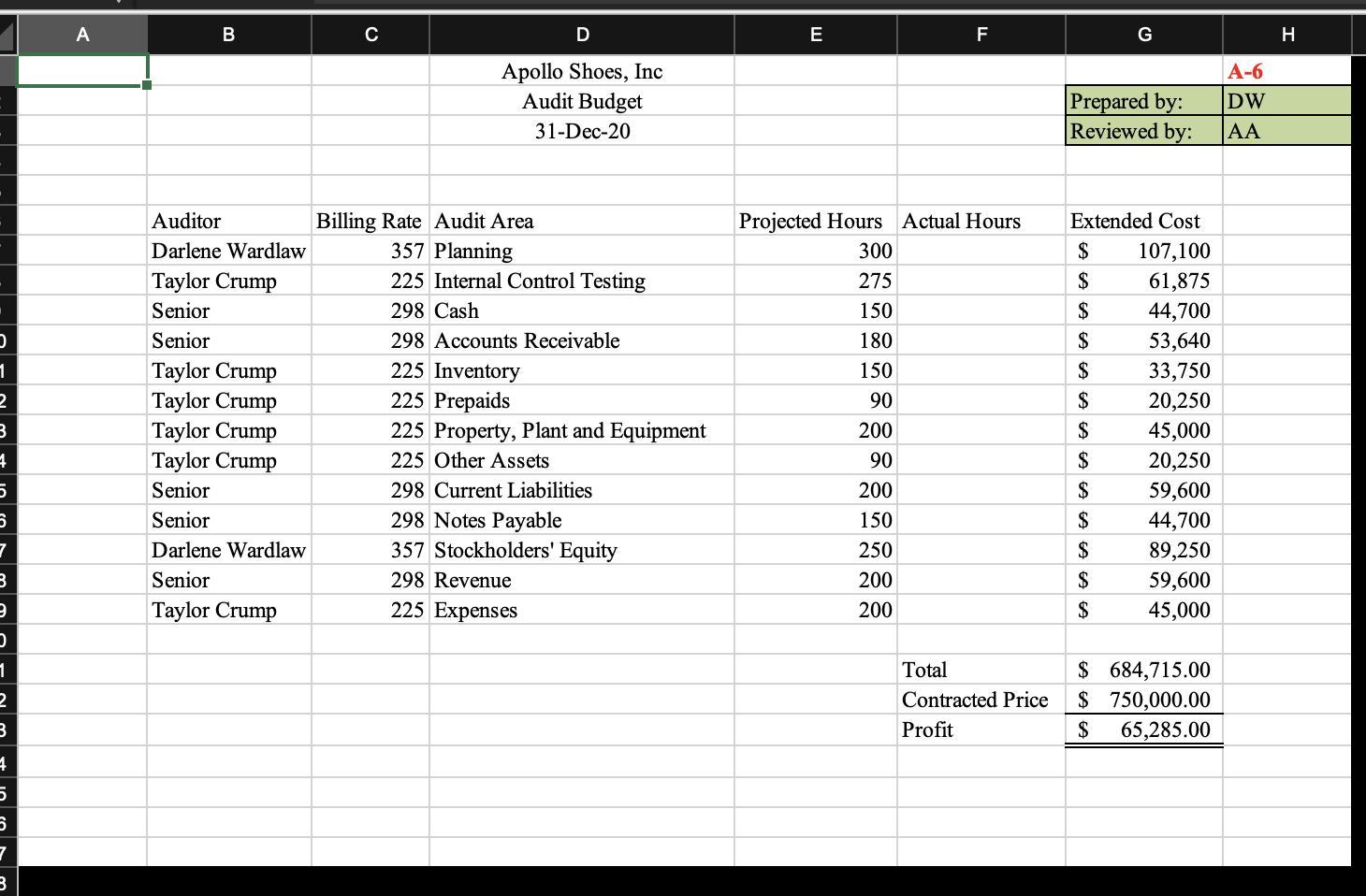

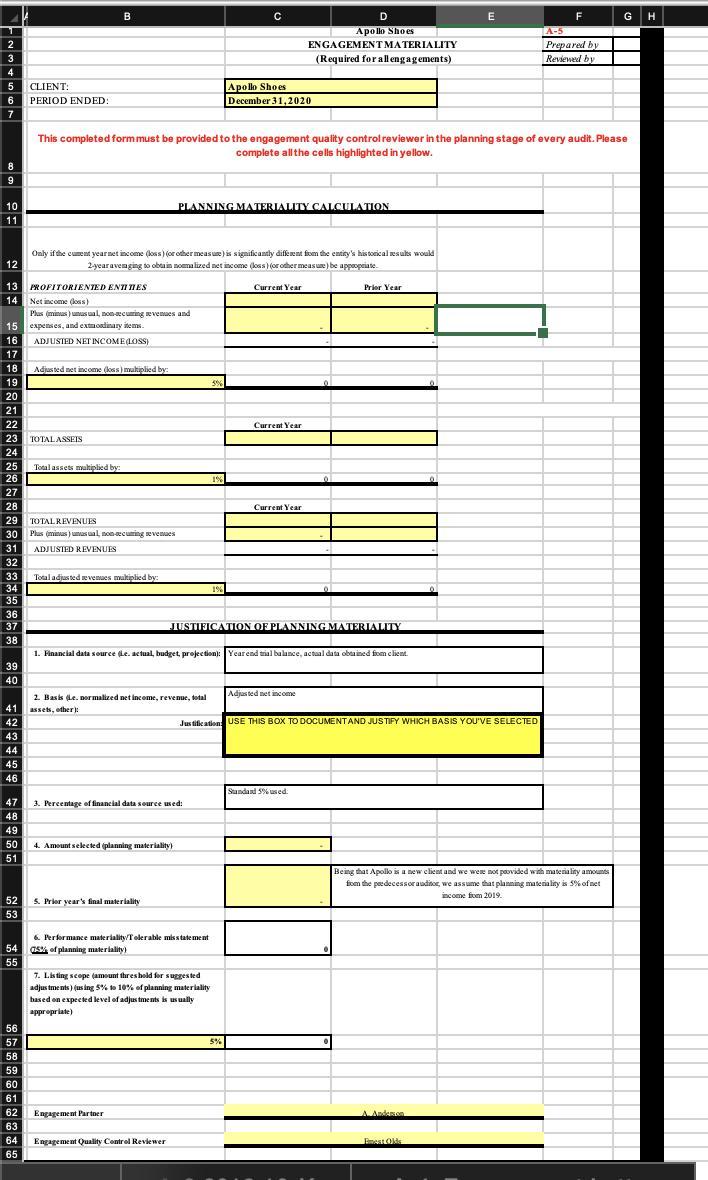

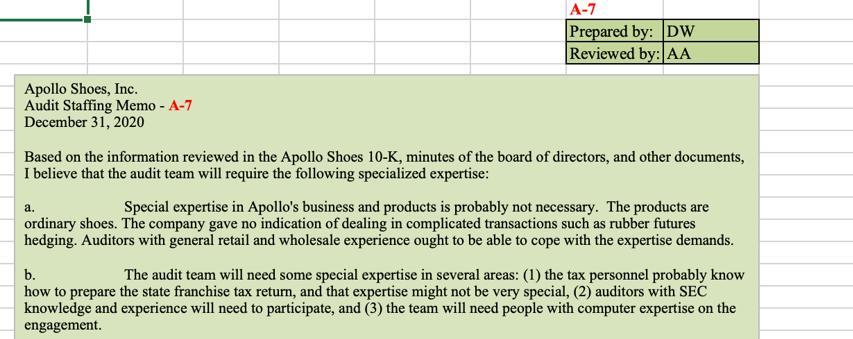

Determine staffing assignments based on consideration of audit risks, and discuss the preliminary audit plan and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text: