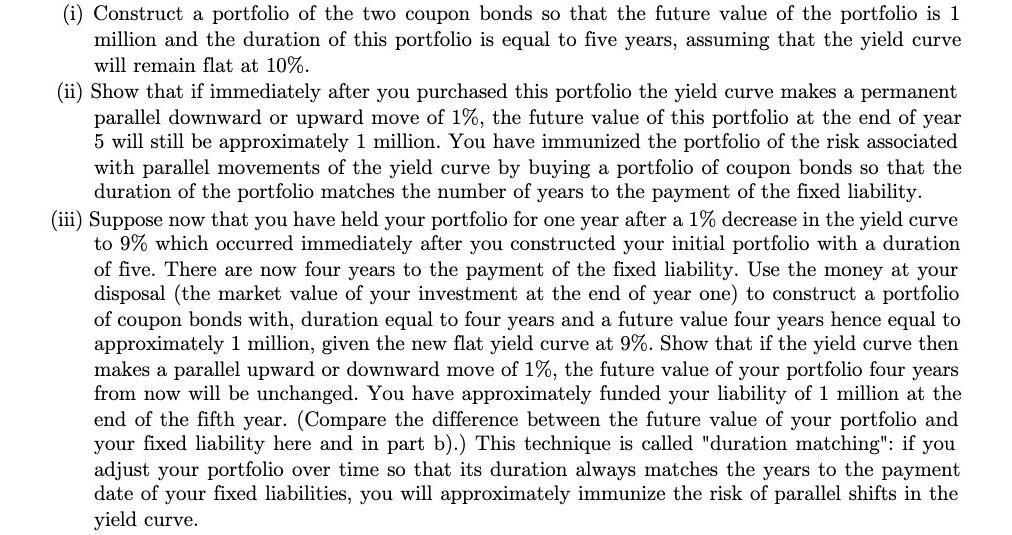

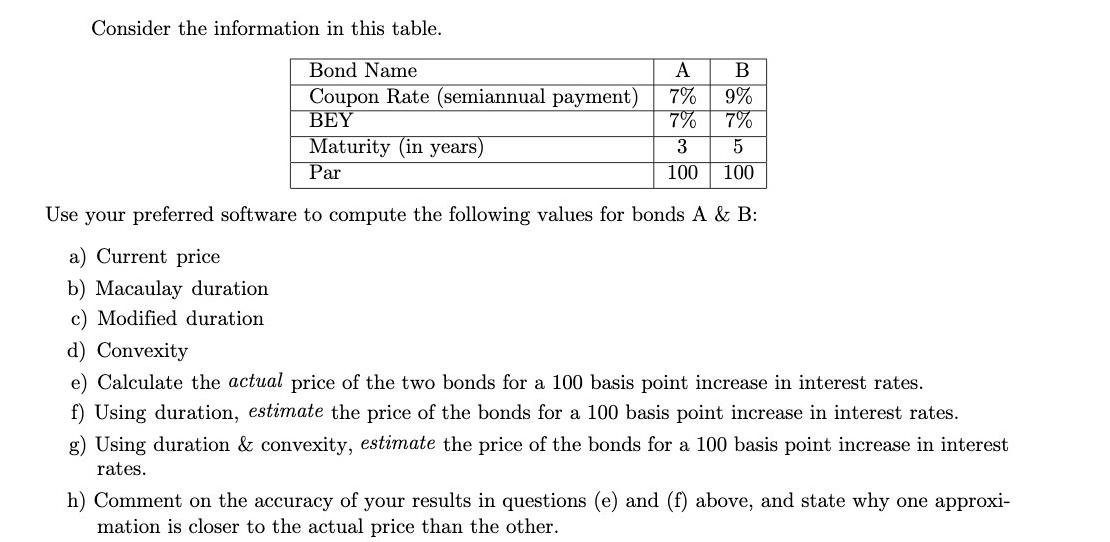

(i) Construct a portfolio of the two coupon bonds so that the future value of the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

i Construct a portfolio of the two coupon bonds so that the future value of the portfolio is 1 million and the duration of this portfolio is equal to five years assuming that the yield curve will rema... View the full answer

Related Book For

Posted Date: