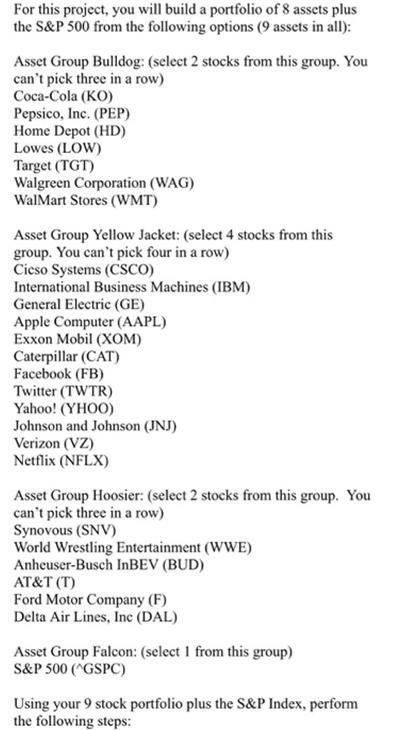

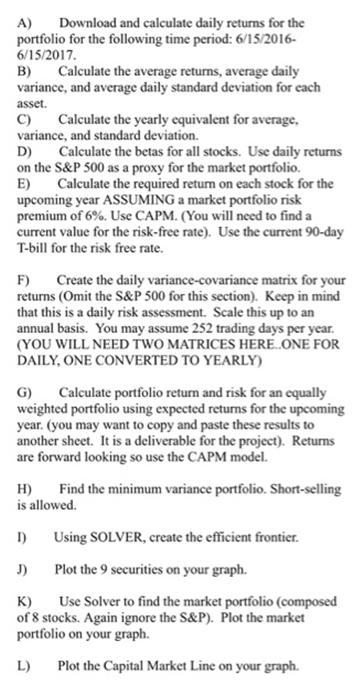

For this project, you will build a portfolio of 8 assets plus the S&P 500 from...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

A To download and calculate daily returns for the portfolio for the given time period you would need access to financial data or a financial software The daily returns can be calculated using the form... View the full answer

Related Book For

Statistical Reasoning for Everyday Life

ISBN: 978-0321817624

4th edition

Authors: Jeff Bennett, Bill Briggs, Mario F. Triola

Posted Date: