Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

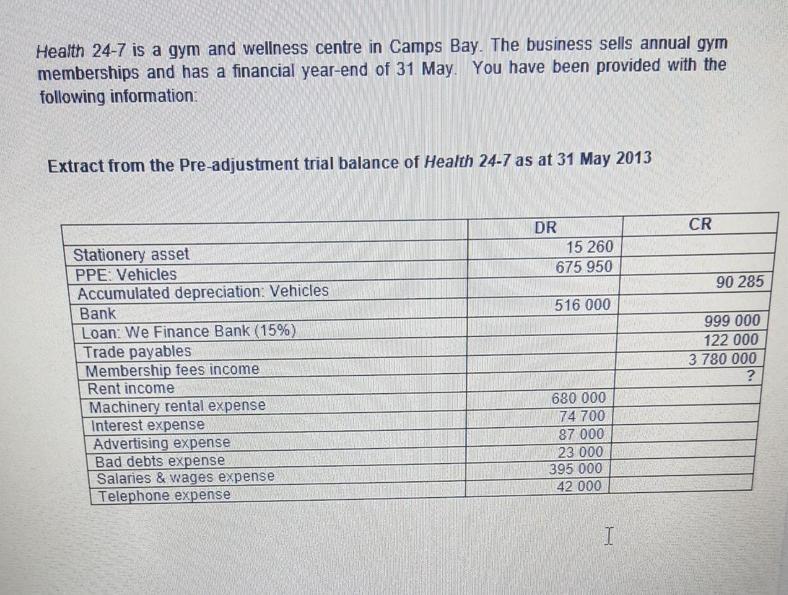

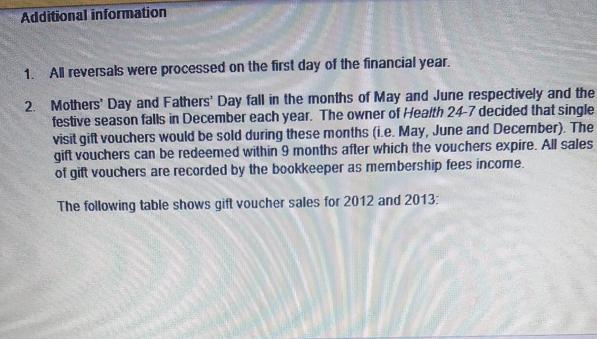

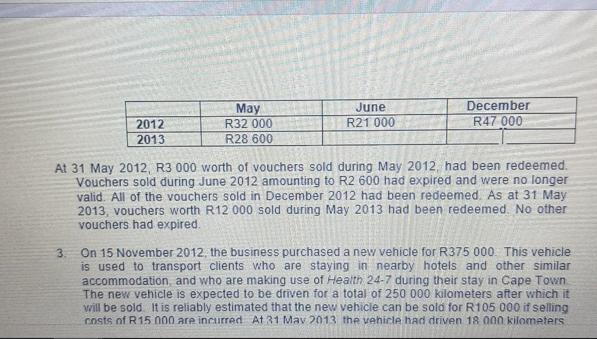

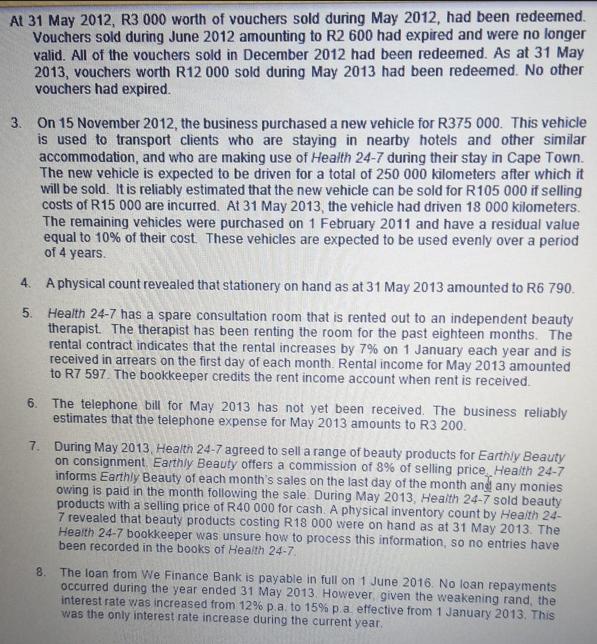

Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym memberships and has a financial year-end of 31 May. You have been provided with the following information: Extract from the Pre-adjustment trial balance of Health 24-7 as at 31 May 2013 Stationery asset PPE: Vehicles Accumulated depreciation: Vehicles Bank Loan: We Finance Bank (15%) Trade payables Membership fees income Rent income Machinery rental expense Interest expense Advertising expense Bad debts expense Salaries & wages expense Telephone expense DR 15 260 675 950 516 000 680 000 74 700 87 000 23 000 395 000 42 000 I CR 90 285 999 000 122 000 3 780 000 ? Additional information 1. All reversals were processed on the first day of the financial year. 2. Mothers' Day and Fathers' Day fall in the months of May and June respectively and the festive season falls in December each year. The owner of Health 24-7 decided that single visit gift vouchers would be sold during these months (i.e. May, June and December). The gift vouchers can be redeemed within 9 months after which the vouchers expire. All sales of gift vouchers are recorded by the bookkeeper as membership fees income. The following table shows gift voucher sales for 2012 and 2013: 2012 2013 May R32 000 R28 600 June R21 000 December R47 000 At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred At 31 May 2013 the vehicle had driven 18 000 kilometers At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town. The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred. At 31 May 2013, the vehicle had driven 18 000 kilometers. The remaining vehicles were purchased on 1 February 2011 and have a residual value equal to 10% of their cost. These vehicles are expected to be used evenly over a period of 4 years. 4. A physical count revealed that stationery on hand as at 31 May 2013 amounted to R6 790. Health 24-7 has a spare consultation room that is rented out to an independent beauty therapist. The therapist has been renting the room for the past eighteen months. The rental contract indicates that the rental increases by 7% on 1 January each year and is received in arrears on the first day of each month. Rental income for May 2013 amounted to R7 597. The bookkeeper credits the rent income account when rent is received. 5. 6. The telephone bill for May 2013 has not yet been received. The business reliably estimates that the telephone expense for May 2013 amounts to R3 200. 7. During May 2013, Health 24-7 agreed to sell a range of beauty products for Earthly Beauty on consignment, Earthly Beauty offers a commission of 8% of selling price Health 24-7 informs Earthly Beauty of each month's sales on the last day of the month and any monies owing is paid in the month following the sale. During May 2013, Health 24-7 sold beauty products with a selling price of R40 000 for cash. A physical inventory count by Health 24- 7 revealed that beauty products costing R18 000 were on hand as at 31 May 2013. The Health 24-7 bookkeeper was unsure how to process this information, so no entries have been recorded in the books of Health 24-7. 8. The loan from We Finance Bank is payable in full on 1 June 2016. No loan repayments occurred during the year ended 31 May 2013. However, given the weakening rand, the interest rate was increased from 12% p.a. to 15% p.a. effective from 1 January 2013. This was the only interest rate increase during the current year. 1. Refer to additional information 2 1.1. Prepare the reversing entry that would have been processed by Health 24-7 on 1 June 2012 in respect of gift vouchers. Ignore dates and narrations. (3 marks) I 1.2. Refer to your answer in 1.1 above. Explain why it is necessary for this reversing journal entry to be processed by the business. marks) (2 1.3. Explain briefly how the business will account for the expired vouchers that were sold during June 2012. Ensure that any relevant definitions are explained. marks) (3 1.4. Prepare the membership fees income account as it would appear in the general ledger of Health 24-7 for the year ended 31 May 2013. marks) (5 2. Refer to additional information 3 Prepare any adjusting journal entry/ies that would have been processed in respect of vehicles on 31 May 2013. Ignore dates and narrations. (8 marks) 3. Refer to additional information 5 4. Refer to additional information 7 Prepare any journal entry/ies that would have been processed in the books of Earthly Beauty on 31 May 2013. Closing entries are not required. Assume Earthly Beauty uses the periodic recording system. Ignore dates and narrations. (4 marks) 5. Refer to additional information 8 Prepare any adjusting journal entry/ies that would have been processed in respect of interest on 31 May 2013. Ignore dates and narrations. (5 marks) 6. After taking into account all additional information provided 6.1. Prepare the statement of comprehensive income of Health 24-7 for the year ended 31 May 2013. (9 marks) H 6.2. Prepare the total assets and the current liabilities sections of the statement of financial position of Health 24-7 as at 31 May 2013. (12 marks) Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym memberships and has a financial year-end of 31 May. You have been provided with the following information: Extract from the Pre-adjustment trial balance of Health 24-7 as at 31 May 2013 Stationery asset PPE: Vehicles Accumulated depreciation: Vehicles Bank Loan: We Finance Bank (15%) Trade payables Membership fees income Rent income Machinery rental expense Interest expense Advertising expense Bad debts expense Salaries & wages expense Telephone expense DR 15 260 675 950 516 000 680 000 74 700 87 000 23 000 395 000 42 000 I CR 90 285 999 000 122 000 3 780 000 ? Additional information 1. All reversals were processed on the first day of the financial year. 2. Mothers' Day and Fathers' Day fall in the months of May and June respectively and the festive season falls in December each year. The owner of Health 24-7 decided that single visit gift vouchers would be sold during these months (i.e. May, June and December). The gift vouchers can be redeemed within 9 months after which the vouchers expire. All sales of gift vouchers are recorded by the bookkeeper as membership fees income. The following table shows gift voucher sales for 2012 and 2013: 2012 2013 May R32 000 R28 600 June R21 000 December R47 000 At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred At 31 May 2013 the vehicle had driven 18 000 kilometers At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town. The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred. At 31 May 2013, the vehicle had driven 18 000 kilometers. The remaining vehicles were purchased on 1 February 2011 and have a residual value equal to 10% of their cost. These vehicles are expected to be used evenly over a period of 4 years. 4. A physical count revealed that stationery on hand as at 31 May 2013 amounted to R6 790. Health 24-7 has a spare consultation room that is rented out to an independent beauty therapist. The therapist has been renting the room for the past eighteen months. The rental contract indicates that the rental increases by 7% on 1 January each year and is received in arrears on the first day of each month. Rental income for May 2013 amounted to R7 597. The bookkeeper credits the rent income account when rent is received. 5. 6. The telephone bill for May 2013 has not yet been received. The business reliably estimates that the telephone expense for May 2013 amounts to R3 200. 7. During May 2013, Health 24-7 agreed to sell a range of beauty products for Earthly Beauty on consignment, Earthly Beauty offers a commission of 8% of selling price Health 24-7 informs Earthly Beauty of each month's sales on the last day of the month and any monies owing is paid in the month following the sale. During May 2013, Health 24-7 sold beauty products with a selling price of R40 000 for cash. A physical inventory count by Health 24- 7 revealed that beauty products costing R18 000 were on hand as at 31 May 2013. The Health 24-7 bookkeeper was unsure how to process this information, so no entries have been recorded in the books of Health 24-7. 8. The loan from We Finance Bank is payable in full on 1 June 2016. No loan repayments occurred during the year ended 31 May 2013. However, given the weakening rand, the interest rate was increased from 12% p.a. to 15% p.a. effective from 1 January 2013. This was the only interest rate increase during the current year. 1. Refer to additional information 2 1.1. Prepare the reversing entry that would have been processed by Health 24-7 on 1 June 2012 in respect of gift vouchers. Ignore dates and narrations. (3 marks) I 1.2. Refer to your answer in 1.1 above. Explain why it is necessary for this reversing journal entry to be processed by the business. marks) (2 1.3. Explain briefly how the business will account for the expired vouchers that were sold during June 2012. Ensure that any relevant definitions are explained. marks) (3 1.4. Prepare the membership fees income account as it would appear in the general ledger of Health 24-7 for the year ended 31 May 2013. marks) (5 2. Refer to additional information 3 Prepare any adjusting journal entry/ies that would have been processed in respect of vehicles on 31 May 2013. Ignore dates and narrations. (8 marks) 3. Refer to additional information 5 4. Refer to additional information 7 Prepare any journal entry/ies that would have been processed in the books of Earthly Beauty on 31 May 2013. Closing entries are not required. Assume Earthly Beauty uses the periodic recording system. Ignore dates and narrations. (4 marks) 5. Refer to additional information 8 Prepare any adjusting journal entry/ies that would have been processed in respect of interest on 31 May 2013. Ignore dates and narrations. (5 marks) 6. After taking into account all additional information provided 6.1. Prepare the statement of comprehensive income of Health 24-7 for the year ended 31 May 2013. (9 marks) H 6.2. Prepare the total assets and the current liabilities sections of the statement of financial position of Health 24-7 as at 31 May 2013. (12 marks)

Expert Answer:

Answer rating: 100% (QA)

11 Prepare the reversing entry that would have been processed by Health 247 on 1 June 2012 in respect of gift vouchers Ignore dates and narrations 3 marks Membership fees income 3 000 Deferred income ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Use the information given below to draw up the Statement of Comprehensive Income for TREK TRADING for the year ended 28 February 2017. Treck Trading Pre Adjustment trial Balance as at 28 February...

-

1. Microcontroller technology (5 marks) Perform a research study on the current state-of-the-art of microcontroller technology. The study shall cover but not limited to, a. Advancement of...

-

Which or the following results has the higher t value for a test of the null hypothesis that the average US passenger car gels 30 miles per gallon? Do not do any calculations; just explain your...

-

Codominance observable effect on the phenotype of a heter neither allele is recessive-both alleles are dominant. 6. Which of the genotypes results in a blood type that provides clear evidence of...

-

Mr Tile Company purchased merchandise on account from a supplier for $9,000, terms 2/10, n/30. MR Tile Company returned $1,500 of the merchandise and received full credit. a. If MR Tile Company pays...

-

The following data for Throwback Industries Inc. relate to the payroll for the week ended December 9, 2018 Hours Hourly Weekly Federal Employee Worked Rate Salary Income Tax Retirements Savings Aaron...

-

What are cross-cousin and parallel-cousin marriages and what are their effects?

-

Alert Companys shareholders equity prior to any of the following events is as follows: Preferred stock, 8%, ................$100,000 $100 par Common stock, $10 par .......... 150,000 Additional...

-

Define VM sprawl and discuss its impact on resource utilization and management in virtualized infrastructures. What strategies can be employed to mitigate VM sprawl and optimize resource allocation ?

-

For the following LP, identify three alternative optimal basic solutions, and then write a general expression for all the non-basic alternative optima comprising these three basic solutions. Maximize...

-

Back to your Canada widgets corporation facility, your director is delivering you some bad new. Apparently, both widget quality levels were below standards last quarter. Your director is looking to...

-

You are the Director of Human Resources at a city. Describe your responsibilities and tasks to fulfill the requirements of "Affirmative Action" in detail .

-

Explain the role of technological innovation and disruptive technologies, such as artificial intelligence (AI), blockchain, and 3D printing, in accelerating the transition towards sustainability,...

-

First, watch the crash course on 'Due Process' listed for this week and then read the short article on a Virginia fight club published by the Washington Post (link below and Word Doc at the bottom):...

-

Green Co. has a checking account at Red Bank and an interest-bearing savings account at Blue Bank. On December 31, Year 1, Green's bank records reflect the following information: Red Bank Bank...

-

Explain the concept and value of benchmarking, and define the differences between internal and external benchmarking. Describe at least 1 internal and 1 external benchmark that risk managers can use...

-

The following data represent the total number of 20 defective cordless iron in a particular production day. 2 3 5 7 8 9 10 13 13 15 15 15 18 19 19 20 23 26 28 29 i. Construct a frequency...

-

Ex. (17): the vector field F = x i-zj + yz k is defined over the volume of the cuboid given by 0x a,0 y b, 0zc, enclosing the surface S. Evaluate the surface integral ff, F. ds?

-

Which should be more important to the management of an entity, cash flow or in come? Explain your answer.

-

In 2015, Chin Corp. purchased a piece of land for $2,500,000. In 2018, the land was sold for $3,500,000. Required: Prepare the journal entry to record the sale of Chin Corp's land.

-

Read the part of Note 1 on the use of judgements, estimates, and assumptions. Why is this note included in the financial statements and why is it important? (In your answer discuss why estimates are...

-

In a stage of impulse-reaction turbine, steam enters with a speed of \(250 \mathrm{~m} / \mathrm{s}\) at an angle of \(30^{\circ}\) in the direction of blade motion. The mean blade speed is \(150...

-

A single row impulse turbine develops \(130 \mathrm{~kW}\) at a blade speed of \(180 \mathrm{~m} / \mathrm{s}\) using \(2 \mathrm{~kg} / \mathrm{s}\) of steam. The steam leaves the nozzle at \(400...

-

A simple impulse turbine has one ring of moving blades running at \(150 \mathrm{~m} / \mathrm{s}\). The absolute velocity of steam at exit from the stage is \(80 \mathrm{~m} / \mathrm{s}\) at an...

Study smarter with the SolutionInn App