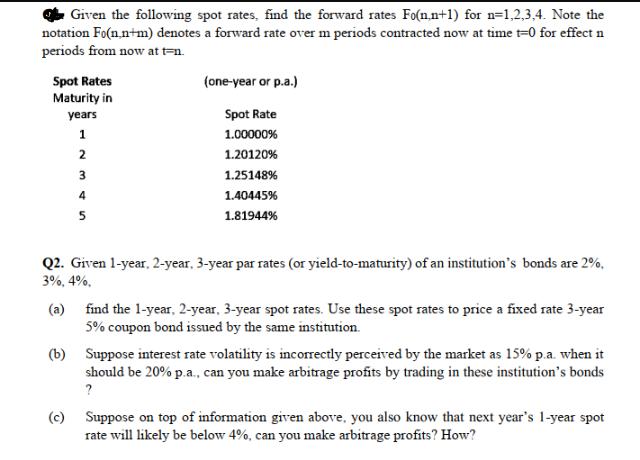

Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m)...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

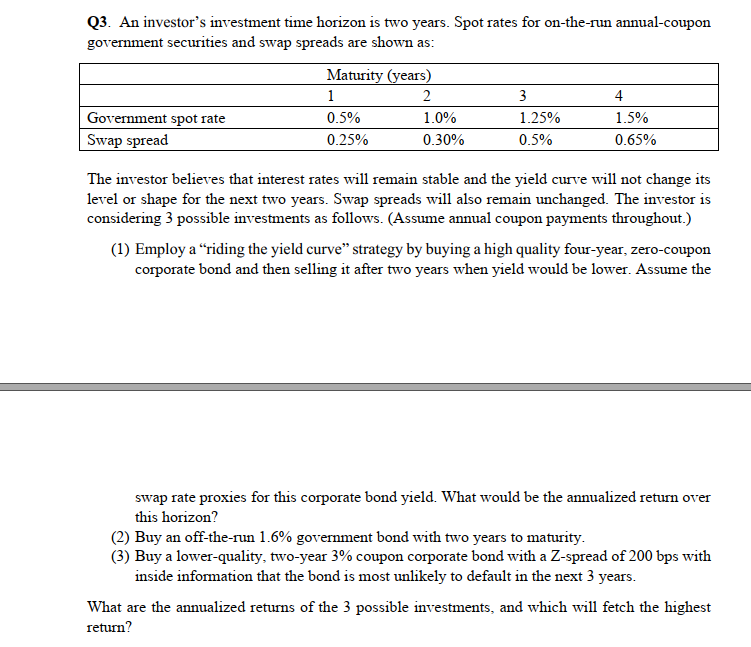

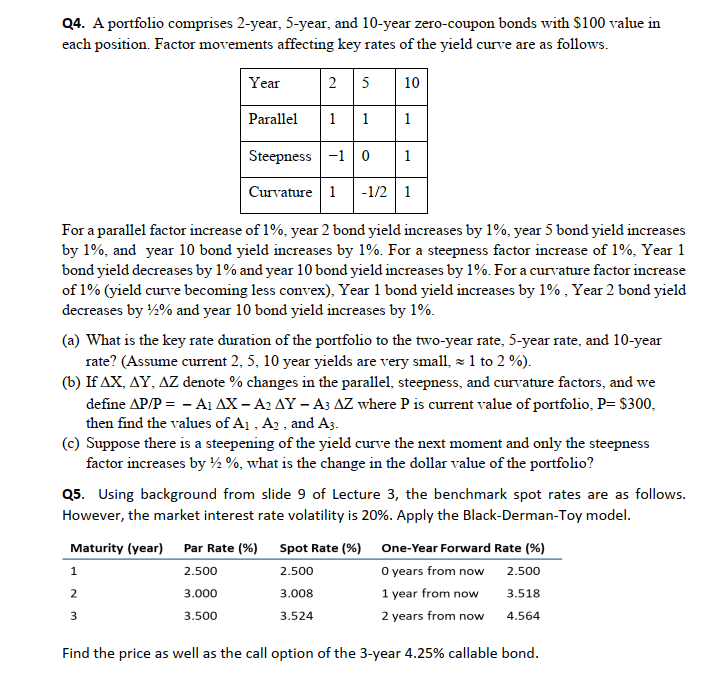

Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m) denotes a forward rate over m periods contracted now at time t=0 for effect n periods from now at t=n. Spot Rates Maturity in years 1 2 3 4 5 (one-year or p.a.) Spot Rate 1.00000% 1.20120% 1.25148% 1.40445% 1.81944% Q2. Given 1-year, 2-year, 3-year par rates (or yield-to-maturity) of an institution's bonds are 2%. 3%, 4%, (a) (c) find the 1-year, 2-year, 3-year spot rates. Use these spot rates to price a fixed rate 3-year 5% coupon bond issued by the same institution. (b) Suppose interest rate volatility is incorrectly perceived by the market as 15% p.a. when it should be 20% p.a., can you make arbitrage profits by trading in these institution's bonds ? Suppose on top of information given above, you also know that next year's 1-year spot rate will likely be below 4%, can you make arbitrage profits? How? Q3. An investor's investment time horizon is two years. Spot rates for on-the-run annual-coupon government securities and swap spreads are shown as: Government spot rate Swap spread Maturity (years) 2 1.0% 0.30% 1 0.5% 0.25% 3 1.25% 0.5% 4 1.5% 0.65% The investor believes that interest rates will remain stable and the yield curve will not change its level or shape for the next two years. Swap spreads will also remain unchanged. The investor is considering 3 possible investments as follows. (Assume annual coupon payments throughout.) (1) Employ a "riding the yield curve" strategy by buying a high quality four-year, zero-coupon corporate bond and then selling it after two years when yield would be lower. Assume the swap rate proxies for this corporate bond yield. What would be the annualized return over this horizon? (2) Buy an off-the-run 1.6% government bond with two years to maturity. (3) Buy a lower-quality, two-year 3% coupon corporate bond with a Z-spread of 200 bps with inside information that the bond is most unlikely to default in the next 3 years. What are the annualized returns of the 3 possible investments, and which will fetch the highest return? Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $100 value in each position. Factor movements affecting key rates of the yield curve are as follows. 25 Year 1 1 Steepness -1 0 Curvature Parallel For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1%, Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. 1 10 (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - A1 AX-A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of A1, A2, and A3. 2 1 1 1-1/2 1 (c) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by %, what is the change in the dollar value of the portfolio? 3 Q5. Using background from slide 9 of Lecture 3, the benchmark spot rates are as follows. However, the market interest rate volatility is 20%. Apply the Black-Derman-Toy model. Maturity (year) Par Rate (%) Spot Rate (%) 2.500 2.500 3.000 3.008 3.500 3.524 One-Year Forward Rate (%) 0 years from now 2.500 1 year from now 3.518 2 years from now 4.564 Find the price as well as the call option of the 3-year 4.25% callable bond. Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m) denotes a forward rate over m periods contracted now at time t=0 for effect n periods from now at t=n. Spot Rates Maturity in years 1 2 3 4 5 (one-year or p.a.) Spot Rate 1.00000% 1.20120% 1.25148% 1.40445% 1.81944% Q2. Given 1-year, 2-year, 3-year par rates (or yield-to-maturity) of an institution's bonds are 2%. 3%, 4%, (a) (c) find the 1-year, 2-year, 3-year spot rates. Use these spot rates to price a fixed rate 3-year 5% coupon bond issued by the same institution. (b) Suppose interest rate volatility is incorrectly perceived by the market as 15% p.a. when it should be 20% p.a., can you make arbitrage profits by trading in these institution's bonds ? Suppose on top of information given above, you also know that next year's 1-year spot rate will likely be below 4%, can you make arbitrage profits? How? Q3. An investor's investment time horizon is two years. Spot rates for on-the-run annual-coupon government securities and swap spreads are shown as: Government spot rate Swap spread Maturity (years) 2 1.0% 0.30% 1 0.5% 0.25% 3 1.25% 0.5% 4 1.5% 0.65% The investor believes that interest rates will remain stable and the yield curve will not change its level or shape for the next two years. Swap spreads will also remain unchanged. The investor is considering 3 possible investments as follows. (Assume annual coupon payments throughout.) (1) Employ a "riding the yield curve" strategy by buying a high quality four-year, zero-coupon corporate bond and then selling it after two years when yield would be lower. Assume the swap rate proxies for this corporate bond yield. What would be the annualized return over this horizon? (2) Buy an off-the-run 1.6% government bond with two years to maturity. (3) Buy a lower-quality, two-year 3% coupon corporate bond with a Z-spread of 200 bps with inside information that the bond is most unlikely to default in the next 3 years. What are the annualized returns of the 3 possible investments, and which will fetch the highest return? Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $100 value in each position. Factor movements affecting key rates of the yield curve are as follows. 25 Year 1 1 Steepness -1 0 Curvature Parallel For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1%, Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. 1 10 (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - A1 AX-A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of A1, A2, and A3. 2 1 1 1-1/2 1 (c) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by %, what is the change in the dollar value of the portfolio? 3 Q5. Using background from slide 9 of Lecture 3, the benchmark spot rates are as follows. However, the market interest rate volatility is 20%. Apply the Black-Derman-Toy model. Maturity (year) Par Rate (%) Spot Rate (%) 2.500 2.500 3.000 3.008 3.500 3.524 One-Year Forward Rate (%) 0 years from now 2.500 1 year from now 3.518 2 years from now 4.564 Find the price as well as the call option of the 3-year 4.25% callable bond.

Expert Answer:

Answer rating: 100% (QA)

Q1 Forward rates F012 120120 F023 125148 F034 140445 Q2 a Spot rates 1Y 2 2Y 1 305 1 15 3Y 1 403 1 1... View the full answer

Related Book For

Fundamentals of Investments

ISBN: 978-0132926171

3rd edition

Authors: Gordon J. Alexander, William F. Sharpe, Jeffery V. Bailey

Posted Date:

Students also viewed these finance questions

-

KYC's stock price can go up by 15 percent every year, or down by 10 percent. Both outcomes are equally likely. The risk free rate is 5 percent, and the current stock price of KYC is 100. (a) Price a...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Consider a set of documents. Assume that all documents have been normalized to have unit length of 1. What is the "shape" of a cluster that consists of all documents whose cosine similarity to a...

-

Pensacola Marine, Inc., had income before income tax of $110,000 and taxable income of $90,000 for 20X8, the company's first year of operations. The income tax rate is 40%. 1. Make the entry to...

-

A company purchases equipment at the beginning of the year at a cost of $45,900. The equipment's useful life is estimated at 10 years, or 389,000 units of product, with a $7,000 salvage value. During...

-

When to use a motion for judgment on the pleadings?

-

Michelle Gutierrez, manager of the Components Division of FX Corporation, is considering a new investment for her division. The division has an investment base of $4,000,000 and operating income of...

-

Our Financial Institutions team understands the ongoing and emerging challenges of the industry because we're immersed in it every day. We know a Financial Institutions competitiveness depends on the...

-

a) Describe at least two ways in which the CMP process improves photolithography. b) In a particular positive resist process, it is sometimes noticed that there is difficulty developing away the last...

-

Compare and Contrast Leadership Styles and Evaluate the Best Coach Fit After reviewing the links below on coaching leadership styles present the coaches and their style might work best for you if you...

-

On October 15, 2023, the board of directors of Martinez Materials Corporation approved a stock option plan for key executives. On January 1, 2024, 38 million stock options were granted, exercisable...

-

An ARM is made for $240,000 for 30 years with the following terms: Initial interest rate = 7 percent Index = 1year Treasuries Payments reset each year Margin = 2 percent Interest rate cap = None...

-

Vincent owns a printer shop, Heartbreaker Ltd . For the month of November 2 0 2 3 , the transactions were as follows: November 2 0 2 3 1 Commenced business with RM 3 , 0 0 0 in the bank. 2 Purchased...

-

If R = B 2, R =B/5 2, R3 = D 2, and I=0.50 A, Calculate resultant resistance? b. At what rate is heat being generated in these resistors? c. Calculate the net voltage on the circuit? R R R

-

Calculate the required length L of this fillet weld. F(N) Weld size b (mm) Allowable stress (N/mm) 0,1 45000 8 165 4th digit, Student ID 4,5 50500 5 145 2,3 60000 6 185 6,7 95000 12 125 8,9 105000 10...

-

Why did management adopt the new plan even though it provides a smaller expected number of exposures than the original plan recommended by the original linear programming model?

-

Given the following information, calculate the three-month price of a call that is consistent with the Black-Scholes model: Ps = $47, E = $45, R = .05. = .40

-

What factors might an individual investor take into account in determining his or her investment policy?

-

Nellie Fox acquired at par a bond for $1,000 that offered a 9% coupon rate. At the time of purchase, the bond had four years to maturity. Assuming annual interest payments, calculate Nellie's actual...

-

What other services do accountants provide in addition to auditing?

-

What are the time limits for laying and delivery of accounts?

-

Define an audit.

Study smarter with the SolutionInn App