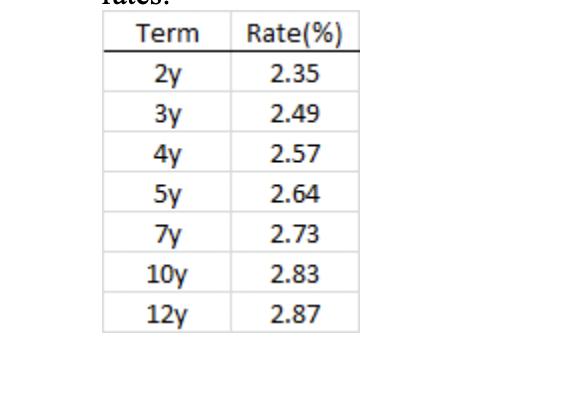

Forward starting swaps Use the spot swap rates listed below to answer the following questions on forward

Fantastic news! We've Found the answer you've been seeking!

Question:

1. Where would you price a 2-year swap starting 2-years from now given the spot rates shown?

2. The current spot spread between 10-year and 2-year swaps (aka 2s/10s swap curve) is 150 basis points. Where does the market expect the spread between 10- year and 2-year swaps to be 2-years from now?

Expert Answer:

To answer these questions you can use the concept of forward starting swaps and the given spot swap ... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: