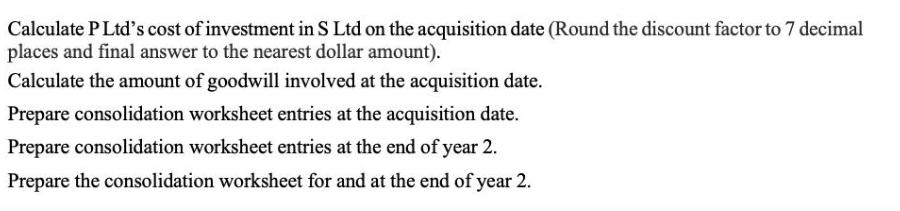

Calculate P Ltd's cost of investment in S Ltd on the acquisition date (Round the discount...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Solution PLads cost of investment in SLad on the acquisition date PLads cost of investment in SLad on the acquisition date can be calculated as follow... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: