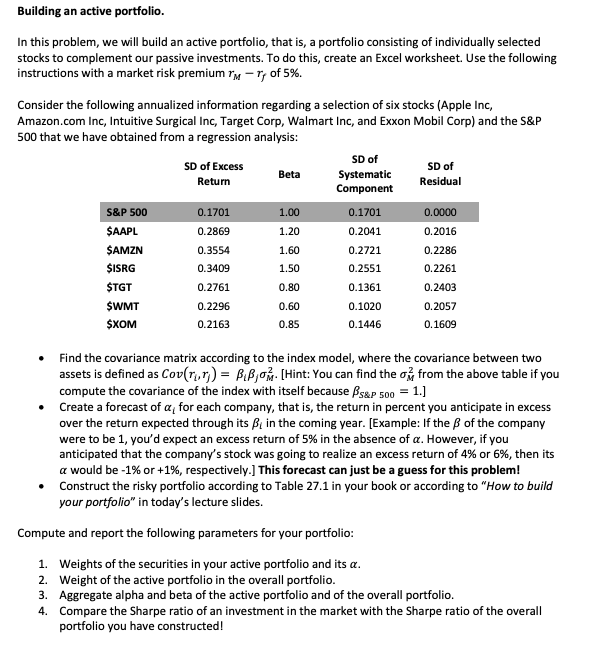

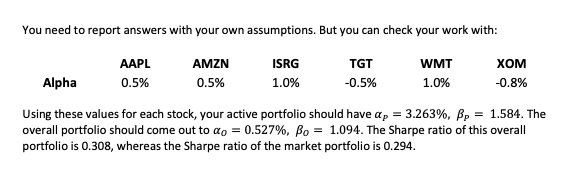

Building an active portfolio. In this problem, we will build an active portfolio, that is, a...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To solve this problem we can follow these steps 1 Calculate the covariance matrix according to the index model using the formula Covri rj i j 2 2 Crea... View the full answer

Related Book For

Probability and Random Processes With Applications to Signal Processing and Communications

ISBN: 978-0123869814

2nd edition

Authors: Scott Miller, Donald Childers

Posted Date: