Electro-Phi Inc. (the Company) is a utility provider that sells electricity to the public. The Company...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

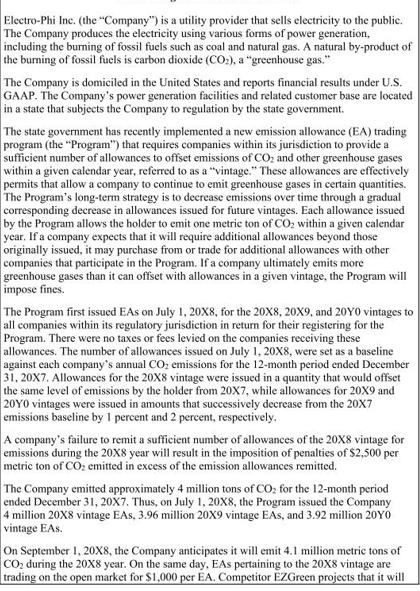

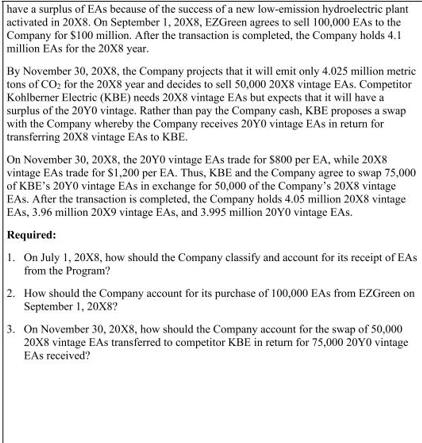

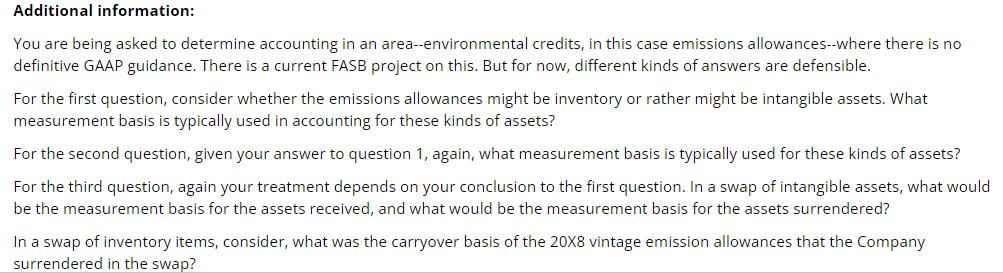

Electro-Phi Inc. (the "Company") is a utility provider that sells electricity to the public. The Company produces the electricity using various forms of power generation, including the burning of fossil fuels such as coal and natural gas. A natural by-product of the burning of fossil fuels is carbon dioxide (CO₂), a "greenhouse gas." The Company is domiciled in the United States and reports financial results under U.S. GAAP. The Company's power generation facilities and related customer base are located in a state that subjects the Company to regulation by the state government. The state government has recently implemented a new emission allowance (EA) trading program (the "Program") that requires companies within its jurisdiction to provide a sufficient number of allowances to offset emissions of CO₂ and other greenhouse gases within a given calendar year, referred to as a "vintage." These allowances are effectively permits that allow a company to continue to emit greenhouse gases in certain quantities. The Program's long-term strategy is to decrease emissions over time through a gradual corresponding decrease in allowances issued for future vintages. Each allowance issued by the Program allows the holder to emit one metric ton of CO₂ within a given calendar year. If a company expects that it will require additional allowances beyond those originally issued, it may purchase from or trade for additional allowances with other companies that participate in the Program. If a company ultimately emits more greenhouse gases than it can offset with allowances in a given vintage, the Program will impose fines. The Program first issued EAs on July 1, 20X8, for the 20X8, 20X9, and 20Y0 vintages to all companies within its regulatory jurisdiction in return for their registering for the Program. There were no taxes or fees levied on the companies receiving these allowances. The number of allowances issued on July 1, 20X8, were set as a baseline against each company's annual CO₂ emissions for the 12-month period ended December 31, 20X7. Allowances for the 20X8 vintage were issued in a quantity that would offset the same level of emissions by the holder from 20X7, while allowances for 20X9 and 20Y0 vintages were issued in amounts that successively decrease from the 20X7 emissions baseline by 1 percent and 2 percent, respectively. A company's failure to remit a sufficient number of allowances of the 20X8 vintage for emissions during the 20X8 year will result in the imposition of penalties of $2,500 per metric ton of CO₂ emitted in excess of the emission allowances remitted. The Company emitted approximately 4 million tons of CO₂ for the 12-month period ended December 31, 20X7. Thus, on July 1, 20X8, the Program issued the Company 4 million 20X8 vintage EAs. 3.96 million 20X9 vintage EAs, and 3.92 million 20Y0 vintage EAs. On September 1, 20X8, the Company anticipates it will emit 4.1 million metric tons of CO₂ during the 20X8 year. On the same day, EAs pertaining to the 20X8 vintage are trading on the open market for $1,000 per EA. Competitor EZGreen projects that it will have a surplus of EAs because of the success of a new low-emission hydroelectric plant activated in 20X8. On September 1, 20X8, EZGreen agrees to sell 100,000 EAs to the Company for $100 million. After the transaction is completed, the Company holds 4.1 million EAs for the 20X8 year. By November 30, 20X8, the Company projects that it will emit only 4.025 million metric tons of CO₂ for the 20X8 year and decides to sell 50,000 20X8 vintage EAs. Competitor Kohlberner Electric (KBE) needs 20X8 vintage EAs but expects that it will have a surplus of the 20Y0 vintage. Rather than pay the Company cash, KBE proposes a swap with the Company whereby the Company receives 20Y0 vintage EAs in return for transferring 20X8 vintage EAs to KBE. On November 30, 20X8, the 20Y0 vintage EAs trade for $800 per EA, while 20X8 vintage EAs trade for $1,200 per EA. Thus, KBE and the Company agree to swap 75,000 of KBE's 20Y0 vintage EAs in exchange for 50,000 of the Company's 20X8 vintage EAS. After the transaction is completed, the Company holds 4.05 million 20X8 vintage EAS, 3.96 million 20X9 vintage EAS, and 3.995 million 20Y0 vintage EAs. Required: 1. On July 1, 20X8, how should the Company classify and account for its receipt of EAS from the Program? 2. How should the Company account for its purchase of 100,000 EAs from EZGreen on September 1, 20X8? 3. On November 30, 20X8, how should the Company account for the swap of 50,000 20X8 vintage EAs transferred to competitor KBE in return for 75,000 20Y0 vintage EAs received? Additional information: You are being asked to determine accounting in an area--environmental credits, in this case emissions allowances--where there is no definitive GAAP guidance. There is a current FASB project on this. But for now, different kinds of answers are defensible. For the first question, consider whether the emissions allowances might be inventory or rather might be intangible assets. What measurement basis is typically used in accounting for these kinds of assets? For the second question, given your answer to question 1, again, what measurement basis is typically used for these kinds of assets? For the third question, again your treatment depends on your conclusion to the first question. In a swap of intangible assets, what would be the measurement basis for the assets received, and what would be the measurement basis for the assets surrendered? In a swap of inventory items, consider, what was the carryover basis of the 20X8 vintage emission allowances that the Company surrendered in the swap? Electro-Phi Inc. (the "Company") is a utility provider that sells electricity to the public. The Company produces the electricity using various forms of power generation, including the burning of fossil fuels such as coal and natural gas. A natural by-product of the burning of fossil fuels is carbon dioxide (CO₂), a "greenhouse gas." The Company is domiciled in the United States and reports financial results under U.S. GAAP. The Company's power generation facilities and related customer base are located in a state that subjects the Company to regulation by the state government. The state government has recently implemented a new emission allowance (EA) trading program (the "Program") that requires companies within its jurisdiction to provide a sufficient number of allowances to offset emissions of CO₂ and other greenhouse gases within a given calendar year, referred to as a "vintage." These allowances are effectively permits that allow a company to continue to emit greenhouse gases in certain quantities. The Program's long-term strategy is to decrease emissions over time through a gradual corresponding decrease in allowances issued for future vintages. Each allowance issued by the Program allows the holder to emit one metric ton of CO₂ within a given calendar year. If a company expects that it will require additional allowances beyond those originally issued, it may purchase from or trade for additional allowances with other companies that participate in the Program. If a company ultimately emits more greenhouse gases than it can offset with allowances in a given vintage, the Program will impose fines. The Program first issued EAs on July 1, 20X8, for the 20X8, 20X9, and 20Y0 vintages to all companies within its regulatory jurisdiction in return for their registering for the Program. There were no taxes or fees levied on the companies receiving these allowances. The number of allowances issued on July 1, 20X8, were set as a baseline against each company's annual CO₂ emissions for the 12-month period ended December 31, 20X7. Allowances for the 20X8 vintage were issued in a quantity that would offset the same level of emissions by the holder from 20X7, while allowances for 20X9 and 20Y0 vintages were issued in amounts that successively decrease from the 20X7 emissions baseline by 1 percent and 2 percent, respectively. A company's failure to remit a sufficient number of allowances of the 20X8 vintage for emissions during the 20X8 year will result in the imposition of penalties of $2,500 per metric ton of CO₂ emitted in excess of the emission allowances remitted. The Company emitted approximately 4 million tons of CO₂ for the 12-month period ended December 31, 20X7. Thus, on July 1, 20X8, the Program issued the Company 4 million 20X8 vintage EAs. 3.96 million 20X9 vintage EAs, and 3.92 million 20Y0 vintage EAs. On September 1, 20X8, the Company anticipates it will emit 4.1 million metric tons of CO₂ during the 20X8 year. On the same day, EAs pertaining to the 20X8 vintage are trading on the open market for $1,000 per EA. Competitor EZGreen projects that it will have a surplus of EAs because of the success of a new low-emission hydroelectric plant activated in 20X8. On September 1, 20X8, EZGreen agrees to sell 100,000 EAs to the Company for $100 million. After the transaction is completed, the Company holds 4.1 million EAs for the 20X8 year. By November 30, 20X8, the Company projects that it will emit only 4.025 million metric tons of CO₂ for the 20X8 year and decides to sell 50,000 20X8 vintage EAs. Competitor Kohlberner Electric (KBE) needs 20X8 vintage EAs but expects that it will have a surplus of the 20Y0 vintage. Rather than pay the Company cash, KBE proposes a swap with the Company whereby the Company receives 20Y0 vintage EAs in return for transferring 20X8 vintage EAs to KBE. On November 30, 20X8, the 20Y0 vintage EAs trade for $800 per EA, while 20X8 vintage EAs trade for $1,200 per EA. Thus, KBE and the Company agree to swap 75,000 of KBE's 20Y0 vintage EAs in exchange for 50,000 of the Company's 20X8 vintage EAS. After the transaction is completed, the Company holds 4.05 million 20X8 vintage EAS, 3.96 million 20X9 vintage EAS, and 3.995 million 20Y0 vintage EAs. Required: 1. On July 1, 20X8, how should the Company classify and account for its receipt of EAS from the Program? 2. How should the Company account for its purchase of 100,000 EAs from EZGreen on September 1, 20X8? 3. On November 30, 20X8, how should the Company account for the swap of 50,000 20X8 vintage EAs transferred to competitor KBE in return for 75,000 20Y0 vintage EAs received? Additional information: You are being asked to determine accounting in an area--environmental credits, in this case emissions allowances--where there is no definitive GAAP guidance. There is a current FASB project on this. But for now, different kinds of answers are defensible. For the first question, consider whether the emissions allowances might be inventory or rather might be intangible assets. What measurement basis is typically used in accounting for these kinds of assets? For the second question, given your answer to question 1, again, what measurement basis is typically used for these kinds of assets? For the third question, again your treatment depends on your conclusion to the first question. In a swap of intangible assets, what would be the measurement basis for the assets received, and what would be the measurement basis for the assets surrendered? In a swap of inventory items, consider, what was the carryover basis of the 20X8 vintage emission allowances that the Company surrendered in the swap?

Expert Answer:

Answer rating: 100% (QA)

1 On July 1 20X8 the Company should classify and account for its receipt of emission allowances EAs from the Program based on the nature of the allowances and the applicable accounting treatment Since ... View the full answer

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date:

Students also viewed these accounting questions

-

The management of WPB Ltd. has spent the past year reorganizing the companys business activities. The company is a service provider to hospitals. Originally the company operated only in Canada, where...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

On the basis of the given scenario create a file Expenses.txt, Open the file and copy it into another Expenses2.txt, Also show output on screen A college has announced a total budget of 50,000Rs.for...

-

Some corporations have issued perpetual warrants. Warrants are call options issued by a firm, allowing the warrant-holder to buy the firms stock.. For now, just consider a perpetual call. (a) What...

-

Compare and contrast 1245 depreciation recapture and 1250 depreciation recapture.

-

State the advantages of high-pressure boilers. Explain the construction and working of Babcock and Wilcox boiler with a neat sketch.

-

Robert Helmer and Percy Helmer, Jr., were authorized signatories on the corporate checking account of Event Marketing, Inc. The Helmers signed a check drawn on Event Marketings account and issued to...

-

Two resultant forces 100kN and Q kN acting at a point at an angle 90 between them. If resultant force is 200kN, find value of Q. Also find angle made by resultant with 100kN force?

-

Krause Industries' balance sheet at December 31, 2021, is presented here. Budgeted data for the year 2022 include the following. To meet sales requirements and to have 2,500 units of finished goods...

-

Viara owns a whole life policy. Viara does not currently have financial difficulties but would like to ensure that her policy is creditor protected. Which of the following options below will meet her...

-

Drewsbury (Pty) Ltd is a company located in Cape Town that manufactures cement and building accessories. The following information is available for the year ended 28 February 2023 (all amounts...

-

Remember the Tax Tip: When itemized deductions are greater than the standard deduction, use the itemized deductions instead of the standard deduction. Scenario Taxpayer is single with eligible...

-

Take a moment now to reflect on a time when you underwent a performance review at work. Reflecting on that experience, consider the following: What was the format of the performance review? For...

-

Evaluate the following code Interfaces.java Create a java program using interfaces to display your textbook information: 1.- Textbook: Title, Author, year of publication, and edition Important: extra...

-

Crane Tar and Gravel Ltd. operates a road construction business. In its first year of operations, the company won a contract to build a road for the municipality of Cochrane West. It is estimated...

-

Problem 1 Sketch the block diagram for the following third order systemusing integrator block method. Label all blocks and signal pathvariables. 2y'''+10y'+48y=0.8u

-

The Taylor's series expansion for cosx about x = 0 is given by: where x is in radians. Write a user-defined function that determines cosx using Taylor's series expansion. For function name and...

-

Johnson, president of the First National Bank of A, believes that it is appropriate to employ only female tellers. Hence, First National refuses to employ Ken Baker as a teller but does offer him a...

-

Anita and Barry were negotiating, and Anitas attorney prepared a long and carefully drawn contract, which was given to Barry for examination. Five days later and prior to its execution, Barrys eyes...

-

Civil Code 1719, subdivision (a) provides in part that any person who draws a check that is dishonored due to insufficient funds shall be liable to the payee for the amount owing upon the check and...

-

Which ETF in Exhibit 1 is most likely to have the lowest tracking error? A. ETF 2 B. ETF 3 C. ETF 4 Howie Rutledge is a senior portfolio strategist for an endowment fund. Rutledge meets with recently...

-

Given the current pricing of ETF 1, the most likely transaction to occur is that: A. new ETF shares will be created by the APs. B. redemption baskets will be received by APs from the ETF sponsor. C....

-

Stosurs statement about quoted bidask spreads is incorrect with respect to the: A. amount of the ongoing order flow in the ETF. B. costs and risks for the ETF liquidity providers. C. amount of...

Study smarter with the SolutionInn App