Additional information i. At 1 July 2012, all the identifiable assets and liabilities of Moon Ltd were

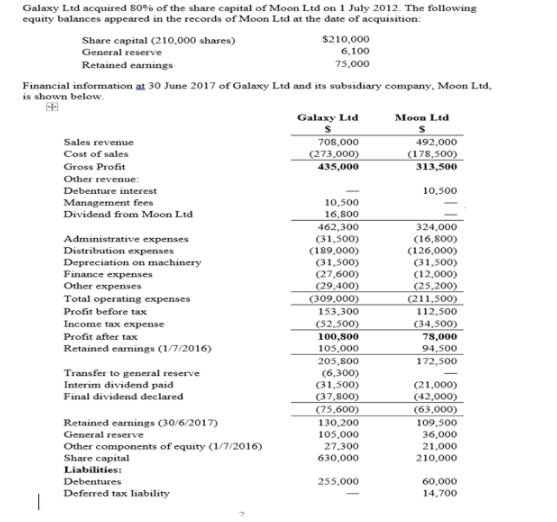

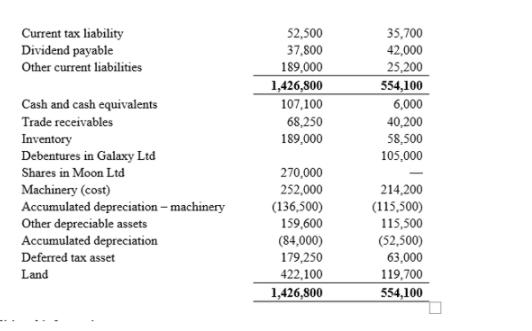

Question:

Additional information i. At 1 July 2012, all the identifiable assets and liabilities of Moon Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land $62,000 $80,000 Machinery (cost 135,000) 105,000 120,000 Receivable 42,000 36,000 The machinery has an expected life of 10 years, with benefits being received evenly over that period. Differences between carrying amounts and fair values are adjusted on consolidation. The land on hand at 1 July 2012 was sold on 1 March 2014 for $84,000. Any valuation reserve in relation to the land is transferred on consolidation to retained earnings. By 30 June 2013, receivables had all been collected.

ii. Galaxy Ltd uses the full goodwill method. The fair value of the non-controlling interest at 1 July 2012 was $66,000.

iii. Opening inventory of Moon Ltd includes unrealized profit of $5,000 on inventory sold by Galaxy Ltd. It was all sold by Moon Ltd during the year. iv. During the year, intragroup sales by Moon Ltd to Galaxy Ltd were $80,000. The mark-up on cost of all sales was 25%. At 30 June 2017, Galaxy Ltd’s inventory included $35,000 of items acquired from Moon Ltd.

v. On 1 January 2017, Moon Ltd sold an item of inventory to Galaxy Ltd for $18,000 at a profit before tax of $3000. Galaxy Ltd had treated this item as an addition to its machinery and depreciated at 10% p.a. straight-line.

vi. On 1 April 2017, Galaxy Ltd sold $15,000 worth of inventory to Moon Ltd. The cost of this inventory was $9000. By 30 June 2017, Moon Ltd had sold 60% of the inventory to outside entities.

vii. Some of the items manufactured by Moon Ltd are used as machinery by Galaxy Ltd. One of the machinery items held by Galaxy Ltd at 30 June 2017 was purchased from Moon Ltd on 1 January 2016. It had cost Moon Ltd $17,500 to manufacture this item and was sold to Galaxy Ltd for $25,000. Galaxy Ltd depreciates such items at 10% p.a. on cost.

viii. Management fees derived by Galaxy Ltd were all from Moon Ltd and represented charges made for administration.

ix. The tax rate is 30%.

Required: a) Prepare the acquisition analysis at 1 July 2012.

b) Prepare the consolidation journal entries, including: - The business combination valuation entries; - The pre-acquisition entries; - The intra-group entries (considering the effects on non-controlling interests);

c) Calculate NCI share of equity at following dates and prepare the journal entries (not considering the effects of intra-group transactions): - 1 July 2012; - 1 July 2012 – 30 June 2016; (4.5 marks) - 1 July 2016 – 30 June 2017.

d) Show the balance of following accounts presented in the consolidated financial statement - The balance of Non-Controlling Interests in the consolidated financial statement; (5.5 marks) - The balance of Business Combination Revaluation Reserve (BCVR) in the consolidated financial statement; (3 marks) - The balance of Deferred Tax Assets in the consolidated financial statement;

Expert Answer:

a Acquisition Analysis at 1 July 2012 Fair value adjustments Land Fair value adjustment Fair value Carrying amount Fair value adjustment 80000 62000 Fair value adjustment 18000 Machinery Fair value ad... View the full answer