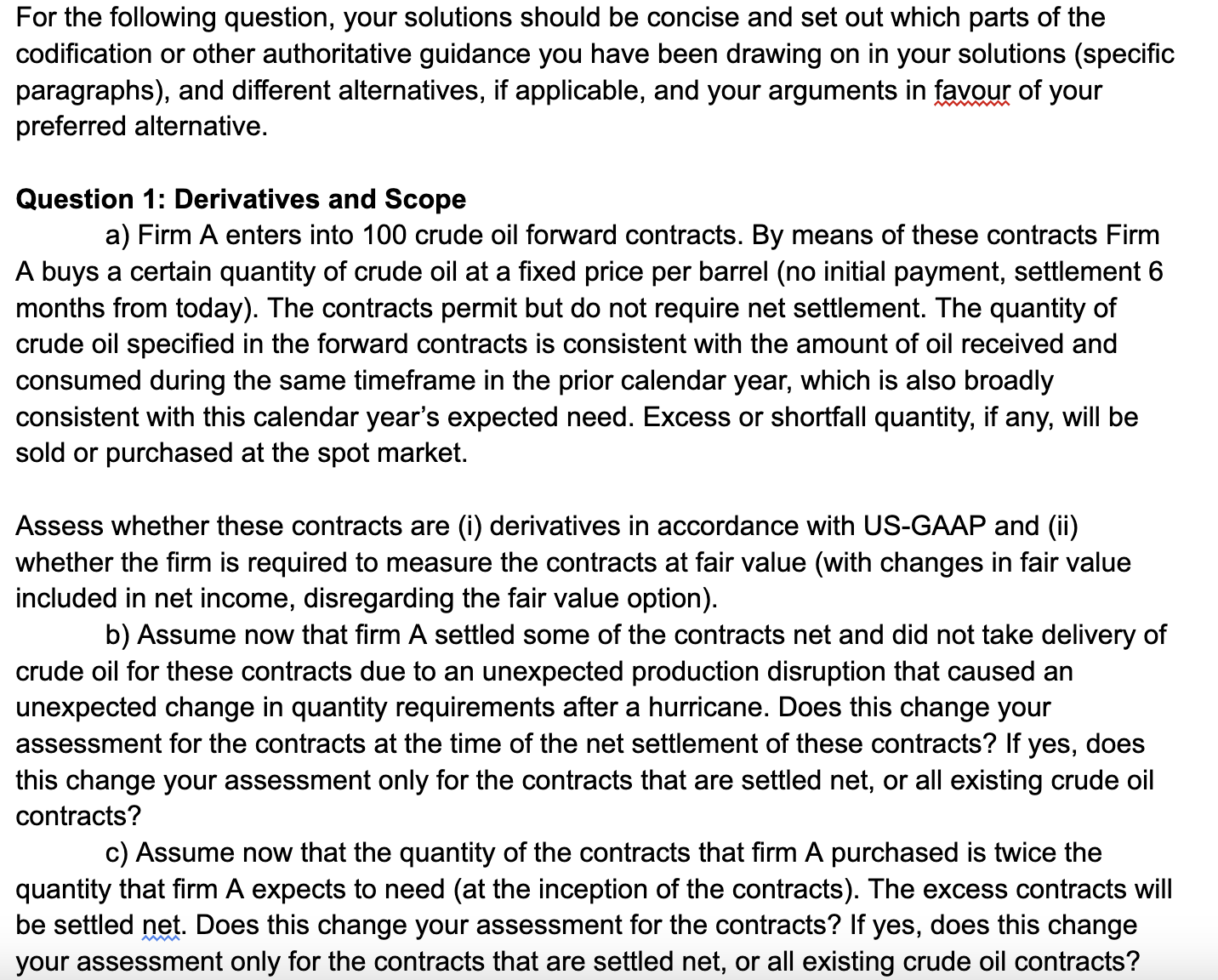

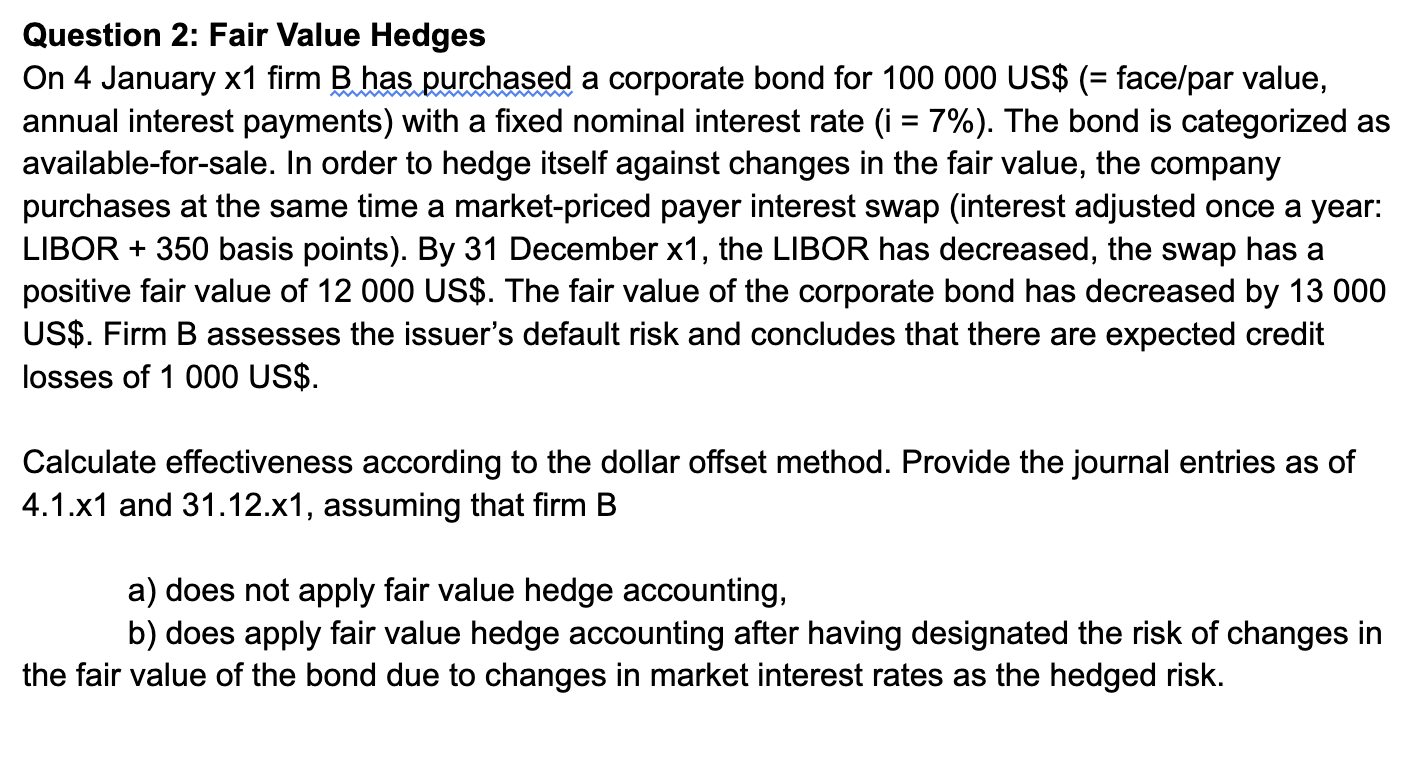

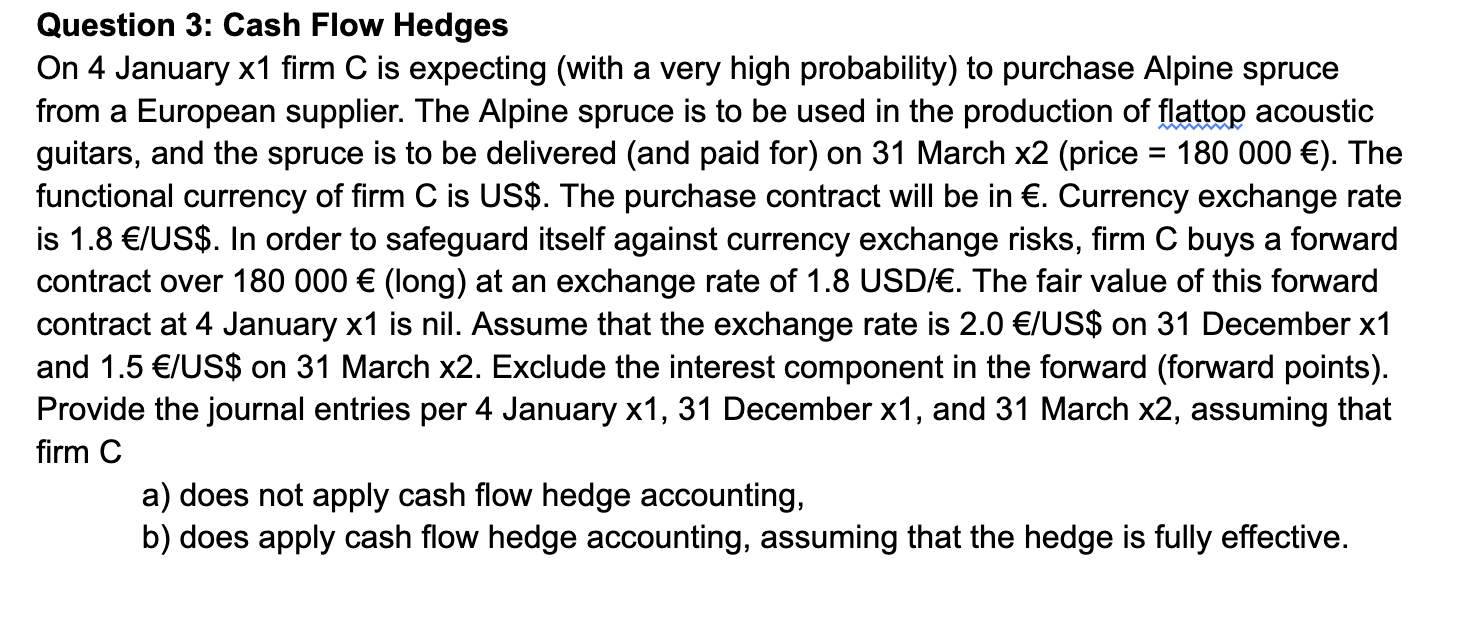

For the following question, your solutions should be concise and set out which parts of the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a According to USGAAP ASC 8151015126 derivatives are defined as financial instruments or other contr... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0132162302

1st edition

Authors: Elizabeth A. Gordon, Jana S. Raedy, Alexander J. Sannella

Posted Date: