= = Exercise 1.5. In Example 1.2.4, we considered an agent who sold the look- back...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

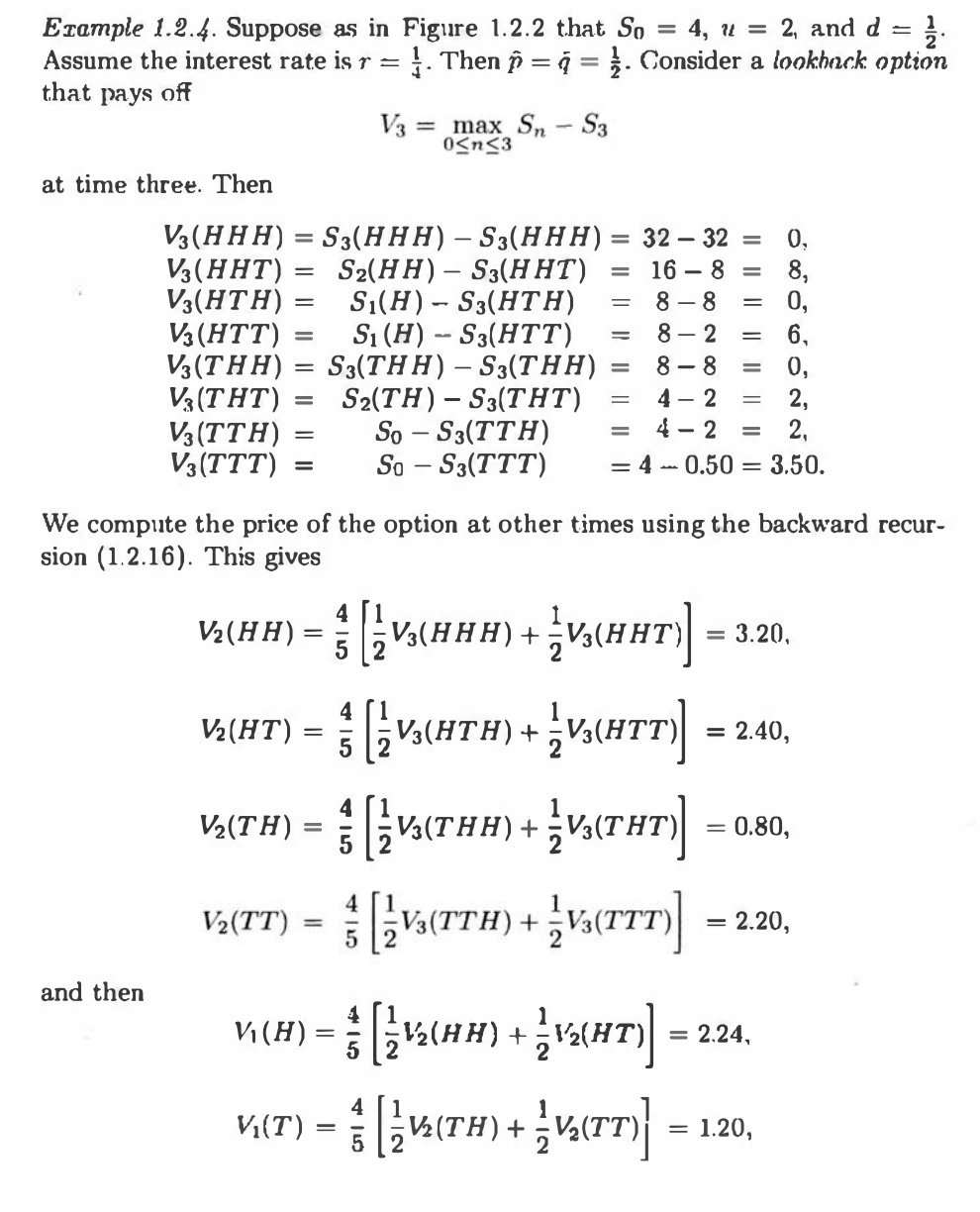

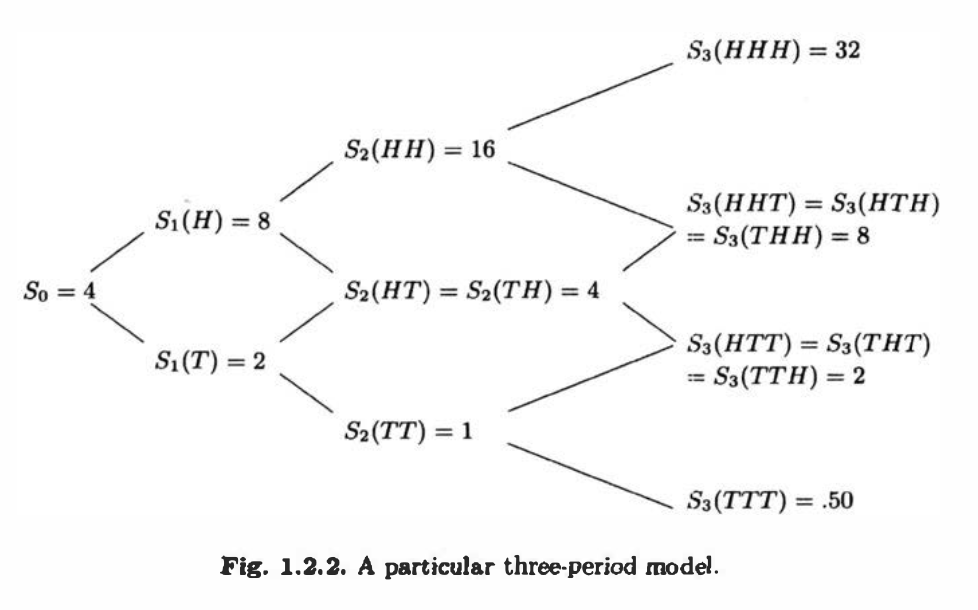

= = Exercise 1.5. In Example 1.2.4, we considered an agent who sold the look- back option for Vo 1.376 and bought 40 0.1733 shares of stock at time zero. At time one, if the stock goes up, she has a portfolio valued at V (H) = 2.24. Assume that she now takes a position of A(H) = V(HH)V2(HT) in the S(HH)-S2(HT) stock. Show that, at time two, if the stock goes up again, she will have a port- folio valued at V(HH) = 3.20, whereas if the stock goes down, her portfolio will be worth V(HT) = 2.40. Finally, under the assumption that the stock goes up in the first period and down in the second period, assume the agent V (HTH) V3(HTT) takes a position of 42 (HT) = 53(HTH) -S3(HTT) in the stock. Show that, at time three, if the stock goes up in the third period, she will have a portfolio valued at V3 (HTH) = 0, whereas if the stock goes down, her portfolio will be worth V3(HTT) = 6. In other words, she has hedged her short position in the option. = Example 1.2.4. Suppose as in Figure 1.2.2 that So = 4, u = 2, and d Assume the interest rate is r = 1. Then y = q = . Consider a lookback option that pays off at time three. Then V3 max Sn - S3 0n3 S3(HHH) - S3(HHH) = 32 - 32 = = 0. || || | 16-8 = 8-8 8, = 0, V3(HHH) V3(HHT) V3(HTH) S2(HH) S3(HHT) = = S(H) S3(HTH) V3 (HTT) = S(H) S3(HTT) = 8-2 = 6, V3(THH) = S3(THH) - S3(THH) = 8-8 = 0, V3 (THT) = S2(TH) S3(THT) 4-2 = 2, V3 (TTH) = So - S3(TTH) = 4-2 = 2 So-S3(TTT) - = 4 0.50 3.50. = V3 (TTT) = We compute the price of the option at other times using the backward recur- sion (1.2.16). This gives 4 V(HH): = (HHH) + (HHT)] = 3.20, 4 V(HT) = 5 V(HT) + (HTT)] = 2.40, V(TH) = [ (THH) + (THT)] = = 0.80, and then V(TT) = Va(TTH) + V(TTT)] [3 V (H) = [ { (HH) + 2(HT)] = = 2.20, = 2.24, V(T) = [V(TH) + V(TT) = 1.20, S3(HHH)=32 S(H)=8 So = 4 S(T) = 2 S2(HH) = 16 = S2(HT) S2(TH) = 4 S3(HHT) =S3(HTH) = S3(THH) = 8 S3(HTT) =S3(THT) ==== S3(TTH) = 2 S2 (TT) = 1 S3 (TTT): = .50 Fig. 1.2.2. A particular three-period model. = = Exercise 1.5. In Example 1.2.4, we considered an agent who sold the look- back option for Vo 1.376 and bought 40 0.1733 shares of stock at time zero. At time one, if the stock goes up, she has a portfolio valued at V (H) = 2.24. Assume that she now takes a position of A(H) = V(HH)V2(HT) in the S(HH)-S2(HT) stock. Show that, at time two, if the stock goes up again, she will have a port- folio valued at V(HH) = 3.20, whereas if the stock goes down, her portfolio will be worth V(HT) = 2.40. Finally, under the assumption that the stock goes up in the first period and down in the second period, assume the agent V (HTH) V3(HTT) takes a position of 42 (HT) = 53(HTH) -S3(HTT) in the stock. Show that, at time three, if the stock goes up in the third period, she will have a portfolio valued at V3 (HTH) = 0, whereas if the stock goes down, her portfolio will be worth V3(HTT) = 6. In other words, she has hedged her short position in the option. = Example 1.2.4. Suppose as in Figure 1.2.2 that So = 4, u = 2, and d Assume the interest rate is r = 1. Then y = q = . Consider a lookback option that pays off at time three. Then V3 max Sn - S3 0n3 S3(HHH) - S3(HHH) = 32 - 32 = = 0. || || | 16-8 = 8-8 8, = 0, V3(HHH) V3(HHT) V3(HTH) S2(HH) S3(HHT) = = S(H) S3(HTH) V3 (HTT) = S(H) S3(HTT) = 8-2 = 6, V3(THH) = S3(THH) - S3(THH) = 8-8 = 0, V3 (THT) = S2(TH) S3(THT) 4-2 = 2, V3 (TTH) = So - S3(TTH) = 4-2 = 2 So-S3(TTT) - = 4 0.50 3.50. = V3 (TTT) = We compute the price of the option at other times using the backward recur- sion (1.2.16). This gives 4 V(HH): = (HHH) + (HHT)] = 3.20, 4 V(HT) = 5 V(HT) + (HTT)] = 2.40, V(TH) = [ (THH) + (THT)] = = 0.80, and then V(TT) = Va(TTH) + V(TTT)] [3 V (H) = [ { (HH) + 2(HT)] = = 2.20, = 2.24, V(T) = [V(TH) + V(TT) = 1.20, S3(HHH)=32 S(H)=8 So = 4 S(T) = 2 S2(HH) = 16 = S2(HT) S2(TH) = 4 S3(HHT) =S3(HTH) = S3(THH) = 8 S3(HTT) =S3(THT) ==== S3(TTH) = 2 S2 (TT) = 1 S3 (TTT): = .50 Fig. 1.2.2. A particular three-period model.

Expert Answer:

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date:

Students also viewed these finance questions

-

7.1. Using risk-neutral valuation, derive a formula for a derivative that pays cash flows over the next two periods. Assume the risk-free rate is 4 percent per period. The underlying asset, which...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

In contrast to our analysis in Section 5.4.3, Carlton and Loury (1980) suggest that a Pigouvian tax alone will not lead to a long run social optimum for competitive polluting firms. Using their...

-

In 2010, Sunbeam Corporation acquired a silver mine in eastern Alaska. Because the mine is located deep in the Alaskan bush, Sunbeam was able to acquire the mine for the low price of $50,000. In...

-

Consider the tensile stress-strain diagrams in Figure 8 - 20 labeled 1 and 2 and answer the following questions. These curves are typical of metals. Consider each part as a separate question that has...

-

What are the advantages and disadvantages of permitting counter-claims for insurance claims to be offset in financial reports? Consider the views of management, shareholders and a non-governmental...

-

The costs of rework are always charged to the specific jobs in which the defects were originally discovered. Do you agree? Explain.

-

Although the Chen Company's milling machine is old, it is still in relatively good working order and would last for another 10 years. It is inefficient compared to modern standards, though, and so...

-

As customers shifted to shopping online, Best Buy's 1,100 giant stores, which enabled the company to obtain its position as the largest retailer of electronics, began to reduce its profitability and...

-

Create the following group policies in the Student OU: i. Enable strong password policy with 12 characters. ii. Accounts should be locked after 3 unsuccessful attempts for 30 minutes. iii. Remove...

-

Galaxy Sports Inc. manufactures and sells two styles of All Terrain Vehicles (ATVs), the Conquistador and Hurricane, from a single manufacturing facility. The manufacturing facility operates at 100%...

-

On January 1, a company issued 5%, 15-year bonds with a face amount of $80 million for $59,249,660 to yield 8%. Interest is paid semiannually. What was the interest expense at the effective interest...

-

Tyrone has already typed 100 words for an essay and can type 35 words per minute. Vanessa has already typed 120 words and can type 30 words per minute. In how many minutes will Tyrone and Vanessa...

-

The following information is provided for the first month of operations for Legal Services Inc.: Prepare a T-accounts to reflect the following business transaction: The Company provided legal...

-

A copper rod is 34.0 m on a winter day when the temperature is -5.0C (Linear expansion coefficient of copper 17 x 10-6/C). How long is the rod on a summer day when the temperature is 38.0C? Express...

-

It is June 6, Sheila Grainger first day in the newly created position of materials manager for Parts Warehouse. A recent graduate of a prominent business school, Grainger is eagerly awaiting her...

-

Three forces with magnitudes of 70pounds, 40 pounds, and 60 pounds act on an object at angles of 30, 45, and 135, respectively, with the positive x-axis. Find the direction and magnitude of the...

-

Wilcox was chief executive officer, chairman of the board of directors, and owner of 60 percent of the shares of Sterling Corporation. When the market price of Sterlings shares was $22 per share,...

-

Discuss the five situations limiting an offerors right to revoke her offer.

-

Several manufacturers introduced into the American market products known as all-terrain vehicles (ATVs). ATVs are motorized bikes that sit on three or four low-pressure balloon tires and are meant to...

-

Assume that you have shorted the put option in Problem 4. a. If the stock is trading at \($8\) in three months, what will you owe? b. If the stock is trading at \($23\) in three months, what will you...

-

Assume that you have shorted the call option in Problem 2. PROBLEM 2 You own a call option on Intuit stock with a strike price of \($40.\) The option will expire in exactly three months. a. If the...

-

Redo Problem 14, but assume that Kay must pay a corporate tax rate of 21%, and that investors pay no taxes. Problem 14. Chen Brothers, Inc., sold 4 million shares in its IPO, at a price of \($18.50\)...

Study smarter with the SolutionInn App