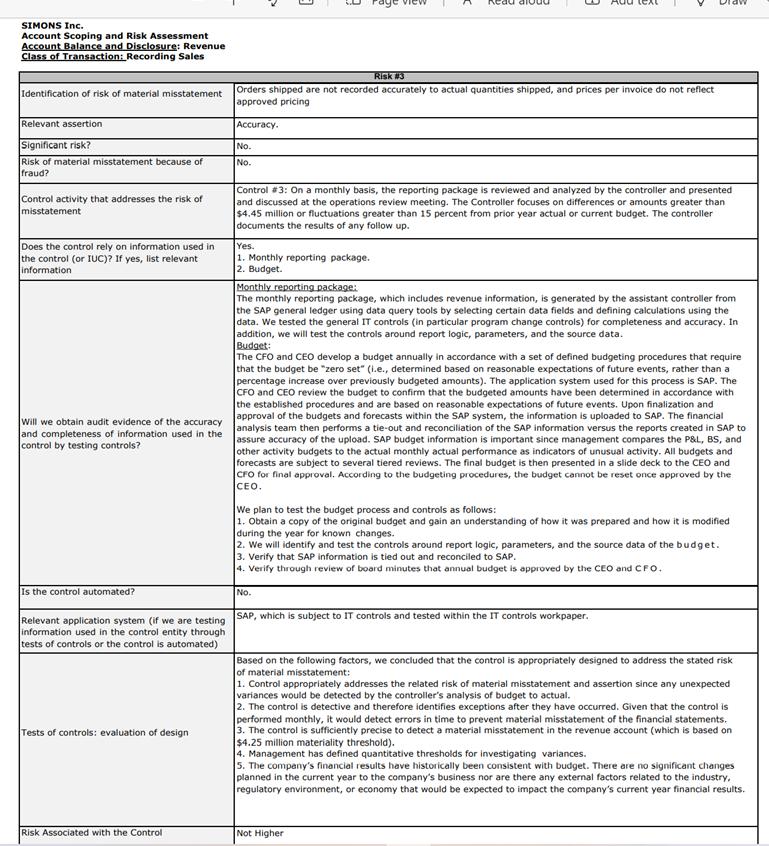

for risk #3: a. Was the engagement teams assessment of the evaluation of the design of each

Fantastic news! We've Found the answer you've been seeking!

Question:

for risk #3:

a. Was the engagement team’s assessment of the evaluation of the design of each control appropriate (i.e., does the control identified by the team address the specific risk of material misstatement and associated assertion)

b. Was the engagement team’s assessment of the risk associated with each control appropriate?

c. Was the team’s interim planned procedures to test the operating effectiveness of each control appropriate considering the risk associated with the control?

d. Was the team’s roll-forward planned procedures to test the operating effectiveness of each control appropriate considering the risk associated with the control

Expert Answer:

Definition of Revenue on sale of goods as per US GAAP Revenue from the sale of goods or products sho... View the full answer

Related Book For

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

Posted Date: