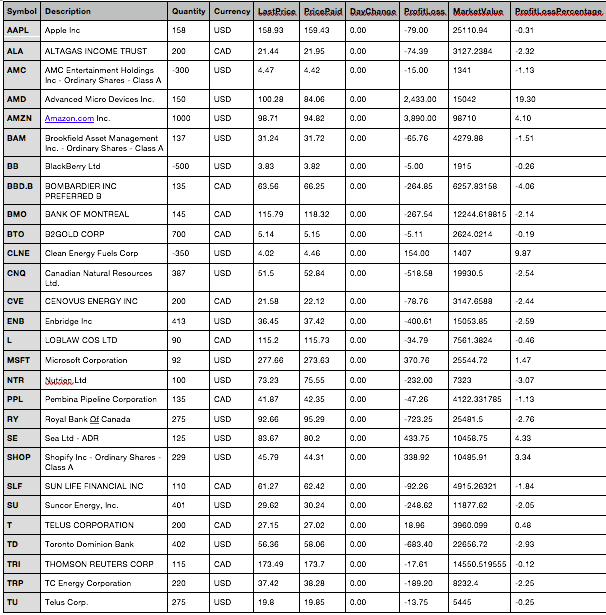

Calculate the treynor, sharpe, and jensen measures with a portfolio beta of 1.12 and a risk free

Fantastic news! We've Found the answer you've been seeking!

Question:

Calculate the treynor, sharpe, and jensen measures with a portfolio beta of 1.12 and a risk free rate of 2.90

Expert Answer:

Related Book For

Posted Date: