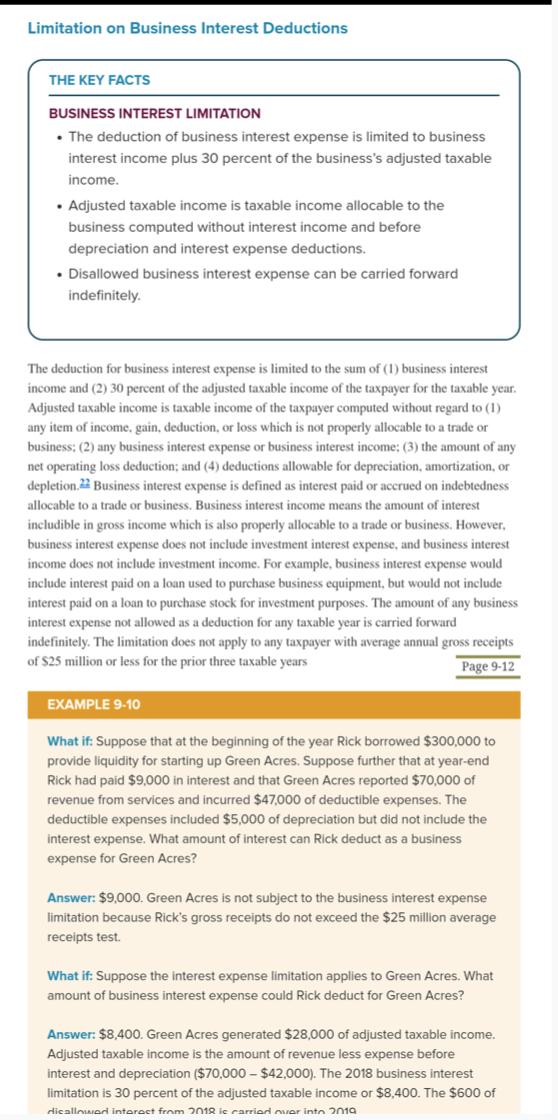

For a business with no interest income, what is the limitation on business interest deductions? What businesses

Fantastic news! We've Found the answer you've been seeking!

Question:

- For a business with no interest income, what is the limitation on business interest deductions?

- What businesses are not subject to this limitation?

- For a business that is subject to the limitation, what benefit can the business get from interest payments that exceed the limit? Give an example. For this question please refer to the screenshot posted.

Expert Answer:

For a business with no interest income what is the limitation on business interest deductions The bu... View the full answer

Related Book For

Services Marketing Concepts, Strategies, & Cases

ISBN: 978-1439039397

4th edition

Authors: Douglas Hoffman, john Bateson

Posted Date: