womens Professional Basketball League (WBL) was formed, leagues have had difficulty...

-

What are the five forms of financing, and how is each used within sport?

-

That financial ratios are most valuable when viewed in comparison to the organizations historical ratio values and competitors values. Why is this context valuable when examining financial ratio...

Study smarter with the SolutionInn App