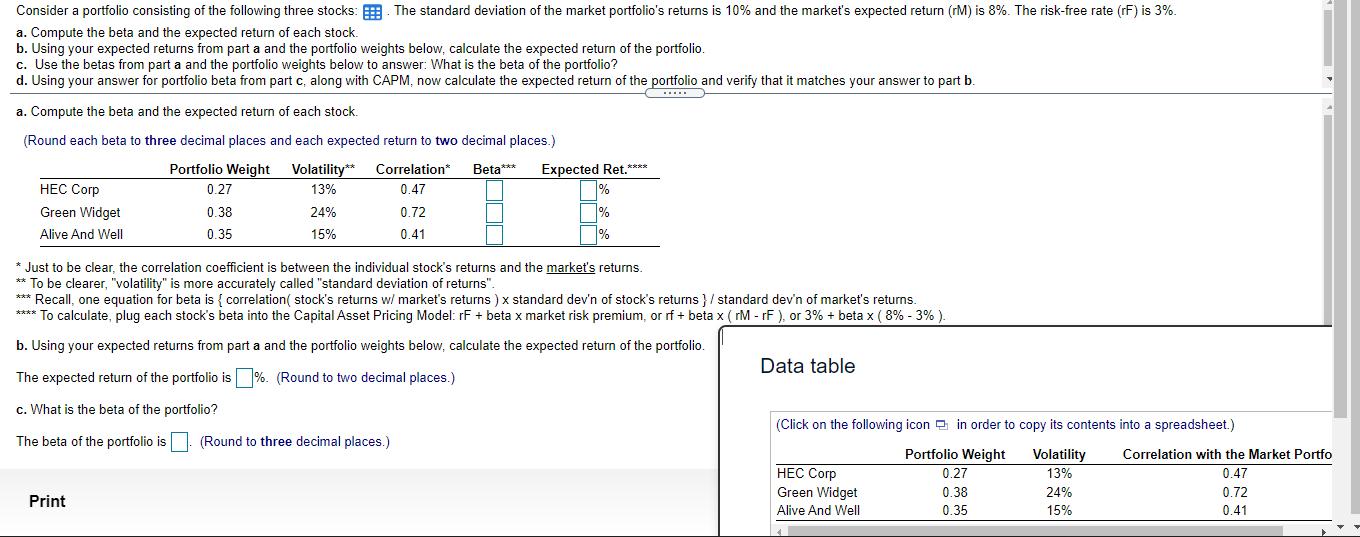

Consider a portfolio consisting of the following three stocks: a. Compute the beta and the expected...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Lets calculate the beta and expected return of each stock first a Compute the beta and the expected return of each stock 1 For HEC Corp Beta HEC Corp ... View the full answer

Related Book For

Posted Date: