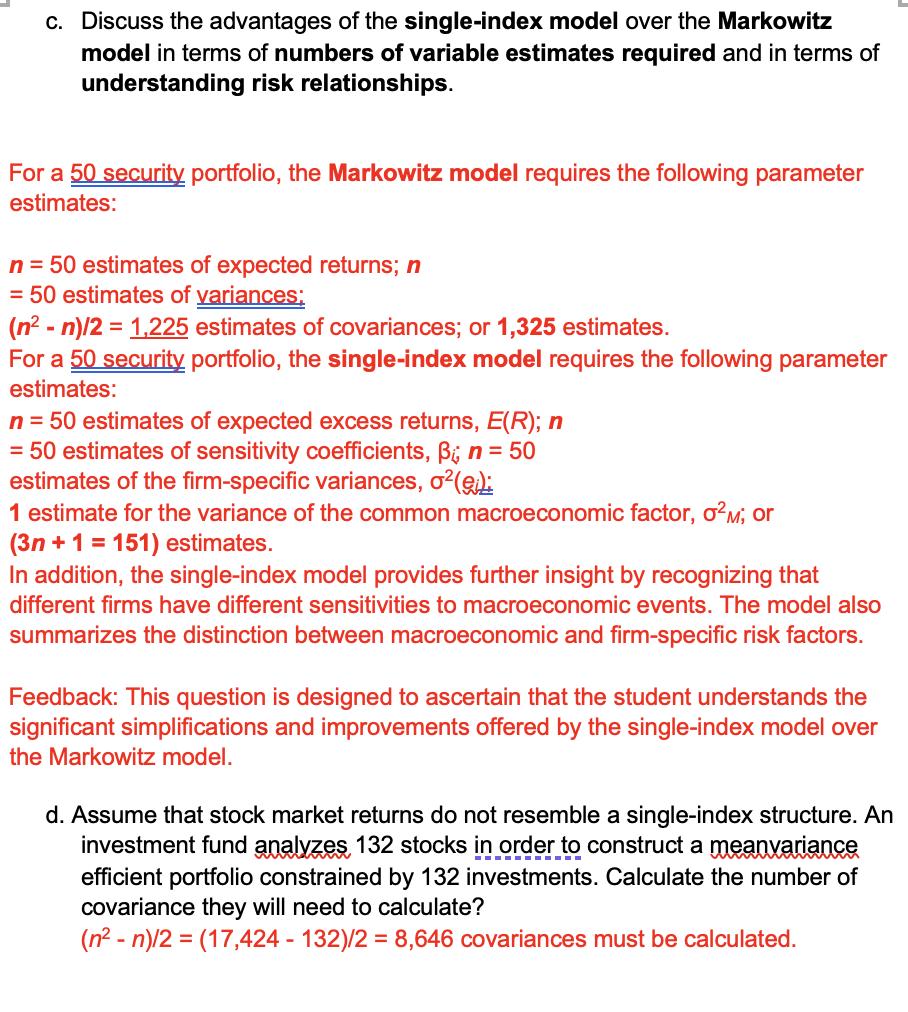

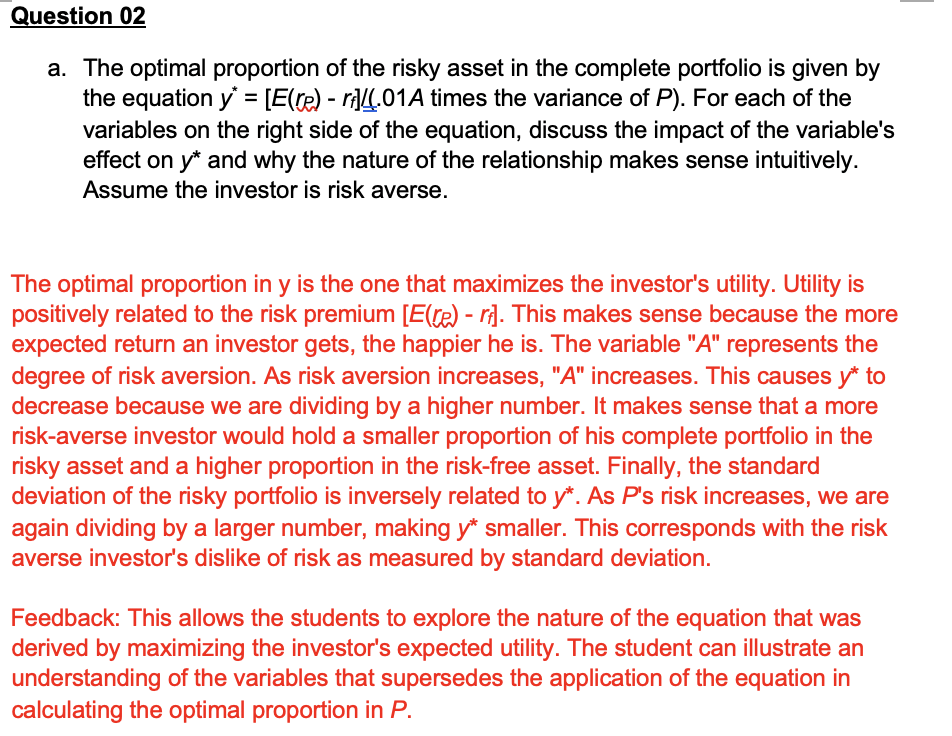

c. Discuss the advantages of the single-index model over the Markowitz model in terms of numbers...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

c The singleindex model offers several advantages over the Markowitz model in terms of the number of ... View the full answer

Related Book For

Elementary Surveying An Introduction to Geomatics

ISBN: 978-0273751441

13th Edition

Authors: Charles D. Ghilani, Paul R. Wolf

Posted Date: