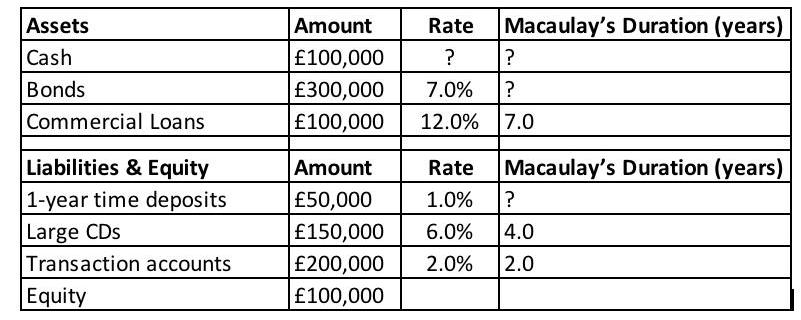

Consider the following summarised balance-sheet and associated average interest rates of a bank. The bank holds zero-coupon

Fantastic news! We've Found the answer you've been seeking!

Question:

Consider the following summarised balance-sheet and associated average interest rates of a bank. The bank holds zero-coupon bonds that have a 4-year maturity with a 7% discount rate. Amounts in the balance-sheet represent current market values.

- Required

- Give two practical recommendations to this bank in terms of minimizing its interest rate risk exposure without changing the size of its balance-sheet.

- Calculate the Macaulay’s Duration for the bank’s bonds.

- Calculate the duration GAP for the bank and the corresponding change in its equity if interest rates were to fall by 3 percentage points.

- Give two practical recommendations to this bank in terms of minimizing its interest rate risk exposure without changing the size of its balance-sheet.

Expert Answer:

To provide practical recommendations to the bank for minimizing interest rate risk exposure without changing the size of its balance sheet here are tw... View the full answer

Related Book For

Posted Date: