Dexter Jennings founded Harding Developments Limited (HDL) under federal law in 1966. The business started off as

Question:

Dexter Jennings founded Harding Developments Limited (HDL) under federal law in 1966. The business started off as a modest home construction. However, HDL quickly rose to prominence as a major developer of commercial, industrial, and residential developments after investing its large earnings in land.

Dexter Jennings, who was 83 years old when he passed away on February 15, 20X1, appointed Wendy Boucher as his estate's administrator. Since HDL's establishment, attorney Boucher has served as the company's in-house legal counsel. Boucher and Jennings collaborated closely on all significant business decisions.

However, all final decisions were made by Jennings who was directly involved in the running of his company up to the date of his death, even though the loss of his eyesight had made this increasingly difficult.

Boucher has now approached your firm, O'Neill & Scott Chartered Professional Accountants (O&S), for advice. O&S has provided a complete range of services to Jennings since 1972, including financial and management accounting, tax advice (including the preparation of all tax returns), and the audit of HDL.

As executor of the estate, Boucher would like O&S to provide her with direction on the tax issues that she needs to address and the most tax-effective ways of dealing with the problems she faces. She informs you that, as executor, she has complete responsibility for the affairs of the late Dexter Jennings, including control of HDL and all his personal affairs. Accordingly, she wants her decisions to reflect judgment beyond reproach.

The O&S partner on the engagement has asked you, CPA, to prepare a draft report to Wendy Boucher addressing all pertinent issues.From your review of the files and brief discussion with Wendy Boucher, you are aware of the

following:

1. Jennings' wife passed away many years ago.

2. Excerpts of Jennings' will read as follows:

"All of my net assets shall remain in the custody of my executor (Wendy Boucher) for five years after the date of my death, except as otherwise provided under this last will and testament. During this time the executor shall liquidate all of my personal assets at their fair market value."

"Distribution to my grandchildren shall be as follows:

a) an amount not exceeding $100,000 annually per grandchild. Distribution shall be made at the discretion of the executor and in the manner prescribed by the executor.

b) at the expiration of five years after my death, the shares of HDL and any other residual assets of my estate shall be distributed equally amongst my grandchildren."

3. Jennings' three children, aged 52, 55 and 63, are not entitled to receive any assets as a result of Jennings's death since each received $2 million three years ago.

4. The common shares of HDL are owned 50% by the estate of Dexter Jennings, 20% by Jonathan Rothschild, and 30% by the 13 grandchildren.

5. Jonathan Rothschild was a business associate and long-time personal friend of Dexter Jennings and amassed considerable wealth through his own real estate development ventures. However, his own businesses have recently run into financial difficulty. As a result, he urgently needs funds.

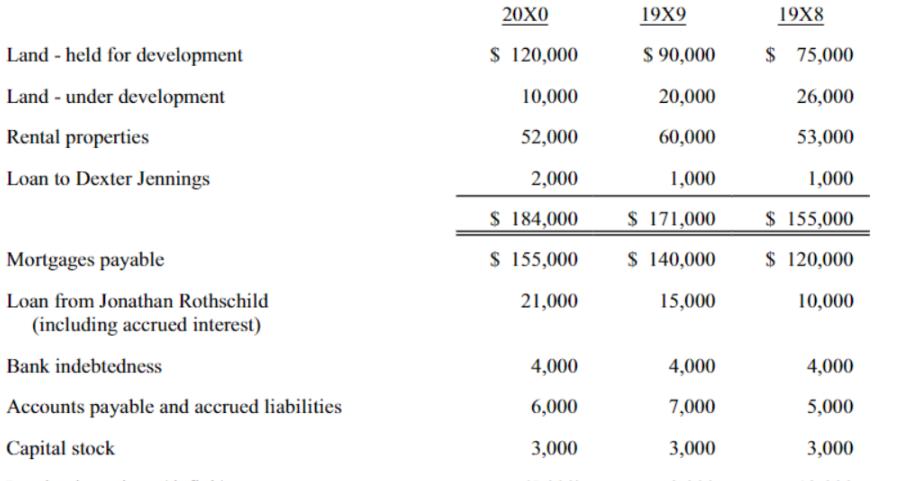

6. The balance sheet of HDL is summarized as follows (in thousands of dollars):

7. The taxable income of HDL reported for the last seven years is as follows (in thousands of

dollars):

20X0 19X9 19X8 19X7 19X6 19X5 19X4

Taxable income (loss) (6,000) 3,000 6,000 10,000 10,000 8,000 7,000

8. HDL's capital dividend account totaled $650,000 at the end of 20X0.

9. In January 20X1, HDL sold properties that results in a gain of $3.1 million. However, the proceeds are receivable over seven years

10. HDL received $300,000 in life insurance proceeds as a result of the death of Jennings.

11. HDL had provided Jennings with a car as well as a driver. Jennings lived in a condominium owned by HDL and rented it for $1 per annum.

12. The loan from Jonathan Rothschild to HDL bears interest at 4% and is repayable upon demand.

13. The Jennings grandchildren hold their investment in HDL through Third Generation, Investments Inc.

14. Boucher keeps in constant contact with the family members. She tries to keep them informed of what she is doing and asks for their opinion on major issues.

15. Jennings had not used any of its capital gains exemption. He did not have a balance in his cumulative net investment loss account, nor had he ever claimed an allowable business investment loss.

16. Shortly after Jennings died, some of the grandchildren requested a cash distribution from the estate.

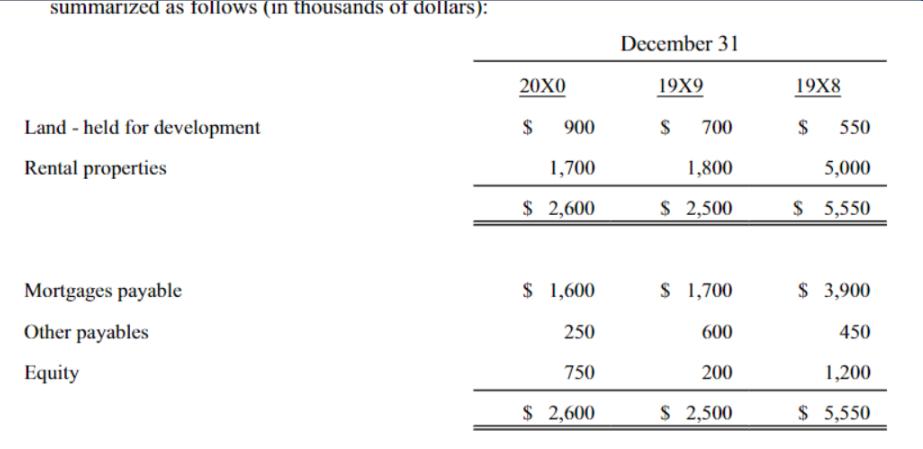

17. Jennings was the sole shareholder of Dexter Ltd. The balance sheet of Dexter Ltd. is summarized as follows (in thousands of dollars)

18. The taxable income of Dexter Ltd. for the last seven years is as follows (in thousands of

18. The taxable income of Dexter Ltd. for the last seven years is as follows (in thousands of

dollars):

20X0 19X9 19X8 19X7 19X6 19X5 19X4

Taxable income (loss) 1,000 (1,500) (5,000) (3,000) (2,000) (6,000) (7,000)

19. Jennings personally owned a condominium in Florida and one in London, England, both of which he visited regularly until his death. Dexter Jennings purchased these properties in 1980. Boucher is in the process of selling these condominiums. She has received an offer of $US120,000 for the Florida condominium and US$475,000 for the London condominium. Commission costs would amount to 5% and 4% respectively. However, Jennings' eldest son has threatened to sue Boucher if she sells either of these properties since, in his words, "Dad wanted them to remain in the family".

20. Other than the above noted items, Jennings' personal assets are limited to personal effects and a bank account with a nominal balance.

Required:

Prepare the report to Wendy Boucher.

Expert Answer:

ONeill Scott Chartered Professional Accountants Draft Report to Wendy Boucher Dear Ms Boucher Subject Tax Issues and Recommendations for Dexter Jennin... View the full answer

Advanced Financial Accounting

ISBN: 978-0137030385

6th edition

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay