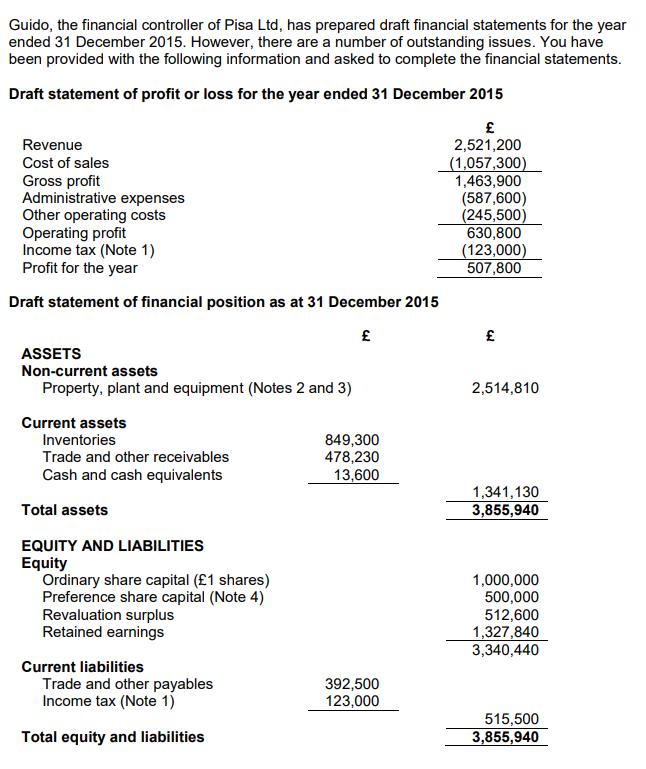

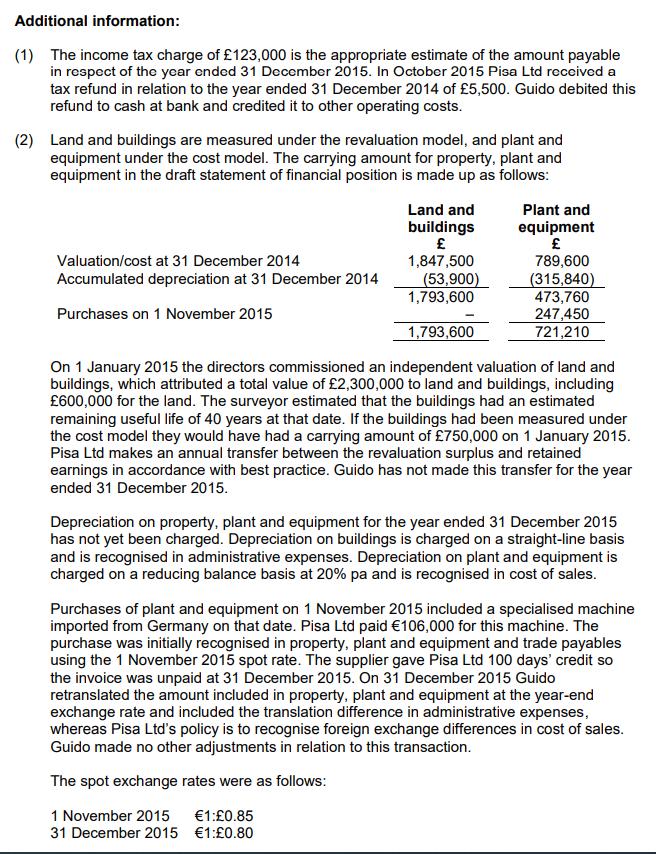

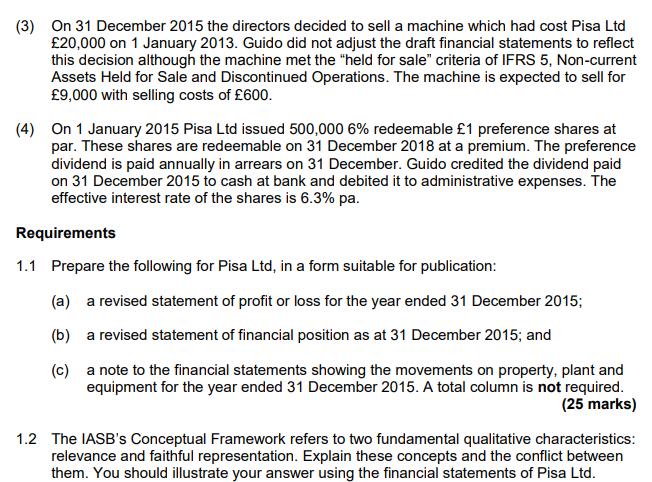

Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended 31 December 2015. However, there are a number of outstanding issues. You have been provided with the following information and asked to complete the financial statements. Draft statement of profit or loss for the year ended 31 December 2015 £ 2,521,200 (1,057,300) 1,463,900 Revenue Cost of sales Gross profit Administrative expenses Other operating costs Operating profit Income tax (Note 1) Profit for the year Draft statement of financial position as at 31 December 2015 ASSETS Non-current assets Property, plant and equipment (Notes 2 and 3) Current assets Inventories Trade and other receivables Cash and cash equivalents Total assets EQUITY AND LIABILITIES Equity Ordinary share capital (£1 shares) Preference share capital (Note 4) Revaluation surplus Retained earnings Current liabilities Trade and other payables Income tax (Note 1) Total equity and liabilities W 849,300 478,230 13,600 392,500 123,000 (587,600) (245,500) 630,800 (123,000) 507,800 £ 2,514,810 1,341,130 3,855,940 1,000,000 500,000 512,600 1,327,840 3,340,440 515,500 3,855,940 Additional information: (1) The income tax charge of £123,000 is the appropriate estimate of the amount payable in respect of the year ended 31 December 2015. In October 2015 Pisa Ltd received a tax refund in relation to the year ended 31 December 2014 of £5,500. Guido debited this refund to cash at bank and credited it to other operating costs. (2) Land and buildings are measured under the revaluation model, and plant and equipment under the cost model. The carrying amount for property, plant and equipment in the draft statement of financial position is made up as follows: Valuation/cost at 31 December 2014 Accumulated depreciation at 31 December 2014 Purchases on 1 November 2015 Land and buildings £ 1,847,500 (53,900) 1,793,600 1,793,600 On 1 January 2015 the directors commissioned an independent valuation of land and buildings, which attributed a total value of £2,300,000 to land and buildings, including £600,000 for the land. The surveyor estimated that the buildings had an estimated remaining useful life of 40 years at that date. If the buildings had been measured under the cost model they would have had a carrying amount of £750,000 on 1 January 2015. Pisa Ltd makes an annual transfer between the revaluation surplus and retained earnings in accordance with best practice. Guido has not made this transfer for the year ended 31 December 2015. Plant and equipment £ 789,600 (315,840) 473,760 247,450 721,210 Depreciation on property, plant and equipment for the year ended 31 December 2015 has not yet been charged. Depreciation on buildings is charged on a straight-line basis and is recognised in administrative expenses. Depreciation on plant and equipment is charged on a reducing balance basis at 20% pa and is recognised in cost of sales. 1 November 2015 31 December 2015 Purchases of plant and equipment on 1 November 2015 included a specialised machine imported from Germany on that date. Pisa Ltd paid €106,000 for this machine. The purchase was initially recognised in property, plant and equipment and trade payables using the 1 November 2015 spot rate. The supplier gave Pisa Ltd 100 days' credit so the invoice was unpaid at 31 December 2015. On 31 December 2015 Guido retranslated the amount included in property, plant and equipment at the year-end exchange rate and included the translation difference in administrative expenses, whereas Pisa Ltd's policy is to recognise foreign exchange differences in cost of sales. Guido made no other adjustments in relation to this transaction. The spot exchange rates were as follows: €1:£0.85 €1:£0.80 (3) On 31 December 2015 the directors decided to sell a machine which had cost Pisa Ltd £20,000 on 1 January 2013. Guido did not adjust the draft financial statements to reflect this decision although the machine met the "held for sale" criteria of IFRS 5, Non-current Assets Held for Sale and Discontinued Operations. The machine is expected to sell for £9,000 with selling costs of £600. (4) On 1 January 2015 Pisa Ltd issued 500,000 6% redeemable £1 preference shares at par. These shares are redeemable on 31 December 2018 at a premium. The preference dividend is paid annually in arrears on 31 December. Guido credited the dividend paid on 31 December 2015 to cash at bank and debited it to administrative expenses. The effective interest rate of the shares is 6.3% pa. Requirements 1.1 Prepare the following for Pisa Ltd, in a form suitable for publication: (a) a revised statement of profit or loss for the year ended 31 December 2015; (b) a revised statement of financial position as at 31 December 2015; and (c) a note to the financial statements showing the movements on property, plant and equipment for the year ended 31 December 2015. A total column is not required. (25 marks) 1.2 The IASB's Conceptual Framework refers to two fundamental qualitative characteristics: relevance and faithful representation. Explain these concepts and the conflict between them. You should illustrate your answer using the financial statements of Pisa Ltd. Guido, the financial controller of Pisa Ltd, has prepared draft financial statements for the year ended 31 December 2015. However, there are a number of outstanding issues. You have been provided with the following information and asked to complete the financial statements. Draft statement of profit or loss for the year ended 31 December 2015 £ 2,521,200 (1,057,300) 1,463,900 Revenue Cost of sales Gross profit Administrative expenses Other operating costs Operating profit Income tax (Note 1) Profit for the year Draft statement of financial position as at 31 December 2015 ASSETS Non-current assets Property, plant and equipment (Notes 2 and 3) Current assets Inventories Trade and other receivables Cash and cash equivalents Total assets EQUITY AND LIABILITIES Equity Ordinary share capital (£1 shares) Preference share capital (Note 4) Revaluation surplus Retained earnings Current liabilities Trade and other payables Income tax (Note 1) Total equity and liabilities W 849,300 478,230 13,600 392,500 123,000 (587,600) (245,500) 630,800 (123,000) 507,800 £ 2,514,810 1,341,130 3,855,940 1,000,000 500,000 512,600 1,327,840 3,340,440 515,500 3,855,940 Additional information: (1) The income tax charge of £123,000 is the appropriate estimate of the amount payable in respect of the year ended 31 December 2015. In October 2015 Pisa Ltd received a tax refund in relation to the year ended 31 December 2014 of £5,500. Guido debited this refund to cash at bank and credited it to other operating costs. (2) Land and buildings are measured under the revaluation model, and plant and equipment under the cost model. The carrying amount for property, plant and equipment in the draft statement of financial position is made up as follows: Valuation/cost at 31 December 2014 Accumulated depreciation at 31 December 2014 Purchases on 1 November 2015 Land and buildings £ 1,847,500 (53,900) 1,793,600 1,793,600 On 1 January 2015 the directors commissioned an independent valuation of land and buildings, which attributed a total value of £2,300,000 to land and buildings, including £600,000 for the land. The surveyor estimated that the buildings had an estimated remaining useful life of 40 years at that date. If the buildings had been measured under the cost model they would have had a carrying amount of £750,000 on 1 January 2015. Pisa Ltd makes an annual transfer between the revaluation surplus and retained earnings in accordance with best practice. Guido has not made this transfer for the year ended 31 December 2015. Plant and equipment £ 789,600 (315,840) 473,760 247,450 721,210 Depreciation on property, plant and equipment for the year ended 31 December 2015 has not yet been charged. Depreciation on buildings is charged on a straight-line basis and is recognised in administrative expenses. Depreciation on plant and equipment is charged on a reducing balance basis at 20% pa and is recognised in cost of sales. 1 November 2015 31 December 2015 Purchases of plant and equipment on 1 November 2015 included a specialised machine imported from Germany on that date. Pisa Ltd paid €106,000 for this machine. The purchase was initially recognised in property, plant and equipment and trade payables using the 1 November 2015 spot rate. The supplier gave Pisa Ltd 100 days' credit so the invoice was unpaid at 31 December 2015. On 31 December 2015 Guido retranslated the amount included in property, plant and equipment at the year-end exchange rate and included the translation difference in administrative expenses, whereas Pisa Ltd's policy is to recognise foreign exchange differences in cost of sales. Guido made no other adjustments in relation to this transaction. The spot exchange rates were as follows: €1:£0.85 €1:£0.80 (3) On 31 December 2015 the directors decided to sell a machine which had cost Pisa Ltd £20,000 on 1 January 2013. Guido did not adjust the draft financial statements to reflect this decision although the machine met the "held for sale" criteria of IFRS 5, Non-current Assets Held for Sale and Discontinued Operations. The machine is expected to sell for £9,000 with selling costs of £600. (4) On 1 January 2015 Pisa Ltd issued 500,000 6% redeemable £1 preference shares at par. These shares are redeemable on 31 December 2018 at a premium. The preference dividend is paid annually in arrears on 31 December. Guido credited the dividend paid on 31 December 2015 to cash at bank and debited it to administrative expenses. The effective interest rate of the shares is 6.3% pa. Requirements 1.1 Prepare the following for Pisa Ltd, in a form suitable for publication: (a) a revised statement of profit or loss for the year ended 31 December 2015; (b) a revised statement of financial position as at 31 December 2015; and (c) a note to the financial statements showing the movements on property, plant and equipment for the year ended 31 December 2015. A total column is not required. (25 marks) 1.2 The IASB's Conceptual Framework refers to two fundamental qualitative characteristics: relevance and faithful representation. Explain these concepts and the conflict between them. You should illustrate your answer using the financial statements of Pisa Ltd.

Expert Answer:

Answer rating: 100% (QA)

11a Statement of profit or loss for the year ended 31 December 2015 2521200 Revenue Cost of sales Gr... View the full answer

Posted Date:

Students also viewed these accounting questions

-

You have been provided with the following information about two companies: Required: a. Calculate the current ratio for each company and the amount of working capital each company has. b. Which...

-

You have been provided with the following information about Everell Inc. (Everell). Required: a. Calculate the accounts receivable, inventory, and accounts payable turnover ratios for 2016 through...

-

You have been provided with the following information regarding R-Steel Inc.'s inventory for March, April, and May. Instructions (a) Calculate the cost and net realizable value of R-Steel's inventory...

-

The table represents values of differentiable functions f and g and their first derivatives. Use the table of values to answer the questions that follow. Work all of the parts below the line. X f g...

-

As a manager of a department store, you must deal with a variety of business transactions. Place the letter of each of the following transactions next to the effect it has on the accounting equation....

-

Discuss the methods by which the SEC can influence the development of generally accepted accounting principles in the United States.

-

Payments to directors would be shown in the financial statements as: a. An expense in the income statement b. A dividend c. A current asset d. Part of share capital

-

Twentieth Century Fox (Fox) owned and distributed the successful motion picture The Commitments. The film tells the story of a group of young Irish men and women who form a soul music band. In the...

-

What is the present worth of an investment that starts at $6,000 in year 1 and increases by 6% per year for 10 years at 6% interest. (10 years total cash flows) O $38,768 $42,056 O $33,001 $56,603

-

If the a company has a market value of debt of 5 million pound and a market value of equity of 15 million pounds what's is the weight of debt for wacc calculation purpose?

-

how has financial services changed in the last 30 years and analyze whether or not you feel those changes increased or decreased the risks banks face. Please include a discussion of Traditional model...

-

A consol bond pays forever two semiannual coupons at an annual coupon rate of 3.60% In other words, the initial principal is never reduced nor repaid.The yield-to-maturity is 6.80% and a coupon was...

-

How can we leverage the interplay between the gut microbiome, the immune system, and genetics to develop personalized therapeutic approaches for autoimmune diseases like inflammatory bowel disease...

-

A very long cupper fin (k=200 W/m.K) with a cross sectional area of Ac = 5 mm2 and perimeter of P = 8 mm, is attached to a surface whose temperature is Tb. The fin is subjected to convection heat...

-

please answer correct in detail Why is "Activity-Based Costing" Useful Information for Human Resources Management?please explain.

-

If gravity is an emergent property arising from the curvature of spacetime caused by mass and energy, how can we reconcile this with the fact that gravity interacts so weakly compared to the other...

-

15 points Speed Toast, a Belleville, Ontario, restaurant, began with investments by the partners as follows: Lea, $233,700, Eve, $177700, and Sophie, $192,300. The first year of operations did not go...

-

Subprime loans have higher loss rates than many other types of loans. Explain why lenders offer subprime loans. Describe the characteristics of the typical borrower in a subprime consumer loan.

-

Assume that interest rate parity exists and it will continue to exist in the future. Assume that interest rates of the United States and the United Kingdom vary substantially in many periods. You...

-

Assume that interest rate parity exists and it will continue to exist in the future. Kentucky Co. wants to forecast the value of the Japanese yen in 1 month. The Japanese interest rate is lower than...

-

Assume that interest rate parity exists. Today the 1-year U.S. interest rate is equal to 8 percent, while Mexicos 1-year interest rate is equal to 10 percent. Today the 2- year annualized U.S....

Study smarter with the SolutionInn App