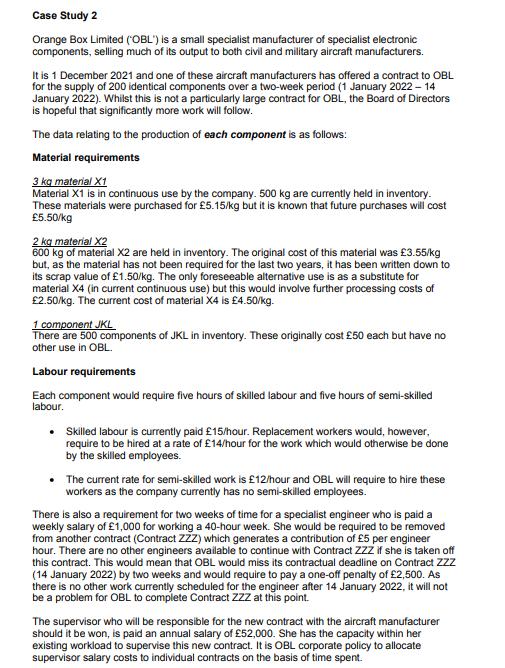

Case Study 2 Orange Box Limited (OBL') is a small specialist manufacturer of specialist electronic components,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

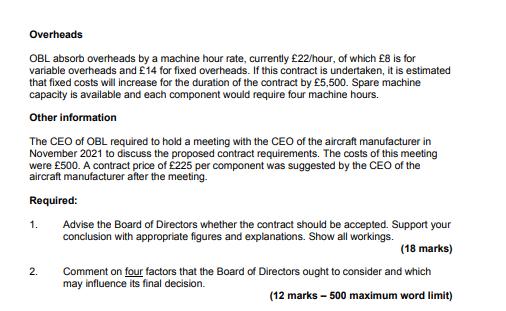

Case Study 2 Orange Box Limited (OBL') is a small specialist manufacturer of specialist electronic components, selling much of its output to both civil and military aircraft manufacturers. It is 1 December 2021 and one of these aircraft manufacturers has offered a contract to OBL for the supply of 200 identical components over a two-week period (1 January 2022 - 14 January 2022). Whilst this is not a particularly large contract for OBL, the Board of Directors is hopeful that significantly more work will follow. The data relating to the production of each component is as follows: Material requirements 3 kg material X1 Material X1 is in continuous use by the company. 500 kg are currently held in inventory. These materials were purchased for £5.15/kg but it is known that future purchases will cost £5.50/kg 2 kg material X2 600 kg of material X2 are held in inventory. The original cost of this material was £3.55/kg but, as the material has not been required for the last two years, it has been written down to its scrap value of £1.50/kg. The only foreseeable alternative use is as a substitute for material X4 (in current continuous use) but this would involve further processing costs of £2.50/kg. The current cost of material X4 is £4.50/kg. 1 component JKL There are 500 components of JKL in inventory. These originally cost £50 each but have no other use in OBL. Labour requirements Each component would require five hours of skilled labour and five hours of semi-skilled labour. • Skilled labour is currently paid £15/hour. Replacement workers would, however, require to be hired at a rate of £14/hour for the work which would otherwise be done by the skilled employees. The current rate for semi-skilled work is £12/hour and OBL will require to hire these workers as the company currently has no semi-skilled employees. There is also a requirement for two weeks of time for a specialist engineer who is paid a weekly salary of £1,000 for working a 40-hour week. She would be required to be removed from another contract (Contract ZZZ) which generates a contribution of £5 per engineer hour. There are no other engineers available to continue with Contract ZZZ if she is taken off this contract. This would mean that OBL would miss its contractual deadline on Contract ZZZ (14 January 2022) by two weeks and would require to pay a one-off penalty of £2,500. As there is no other work currently scheduled for the engineer after 14 January 2022, it will not be a problem for OBL to complete Contract ZZZ at this point. The supervisor who will be responsible for the new contract with the aircraft manufacturer should it be won, is paid an annual salary of £52,000. She has the capacity within her existing workload to supervise this new contract. It is OBL corporate policy to allocate supervisor salary costs to individual contracts on the basis of time spent. Overheads OBL absorb overheads by a machine hour rate, currently £22/hour, of which £8 is for variable overheads and £14 for fixed overheads. If this contract is undertaken, it is estimated that fixed costs will increase for the duration of the contract by £5,500. Spare machine capacity is available and each component would require four machine hours. Other information The CEO of OBL required to hold a meeting with the CEO of the aircraft manufacturer in November 2021 to discuss the proposed contract requirements. The costs of this meeting were £500. A contract price of £225 per component was suggested by the CEO of the aircraft manufacturer after the meeting. Required: 1. 2. Advise the Board of Directors whether the contract should be accepted. Support your conclusion with appropriate figures and explanations. Show all workings. (18 marks) Comment on four factors that the Board of Directors ought to consider and which may influence its final decision. (12 marks - 500 maximum word limit) Case Study 2 Orange Box Limited (OBL') is a small specialist manufacturer of specialist electronic components, selling much of its output to both civil and military aircraft manufacturers. It is 1 December 2021 and one of these aircraft manufacturers has offered a contract to OBL for the supply of 200 identical components over a two-week period (1 January 2022 - 14 January 2022). Whilst this is not a particularly large contract for OBL, the Board of Directors is hopeful that significantly more work will follow. The data relating to the production of each component is as follows: Material requirements 3 kg material X1 Material X1 is in continuous use by the company. 500 kg are currently held in inventory. These materials were purchased for £5.15/kg but it is known that future purchases will cost £5.50/kg 2 kg material X2 600 kg of material X2 are held in inventory. The original cost of this material was £3.55/kg but, as the material has not been required for the last two years, it has been written down to its scrap value of £1.50/kg. The only foreseeable alternative use is as a substitute for material X4 (in current continuous use) but this would involve further processing costs of £2.50/kg. The current cost of material X4 is £4.50/kg. 1 component JKL There are 500 components of JKL in inventory. These originally cost £50 each but have no other use in OBL. Labour requirements Each component would require five hours of skilled labour and five hours of semi-skilled labour. • Skilled labour is currently paid £15/hour. Replacement workers would, however, require to be hired at a rate of £14/hour for the work which would otherwise be done by the skilled employees. The current rate for semi-skilled work is £12/hour and OBL will require to hire these workers as the company currently has no semi-skilled employees. There is also a requirement for two weeks of time for a specialist engineer who is paid a weekly salary of £1,000 for working a 40-hour week. She would be required to be removed from another contract (Contract ZZZ) which generates a contribution of £5 per engineer hour. There are no other engineers available to continue with Contract ZZZ if she is taken off this contract. This would mean that OBL would miss its contractual deadline on Contract ZZZ (14 January 2022) by two weeks and would require to pay a one-off penalty of £2,500. As there is no other work currently scheduled for the engineer after 14 January 2022, it will not be a problem for OBL to complete Contract ZZZ at this point. The supervisor who will be responsible for the new contract with the aircraft manufacturer should it be won, is paid an annual salary of £52,000. She has the capacity within her existing workload to supervise this new contract. It is OBL corporate policy to allocate supervisor salary costs to individual contracts on the basis of time spent. Overheads OBL absorb overheads by a machine hour rate, currently £22/hour, of which £8 is for variable overheads and £14 for fixed overheads. If this contract is undertaken, it is estimated that fixed costs will increase for the duration of the contract by £5,500. Spare machine capacity is available and each component would require four machine hours. Other information The CEO of OBL required to hold a meeting with the CEO of the aircraft manufacturer in November 2021 to discuss the proposed contract requirements. The costs of this meeting were £500. A contract price of £225 per component was suggested by the CEO of the aircraft manufacturer after the meeting. Required: 1. 2. Advise the Board of Directors whether the contract should be accepted. Support your conclusion with appropriate figures and explanations. Show all workings. (18 marks) Comment on four factors that the Board of Directors ought to consider and which may influence its final decision. (12 marks - 500 maximum word limit)

Expert Answer:

Answer rating: 100% (QA)

1 The Board of Directors should accept the contract The total cost of the contract would be Material... View the full answer

Related Book For

A Survey Of Mathematics With Applications

ISBN: 9780135740460

11th Edition

Authors: Allen R. Angel, Christine D. Abbott, Dennis Runde

Posted Date:

Students also viewed these accounting questions

-

Bruces Bakery is thinking of making its own Danish pastries. Two machines, A and B, are being considered for purchase. Bruces now purchases the Danish pastries from an outside supplier for 20 cents...

-

JB Limited is a small specialist manufacturer of electronic components and much of its output is used by the makers of aircraft for both civil and military purposes. One of the few aircraft...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Julia Robertson is a senior at Tech, and she's investigating different ways to finance her final year at school. She is considering leasing a food booth outside the Tech stadium at home football...

-

Discuss the difference between goalpost conformance and absolute quality conformance.

-

On November 30, the end of the first month of operations, Weatherford Company prepared the following income statement, based on the absorption costing concept: If the fixed manufacturing costs were...

-

Wayflaire Inc. produces home products. The cost to manufacture a case ( 36 sets) of its most popular set of casual dinnerware is as follows: The average sales price for a case of dinnerware is \(\$...

-

Presented below is information related to the sole proprietorship of Alice Henning, attorney. Legal service revenue2017 ........ $ 335,000 Total expenses2017 ............ 211,000 Assets, January 1,...

-

Bandar Industries Berhad of Malaysia manufactures sporting equipment. One of the company's products, a football helmet for the North American market, requires a special plastic. During the quarter...

-

Fantastique Bikes is a company that manufactures bikes in a monopolistically competitive market. The following graph shows Fantastique?s demand curve, marginal revenue curve (MR), marginal cost curve...

-

Find the p-value for each test statistic. (round your answers to 4 decimal places.) Right-tailed test z=+2.82 Left-tailed test z=-1.28 Two-tailed test z=-1.55

-

Members X and Z form Rosmead Gardens LLC on January 1, 2024. Purpose of the LLC is to acquire an existing residential multifamily asset, known as Rosmead Gardens. The total cost of acquisition is...

-

Explain the components. Describe the task's role in OS security. Identify the major tasks of an OS. Examine how different networks are managed by the OS.? 1. process management, 2. memory management,...

-

Derive the probability distribution of the 1-year HPR on a 30-year U.S. Treasury bond with a 4.0% coupon if it is currently selling at par and the probability distribution of its yield to maturity a...

-

Johnson Inc.'s non-strategic investment portfolio at December 31, 2022, consisted of the following: Debt and Equity Investments* 10,600 Xavier Corp. common shares Cost $173,310 80,600 41,800 Fair...

-

How is it that price controls might cause shortages, and why do these shortages increase impact the availability of services? Many have suggested we limit drug prices. Will this work and what is the...

-

1. Consider a hypothetical country in Latin America or the Caribbean thet currently is experiending hyperinflation It is also on the brink of defaulting on its sovereign debt, most of which is...

-

Suppose you are comparing just two means. Among the possible statistics you could use is the difference in means, the MAD, or the max min (the difference between the largest mean and the smallest...

-

In Exercise fill in the blanks with an appropriate word, phrase, or symbol(s). In clock 12 arithmetic, since 1 + 11 = 11 + 1 = 12, we say that 1 and 11 are additive ________.

-

Fill in the blanks with an appropriate word, phrase, or symbol(s). If an Euler diagram can be drawn only in a way in which the conclusion necessarily follows from the premises, the syllogistic...

-

Determine the indicated term for the arithmetic sequence with the first term, a 1 , and common difference, d. Determine a 20 when a 1 = 4, d = 3.

-

IFRS and the CPA Canada Handbook, Part II, have equal status in Canada for financial reporting.

-

Any Canadian company that uses U.S. GAAP must prepare its statements in U.S. dollars.

-

In a private corporation, the needs of external users have no impact on the companys financial reporting objectives.

Study smarter with the SolutionInn App