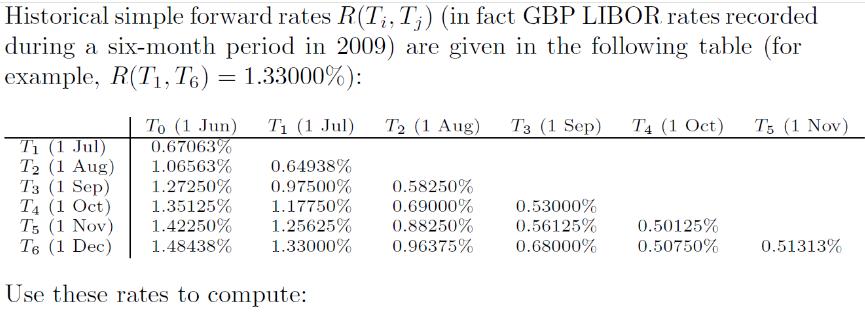

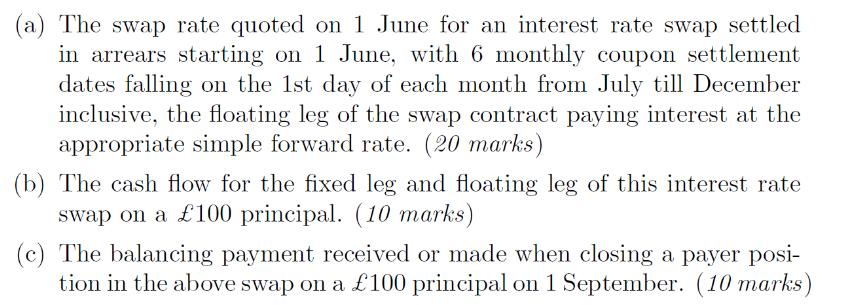

Historical simple forward rates R(Ti,Tj) (in fact GBP LIBOR rates recorded during a six-month period in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION a The swap rate quoted on 1 June for an interest rate swap settled in arrears starting on 1 June with 6 monthly coupon settlement dates falling on the 1st day of each month from July till Dec... View the full answer

Related Book For

Posted Date: