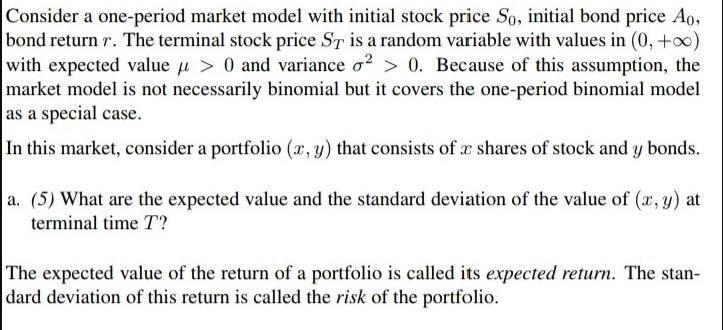

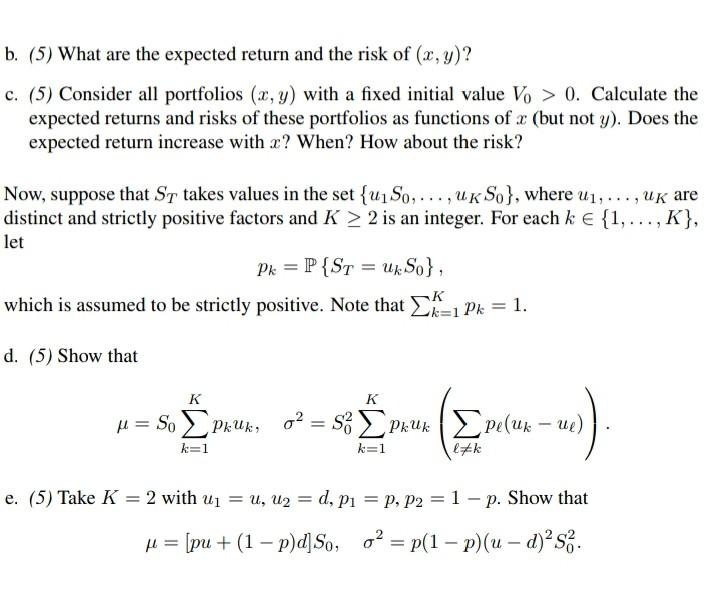

Consider a one-period market model with initial stock price So, initial bond price Ao, bond return...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION a To find the expected value and standard deviation of the portfolio x y at terminal time T we need to consider the expected value and varian... View the full answer

Related Book For

Calculus Of A Single Variable

ISBN: 9781337275361

11th Edition

Authors: Ron Larson, Bruce H. Edwards

Posted Date: