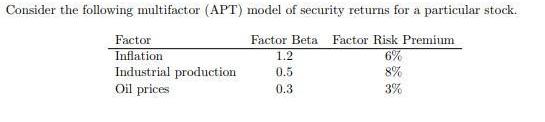

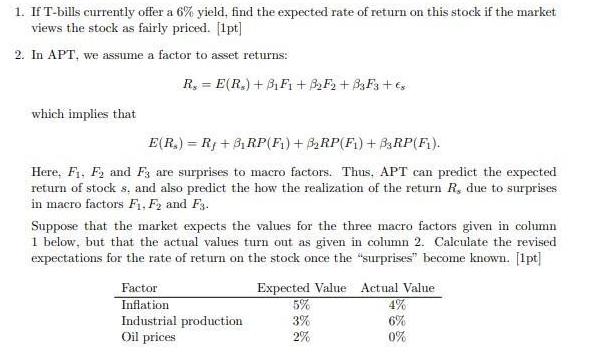

Consider the following multifactor (APT) model of security returns for a particular stock. Factor Beta Factor...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 To calculate the expected rate of return on the stock when the market views it as fairly priced we can use the APT model Expected Return RiskFree Rate Factor Beta1 Factor Risk Premium1 Factor Beta2 ... View the full answer

Related Book For

Accounting Principles

ISBN: 978-1118342190

11th Edition

Authors: Jerry Weygandt, Paul Kimmel, Donald Kieso

Posted Date: