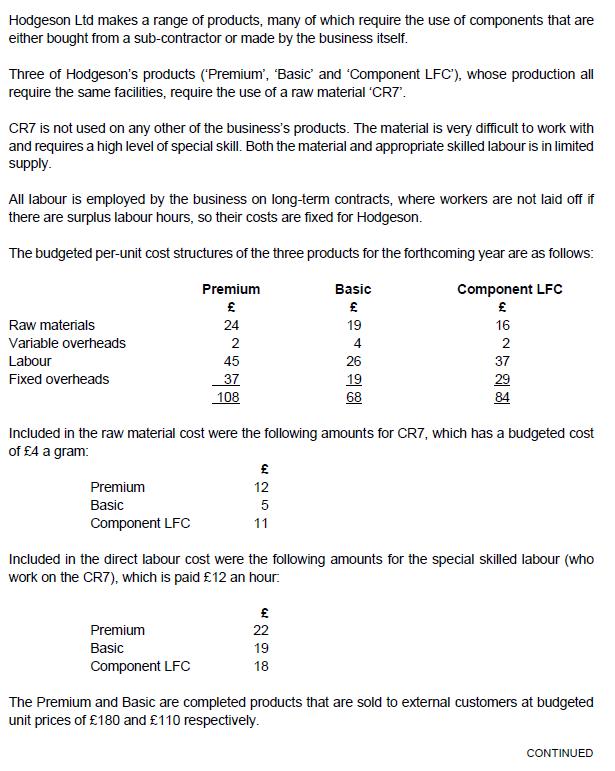

Hodgeson Ltd makes a range of products, many of which require the use of components that...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

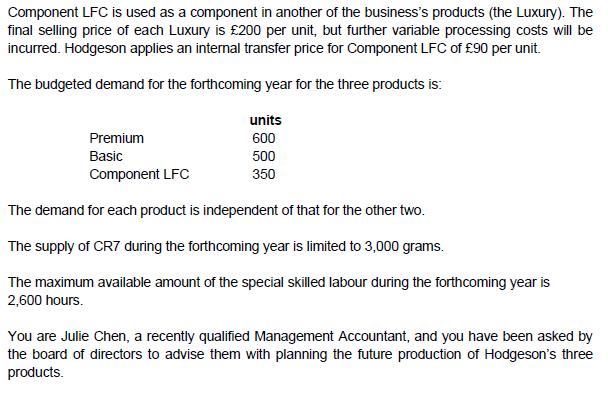

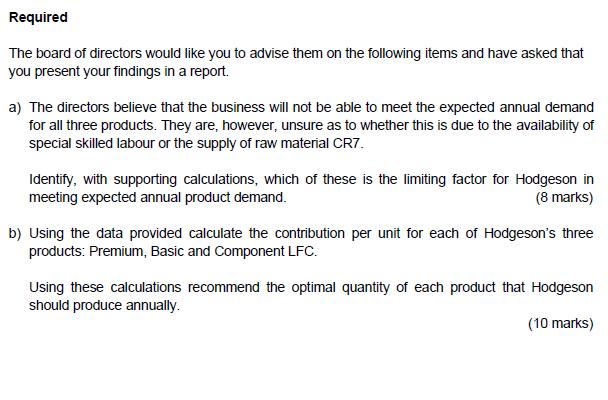

Hodgeson Ltd makes a range of products, many of which require the use of components that are either bought from a sub-contractor or made by the business itself. Three of Hodgeson's products ('Premium', "Basic and 'Component LFC'), whose production all require the same facilities, require the use of a raw material 'CR7". CR7 is not used on any other of the business's products. The material is very difficult to work with and requires a high level of special skill. Both the material and appropriate skilled labour is in limited supply. All labour is employed by the business on long-term contracts, where workers are not laid off if there are surplus labour hours, so their costs are fixed for Hodgeson. The budgeted per-unit cost structures of the three products for the forthcoming year are as follows: Premium Component LFC TIT Basic Raw materials 24 19 16 Variable overheads 2 4 2 Labour 45 26 37 Fixed overheads 37 108 19 68 29 84 Included in the raw material cost were the following amounts for CR7, which has a budgeted cost of £4 a gram: Premium 12 Basic Component LFC 11 Included in the direct labour cost were the following amounts for the special skilled labour (who work on the CR7), which is paid £12 an hour: Premium 22 Basic 19 Component LFC 18 The Premium and Basic are completed products that are sold to external customers at budgeted unit prices of £180 and £110 respectively. CONTINUED Component LFC is used as a component in another of the business's products (the Luxury). The final selling price of each Luxury is £200 per unit, but further variable processing costs will be incurred. Hodgeson applies an internal transfer price for Component LFC of £90 per unit. The budgeted demand for the forthcoming year for the three products is: units Premium 600 Basic 500 Component LFC 350 The demand for each product is independent of that for the other two. The supply of CR7 during the forthcoming year is limited to 3,000 grams. The maximum available amount of the special skilled labour during the forthcoming year is 2,600 hours. You are Julie Chen, a recently qualified Management Accountant, and you have been asked by the board of directors to advise them with planning the future production of Hodgeson's three products. Required The board of directors would like you to advise them on the following items and have asked that you present your findings in a report. a) The directors believe that the business will not be able to meet the expected annual demand for all three products. They are, however, unsure as to whether this is due to the availability of special skilled labour or the supply of raw material CR7. Identify, with supporting calculations, which of these is the limiting factor for Hodgeson in meeting expected annual product demand. (8 marks) b) Using the data provided calculate the contribution per unit for each of Hodgeson's three products: Premium, Basic and Component LFC. Using these calculations recommend the optimal quantity of each product that Hodgeson should produce annually. (10 marks) Hodgeson Ltd makes a range of products, many of which require the use of components that are either bought from a sub-contractor or made by the business itself. Three of Hodgeson's products ('Premium', "Basic and 'Component LFC'), whose production all require the same facilities, require the use of a raw material 'CR7". CR7 is not used on any other of the business's products. The material is very difficult to work with and requires a high level of special skill. Both the material and appropriate skilled labour is in limited supply. All labour is employed by the business on long-term contracts, where workers are not laid off if there are surplus labour hours, so their costs are fixed for Hodgeson. The budgeted per-unit cost structures of the three products for the forthcoming year are as follows: Premium Component LFC TIT Basic Raw materials 24 19 16 Variable overheads 2 4 2 Labour 45 26 37 Fixed overheads 37 108 19 68 29 84 Included in the raw material cost were the following amounts for CR7, which has a budgeted cost of £4 a gram: Premium 12 Basic Component LFC 11 Included in the direct labour cost were the following amounts for the special skilled labour (who work on the CR7), which is paid £12 an hour: Premium 22 Basic 19 Component LFC 18 The Premium and Basic are completed products that are sold to external customers at budgeted unit prices of £180 and £110 respectively. CONTINUED Component LFC is used as a component in another of the business's products (the Luxury). The final selling price of each Luxury is £200 per unit, but further variable processing costs will be incurred. Hodgeson applies an internal transfer price for Component LFC of £90 per unit. The budgeted demand for the forthcoming year for the three products is: units Premium 600 Basic 500 Component LFC 350 The demand for each product is independent of that for the other two. The supply of CR7 during the forthcoming year is limited to 3,000 grams. The maximum available amount of the special skilled labour during the forthcoming year is 2,600 hours. You are Julie Chen, a recently qualified Management Accountant, and you have been asked by the board of directors to advise them with planning the future production of Hodgeson's three products. Required The board of directors would like you to advise them on the following items and have asked that you present your findings in a report. a) The directors believe that the business will not be able to meet the expected annual demand for all three products. They are, however, unsure as to whether this is due to the availability of special skilled labour or the supply of raw material CR7. Identify, with supporting calculations, which of these is the limiting factor for Hodgeson in meeting expected annual product demand. (8 marks) b) Using the data provided calculate the contribution per unit for each of Hodgeson's three products: Premium, Basic and Component LFC. Using these calculations recommend the optimal quantity of each product that Hodgeson should produce annually. (10 marks) Hodgeson Ltd makes a range of products, many of which require the use of components that are either bought from a sub-contractor or made by the business itself. Three of Hodgeson's products ('Premium', "Basic and 'Component LFC'), whose production all require the same facilities, require the use of a raw material 'CR7". CR7 is not used on any other of the business's products. The material is very difficult to work with and requires a high level of special skill. Both the material and appropriate skilled labour is in limited supply. All labour is employed by the business on long-term contracts, where workers are not laid off if there are surplus labour hours, so their costs are fixed for Hodgeson. The budgeted per-unit cost structures of the three products for the forthcoming year are as follows: Premium Component LFC TIT Basic Raw materials 24 19 16 Variable overheads 2 4 2 Labour 45 26 37 Fixed overheads 37 108 19 68 29 84 Included in the raw material cost were the following amounts for CR7, which has a budgeted cost of £4 a gram: Premium 12 Basic Component LFC 11 Included in the direct labour cost were the following amounts for the special skilled labour (who work on the CR7), which is paid £12 an hour: Premium 22 Basic 19 Component LFC 18 The Premium and Basic are completed products that are sold to external customers at budgeted unit prices of £180 and £110 respectively. CONTINUED Component LFC is used as a component in another of the business's products (the Luxury). The final selling price of each Luxury is £200 per unit, but further variable processing costs will be incurred. Hodgeson applies an internal transfer price for Component LFC of £90 per unit. The budgeted demand for the forthcoming year for the three products is: units Premium 600 Basic 500 Component LFC 350 The demand for each product is independent of that for the other two. The supply of CR7 during the forthcoming year is limited to 3,000 grams. The maximum available amount of the special skilled labour during the forthcoming year is 2,600 hours. You are Julie Chen, a recently qualified Management Accountant, and you have been asked by the board of directors to advise them with planning the future production of Hodgeson's three products. Required The board of directors would like you to advise them on the following items and have asked that you present your findings in a report. a) The directors believe that the business will not be able to meet the expected annual demand for all three products. They are, however, unsure as to whether this is due to the availability of special skilled labour or the supply of raw material CR7. Identify, with supporting calculations, which of these is the limiting factor for Hodgeson in meeting expected annual product demand. (8 marks) b) Using the data provided calculate the contribution per unit for each of Hodgeson's three products: Premium, Basic and Component LFC. Using these calculations recommend the optimal quantity of each product that Hodgeson should produce annually. (10 marks) Hodgeson Ltd makes a range of products, many of which require the use of components that are either bought from a sub-contractor or made by the business itself. Three of Hodgeson's products ('Premium', "Basic and 'Component LFC'), whose production all require the same facilities, require the use of a raw material 'CR7". CR7 is not used on any other of the business's products. The material is very difficult to work with and requires a high level of special skill. Both the material and appropriate skilled labour is in limited supply. All labour is employed by the business on long-term contracts, where workers are not laid off if there are surplus labour hours, so their costs are fixed for Hodgeson. The budgeted per-unit cost structures of the three products for the forthcoming year are as follows: Premium Component LFC TIT Basic Raw materials 24 19 16 Variable overheads 2 4 2 Labour 45 26 37 Fixed overheads 37 108 19 68 29 84 Included in the raw material cost were the following amounts for CR7, which has a budgeted cost of £4 a gram: Premium 12 Basic Component LFC 11 Included in the direct labour cost were the following amounts for the special skilled labour (who work on the CR7), which is paid £12 an hour: Premium 22 Basic 19 Component LFC 18 The Premium and Basic are completed products that are sold to external customers at budgeted unit prices of £180 and £110 respectively. CONTINUED Component LFC is used as a component in another of the business's products (the Luxury). The final selling price of each Luxury is £200 per unit, but further variable processing costs will be incurred. Hodgeson applies an internal transfer price for Component LFC of £90 per unit. The budgeted demand for the forthcoming year for the three products is: units Premium 600 Basic 500 Component LFC 350 The demand for each product is independent of that for the other two. The supply of CR7 during the forthcoming year is limited to 3,000 grams. The maximum available amount of the special skilled labour during the forthcoming year is 2,600 hours. You are Julie Chen, a recently qualified Management Accountant, and you have been asked by the board of directors to advise them with planning the future production of Hodgeson's three products. Required The board of directors would like you to advise them on the following items and have asked that you present your findings in a report. a) The directors believe that the business will not be able to meet the expected annual demand for all three products. They are, however, unsure as to whether this is due to the availability of special skilled labour or the supply of raw material CR7. Identify, with supporting calculations, which of these is the limiting factor for Hodgeson in meeting expected annual product demand. (8 marks) b) Using the data provided calculate the contribution per unit for each of Hodgeson's three products: Premium, Basic and Component LFC. Using these calculations recommend the optimal quantity of each product that Hodgeson should produce annually. (10 marks)

Expert Answer:

Answer rating: 100% (QA)

a Limiting Factor Answer Raw Material CR7 is the limiting factor Working i Calculations for quantity of the material CR7 required for meeting the tota... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

A company makes a range of products with total budgeted manufacturing overheads of 973 560 incurred in three production departments (A, B and C) and one service department. Department A has 10 direct...

-

Ltd manufactures a range of products which are sold to a limited number of wholesale outlets. Four of these products are manufactured in a particular department on common equipment. No other...

-

5. Great Products Ltd has a range of products which are in regular demand but needs to introduce new products from time to time to maintain profitability. The following shows the forecast Income...

-

Daniel and Karen Chapman have three children, aged 2, 8 and 11 at the end of the year. The 8 year old is blind and therefore qualifies for the disability tax credit. The other two are in good mental...

-

You have selected two random samples of size 50, one from Population 1 and one from Population 2. You intend to use the samples to test the following hypotheses regarding the difference in means for...

-

1. What types of work behaviors did AIG intend to encourage through its retention bonus plan? 2. Which needs seem to be important to the employees of AIGs Financial Products unit? 3. Using the model...

-

Use Table 1, or software, to find (a) \(B(8 ; 16,0.40)\); (b) \(b(8 ; 16,0.40)\); (c) \(B(9 ; 12,0.60)\); (d) \(b(9 ; 12,0.60)\); (e) \(\sum_{k=6}^{20} b(k ; 20,0.15)\); (f) \(\sum_{k=6}^{9} b(k ;...

-

Use the Rolling Hills, Inc. data from Problem P14-34A. Requirements 1. Prepare the 2018 statement of cash flows by the direct method. 2. How will what you learned in this problem help you evaluate an...

-

A farmer is currently growing wheat and plans to sell it in September next year. He needs to plan his budget now, because of upcoming expenses. Suppose that the futures price of wheat for September...

-

Reba Dixon is a fifth-grade school teacher who earned a salary of $38,000 in 2020. She is 45 years old and has been divorced for four years. She receives $1,200 of alimony payments each month from...

-

Assume the role of a newly hired HR Director of a tech company, the CEO has asked you to prepare an HR Strategy Plan which ensures that your company draws inspiration from successful global companies...

-

What are restrictive covenants and when are they used?

-

Which graphics presentation likely plays the smallest role in an investigation? 1. Association matrix 2. Link charts 3. Flow diagrams 4. Timelines

-

How do individual codes of ethics help to overcome the power of groupthink?

-

What are the major differences between agency law in the United States and (a) agency law in Japan, and (b) agency law in the European Union?

-

What is TRIPS and what does it protect?

-

Calculate the contribution per mile and total annualcontribution associated with accepting FHP??s proposal. What do yourecommend? (Use 52 weeks per year in yourcalculations.)FHP offered a total o 2...

-

Danielle has an insurance policy with a premium of $75 per month. In September she is in an accident and receives a bill worth $2990 for the repair of her own property. Her deductible is $250 and her...

-

Trimake Limited makes three main products, using broadly the same production methods and equipment for each. A conventional product costing system is used at present, although an activity-based...

-

A company using process costing manufactures a single product which passes through two processes, the output of process 1 becoming the input to process 2. Normal losses and abnormal losses are...

-

The directors of The Healthy Eating Group (HEG), a successful restaurant chain, which commenced trading in 1998, have decided to enter the sandwich market in Homeland, its country of operation. It...

-

N = 230, n = 15, k = 200 Compute the mean and standard deviation of the hypergeometric random variable X.

-

N = 60, n = 8, k = 25 Compute the mean and standard deviation of the hypergeometric random variable X.

-

One study showed that in a certain year, airline fatalities occur at the rate of 0.011 deaths per 100 million miles. Find the probability that, during the next 100 million miles of flight, there will...

Study smarter with the SolutionInn App