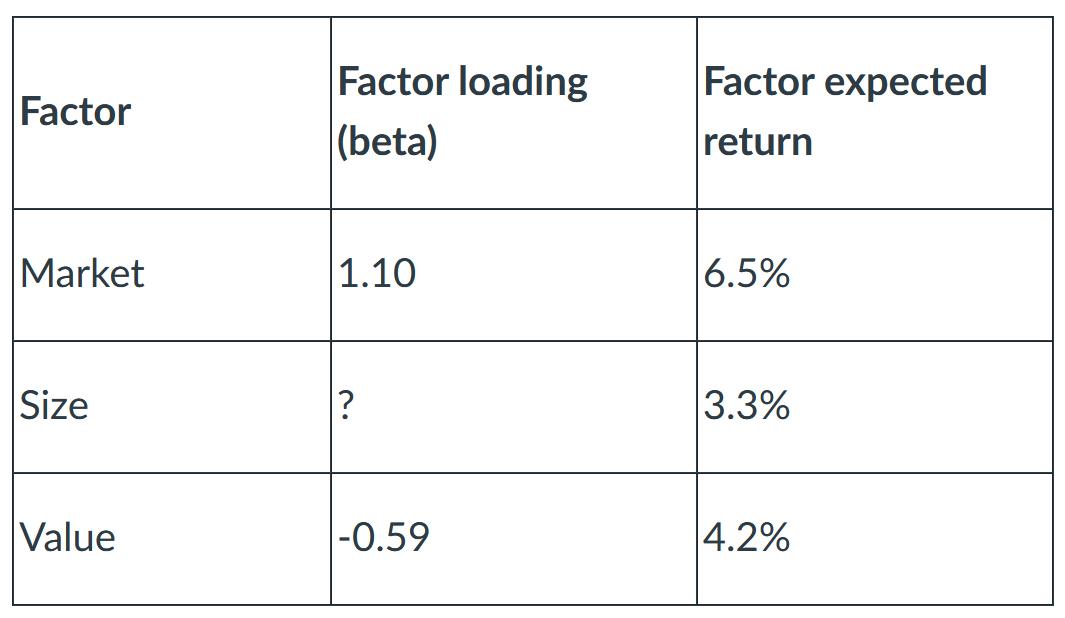

Estimated factor loadings (betas) for the Mystery Fund, according to the Fama-French 3 Factor model (FF3), are

Fantastic news! We've Found the answer you've been seeking!

Question:

Estimated factor loadings (betas) for the Mystery Fund, according to the Fama-French 3 Factor model (FF3), are reported in the table below, along with annual factor expected returns.

If the Mystery Fund's annual return was 10%, its FF3 alpha was 5%, and the risk-free rate was 2% over the same period, what was the fund's FF3 size beta?

Expert Answer:

Answer We can use the information provided to solve for the FF3 size beta of the Mystery Fund Heres ... View the full answer

Related Book For

Introduction To Probability And Statistics

ISBN: 9780495389538

13th Edition

Authors: William Mendenhall, Robert J. Beaver, Barbara M. Beaver

Posted Date: