City Art Gallery (CAG) is an Alberta not-for-profit organization managing the operations of a gallery with 65

Question:

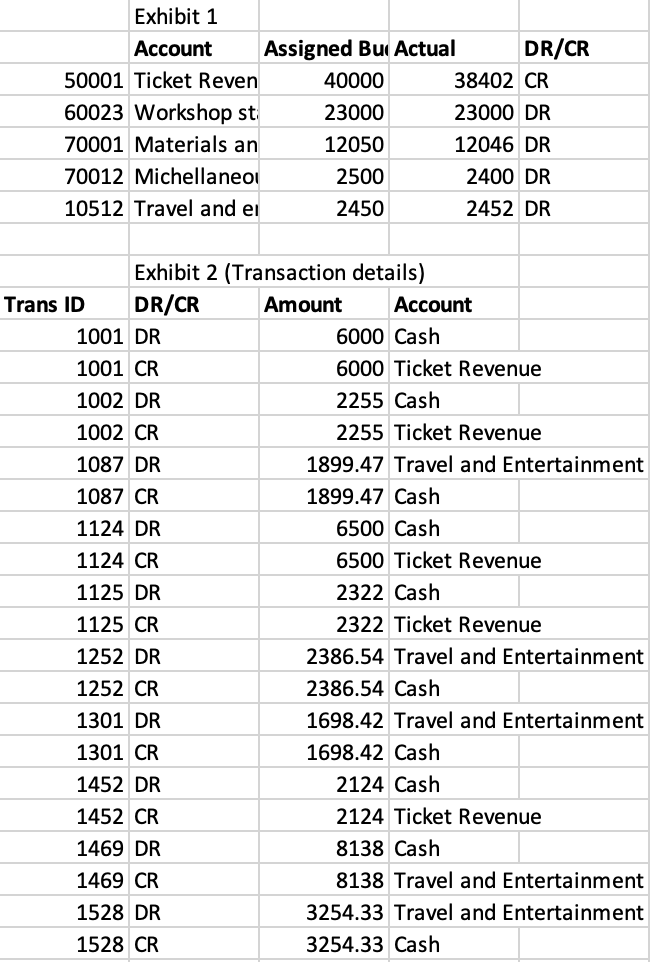

City Art Gallery (CAG) is an Alberta not-for-profit organization managing the operations of a gallery with 65 full-time employees and 25 volunteers. CAG is primarily funded by government grants, and an annual audit is a requirement for receiving some of the grants. Five years ago, the curator decided to organize regular workshops for adults and children to enhance their experience of various art exhibitions. The cost to attend these workshops range from $59.99 to $149.49 plus GST. The curator, Harvey, has assigned the entire operation Marvin,one of his trusted managers. The workshop program is supposed to be self-financing (i.e., it would not be allocated any has had to shift money from the operating fund to cover deficits in the workshop fund. The only source of revenue is fees collected from people attending the workshops. All revenue collected and expenses incurred are tracked through a special fund. The use of this fund facilitates budget reconciliations as the account balances can be easily traced. Marvin is responsible for entering the workshop transactions into the accounting system and is also in charge of collecting and depositing the fees. Harvey does not believe in micromanaging his staff and has never scrutinized the operations other than reviewing the annual audit report prepared for CAG. Recently, a couple of members of H mentioned the large number of people at the workshop. Harvey was puzzled, as Marvin had told him that attendance was expected to be much lower than originally forecasted. According to financial reportsfrom the past three years, revenue shortages were the cause of the deficits. Harvey decided to review the report from the current fiscal year (Exhibit 1).

In addition, Harvey reviewed the transactions that were used to compile the financial report line items listed in Exhibit 1. He discovered that, in at least one instance, revenue collected had been posted to the travel and entertainment account. The transactions in the travel and entertainment account were of particular interest to Harvey, as Marvin had travelled to Europe for research related to the workshops. The amount indicated on the financial report did not seem reasonable given the cost of a trip to Europe. Harvey has asked you to perform an analysis on the data to identify any weaknesses, errors in posting, or indications of potential fraud. Harvey has provided you with the following print-out (Exhibit 2) so that you can perform whatever analysis youdeem appropriate.

Harvey has traced all the cash debits in Exhibit 2 to deposits on the bank statements.

Required:

a)What observations can you draw from the data that Harvey has provided to you? (6marks)

b) Identify 4 control weaknesses you would include in a management letter

For each weakness,

i) discuss the implication of the weakness to the operations of CAG.(4marks)

ii) provide recommendations to be included in the management letter and discuss why these are appropriate. (4marks)

c)Harvey is concerned about whether fraud has taken place. CAG is required to have an annual audit for funding purposes and have received clean reports in the past. Harvey is concerned that the audits in the past years were not carried out appropriately

Expert Answer:

Modern Advanced Accounting In Canada

ISBN: 9781259066481

7th Edition

Authors: Hilton Murray, Herauf Darrell