Question 1 Soda Crush Media Pte Ltd (Soda Crush), a Singapore incorporated company, is in the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

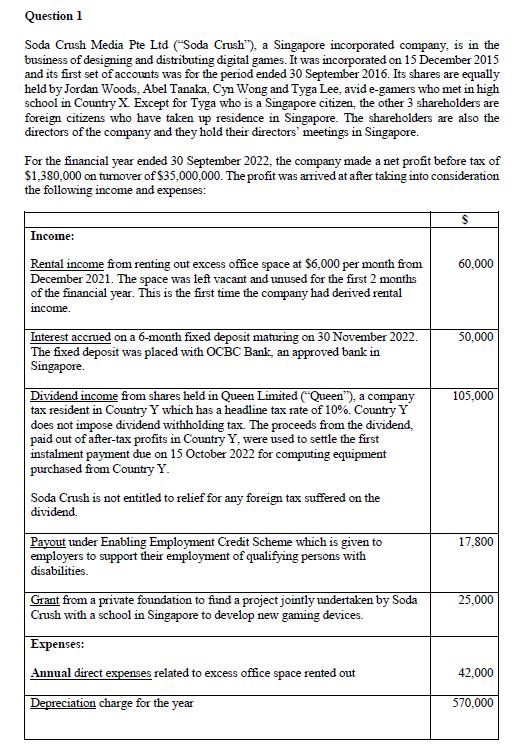

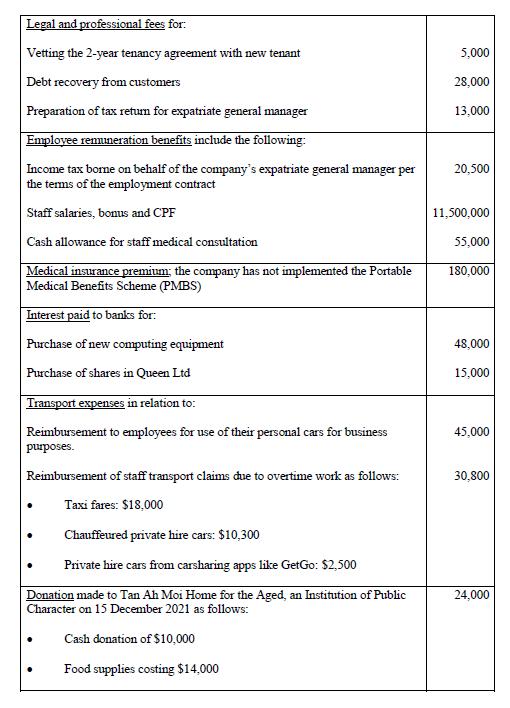

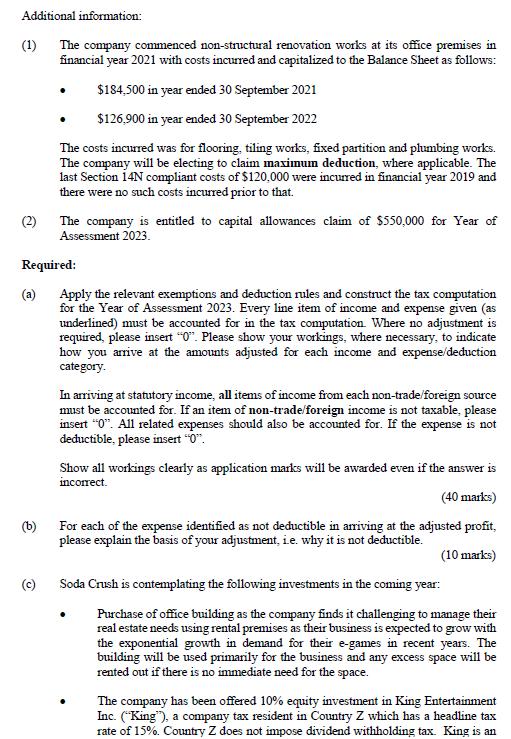

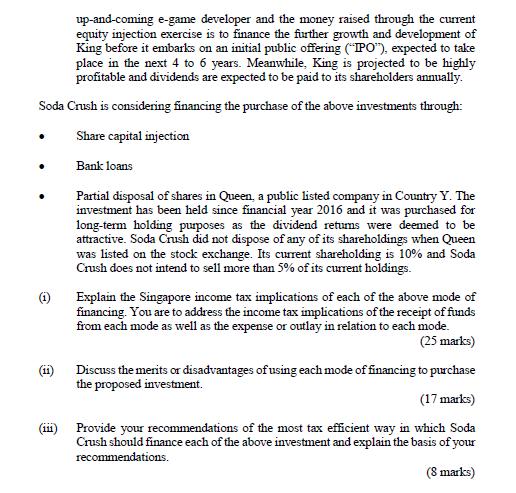

Question 1 Soda Crush Media Pte Ltd ("Soda Crush"), a Singapore incorporated company, is in the business of designing and distributing digital games. It was incorporated on 15 December 2015 and its first set of accounts was for the period ended 30 September 2016. Its shares are equally held by Jordan Woods, Abel Tanaka, Cyn Wong and Tyga Lee, avid e-gamers who met in high school in Country X Except for Tyga who is a Singapore citizen, the other 3 shareholders are foreign citizens who have taken up residence in Singapore. The shareholders are also the directors of the company and they hold their directors' meetings in Singapore. For the financial year ended 30 September 2022, the company made a net profit before tax of $1,380,000 on turnover of $35,000,000. The profit was arrived at after taking into consideration the following income and expenses: Income: S Rental income from renting out excess office space at $6,000 per month from December 2021. The space was left vacant and unused for the first 2 months of the financial year. This is the first time the company had derived rental 60,000 income. Interest accrued on a 6-month fixed deposit maturing on 30 November 2022. The fixed deposit was placed with OCBC Bank, an approved bank in Singapore. 50,000 Dividend income from shares held in Queen Limited ("Queen"), a company tax resident in Country Y which has a headline tax rate of 10%. Country Y does not impose dividend withholding tax. The proceeds from the dividend, paid out of after-tax profits in Country Y, were used to settle the first instalment payment due on 15 October 2022 for computing equipment purchased from Country Y. 105,000 Soda Crush is not entitled to relief for any foreign tax suffered on the dividend. Payout under Enabling Employment Credit Scheme which is given to employers to support their employment of qualifying persons with disabilities. 17,800 Grant from a private foundation to fund a project jointly undertaken by Soda Crush with a school in Singapore to develop new gaming devices. 25,000 Expenses: Annual direct expenses related to excess office space rented out 42,000 Depreciation charge for the year 570,000 Legal and professional fees for: Vetting the 2-year tenancy agreement with new tenant Debt recovery from customers Preparation of tax retum for expatriate general manager 5,000 28,000 13,000 Employee remuneration benefits include the following: Income tax borne on behalf of the company's expatriate general manager per the terms of the employment contract 20,500 Staff salaries, bonus and CPF 11,500,000 Cash allowance for staff medical consultation 55,000 Medical insurance premium; the company has not implemented the Portable Medical Benefits Scheme (PMBS) 180,000 Interest paid to banks for: Purchase of new computing equipment Purchase of shares in Queen Ltd 48,000 15,000 Transport expenses in relation to: Reimbursement to employees for use of their personal cars for business purposes. 45,000 Reimbursement of staff transport claims due to overtime work as follows: 30,800 Taxi fares: $18,000 Chauffeured private hire cars: $10,300 Private hire cars from carsharing apps like GetGo: $2,500 Donation made to Tan Ah Moi Home for the Aged, an Institution of Public Character on 15 December 2021 as follows: 24,000 Cash donation of $10,000 Food supplies costing $14,000 Additional information: (1) The company commenced non-structural renovation works at its office premises in financial year 2021 with costs incurred and capitalized to the Balance Sheet as follows: • $184,500 in year ended 30 September 2021 $126,900 in year ended 30 September 2022 The costs incurred was for flooring, tiling works, fixed partition and plumbing works. The company will be electing to claim maximum deduction, where applicable. The last Section 14N compliant costs of $120,000 were incurred in financial year 2019 and there were no such costs incurred prior to that. (2) The company is entitled to capital allowances claim of $550,000 for Year of Assessment 2023. Required: (a) Apply the relevant exemptions and deduction rules and construct the tax computation for the Year of Assessment 2023. Every line item of income and expense given (as underlined) must be accounted for in the tax computation. Where no adjustment is required, please insert "0". Please show your workings, where necessary, to indicate how you arrive at the amounts adjusted for each income and expense/deduction category. In arriving at statutory income, all items of income from each non-trade/foreign source must be accounted for. If an item of non-trade/foreign income is not taxable, please insert "0". All related expenses should also be accounted for. If the expense is not deductible, please insert "0". Show all workings clearly as application marks will be awarded even if the answer is incorrect. (b) (40 marks) For each of the expense identified as not deductible in arriving at the adjusted profit, please explain the basis of your adjustment, i.e. why it is not deductible. (10 marks) (c) Soda Crush is contemplating the following investments in the coming year: Purchase of office building as the company finds it challenging to manage their real estate needs using rental premises as their business is expected to grow with the exponential growth in demand for their e-games in recent years. The building will be used primarily for the business and any excess space will be rented out if there is no immediate need for the space. The company has been offered 10% equity investment in King Entertainment Inc. ("King"), a company tax resident in Country Z which has a headline tax rate of 15%. Country Z does not impose dividend withholding tax. King is an up-and-coming e-game developer and the money raised through the current equity injection exercise is to finance the further growth and development of King before it embarks on an initial public offering (IPO"), expected to take place in the next 4 to 6 years. Meanwhile, King is projected to be highly profitable and dividends are expected to be paid to its shareholders annually. Soda Crush is considering financing the purchase of the above investments through: . • (i) (111) Share capital injection Bank loans Partial disposal of shares in Queen, a public listed company in Country Y. The investment has been held since financial year 2016 and it was purchased for long-term holding purposes as the dividend retums were deemed to be attractive. Soda Crush did not dispose of any of its shareholdings when Queen was listed on the stock exchange. Its current shareholding is 10% and Soda Crush does not intend to sell more than 5% of its current holdings. Explain the Singapore income tax implications of each of the above mode of financing. You are to address the income tax implications of the receipt of funds from each mode as well as the expense or outlay in relation to each mode. (25 marks) Discuss the merits or disadvantages of using each mode of financing to purchase the proposed investment. (17 marks) Provide your recommendations of the most tax efficient way in which Soda Crush should finance each of the above investment and explain the basis of your recommendations. (8 marks) Question 1 Soda Crush Media Pte Ltd ("Soda Crush"), a Singapore incorporated company, is in the business of designing and distributing digital games. It was incorporated on 15 December 2015 and its first set of accounts was for the period ended 30 September 2016. Its shares are equally held by Jordan Woods, Abel Tanaka, Cyn Wong and Tyga Lee, avid e-gamers who met in high school in Country X Except for Tyga who is a Singapore citizen, the other 3 shareholders are foreign citizens who have taken up residence in Singapore. The shareholders are also the directors of the company and they hold their directors' meetings in Singapore. For the financial year ended 30 September 2022, the company made a net profit before tax of $1,380,000 on turnover of $35,000,000. The profit was arrived at after taking into consideration the following income and expenses: Income: S Rental income from renting out excess office space at $6,000 per month from December 2021. The space was left vacant and unused for the first 2 months of the financial year. This is the first time the company had derived rental 60,000 income. Interest accrued on a 6-month fixed deposit maturing on 30 November 2022. The fixed deposit was placed with OCBC Bank, an approved bank in Singapore. 50,000 Dividend income from shares held in Queen Limited ("Queen"), a company tax resident in Country Y which has a headline tax rate of 10%. Country Y does not impose dividend withholding tax. The proceeds from the dividend, paid out of after-tax profits in Country Y, were used to settle the first instalment payment due on 15 October 2022 for computing equipment purchased from Country Y. 105,000 Soda Crush is not entitled to relief for any foreign tax suffered on the dividend. Payout under Enabling Employment Credit Scheme which is given to employers to support their employment of qualifying persons with disabilities. 17,800 Grant from a private foundation to fund a project jointly undertaken by Soda Crush with a school in Singapore to develop new gaming devices. 25,000 Expenses: Annual direct expenses related to excess office space rented out 42,000 Depreciation charge for the year 570,000 Legal and professional fees for: Vetting the 2-year tenancy agreement with new tenant Debt recovery from customers Preparation of tax retum for expatriate general manager 5,000 28,000 13,000 Employee remuneration benefits include the following: Income tax borne on behalf of the company's expatriate general manager per the terms of the employment contract 20,500 Staff salaries, bonus and CPF 11,500,000 Cash allowance for staff medical consultation 55,000 Medical insurance premium; the company has not implemented the Portable Medical Benefits Scheme (PMBS) 180,000 Interest paid to banks for: Purchase of new computing equipment Purchase of shares in Queen Ltd 48,000 15,000 Transport expenses in relation to: Reimbursement to employees for use of their personal cars for business purposes. 45,000 Reimbursement of staff transport claims due to overtime work as follows: 30,800 Taxi fares: $18,000 Chauffeured private hire cars: $10,300 Private hire cars from carsharing apps like GetGo: $2,500 Donation made to Tan Ah Moi Home for the Aged, an Institution of Public Character on 15 December 2021 as follows: 24,000 Cash donation of $10,000 Food supplies costing $14,000 Additional information: (1) The company commenced non-structural renovation works at its office premises in financial year 2021 with costs incurred and capitalized to the Balance Sheet as follows: • $184,500 in year ended 30 September 2021 $126,900 in year ended 30 September 2022 The costs incurred was for flooring, tiling works, fixed partition and plumbing works. The company will be electing to claim maximum deduction, where applicable. The last Section 14N compliant costs of $120,000 were incurred in financial year 2019 and there were no such costs incurred prior to that. (2) The company is entitled to capital allowances claim of $550,000 for Year of Assessment 2023. Required: (a) Apply the relevant exemptions and deduction rules and construct the tax computation for the Year of Assessment 2023. Every line item of income and expense given (as underlined) must be accounted for in the tax computation. Where no adjustment is required, please insert "0". Please show your workings, where necessary, to indicate how you arrive at the amounts adjusted for each income and expense/deduction category. In arriving at statutory income, all items of income from each non-trade/foreign source must be accounted for. If an item of non-trade/foreign income is not taxable, please insert "0". All related expenses should also be accounted for. If the expense is not deductible, please insert "0". Show all workings clearly as application marks will be awarded even if the answer is incorrect. (b) (40 marks) For each of the expense identified as not deductible in arriving at the adjusted profit, please explain the basis of your adjustment, i.e. why it is not deductible. (10 marks) (c) Soda Crush is contemplating the following investments in the coming year: Purchase of office building as the company finds it challenging to manage their real estate needs using rental premises as their business is expected to grow with the exponential growth in demand for their e-games in recent years. The building will be used primarily for the business and any excess space will be rented out if there is no immediate need for the space. The company has been offered 10% equity investment in King Entertainment Inc. ("King"), a company tax resident in Country Z which has a headline tax rate of 15%. Country Z does not impose dividend withholding tax. King is an up-and-coming e-game developer and the money raised through the current equity injection exercise is to finance the further growth and development of King before it embarks on an initial public offering (IPO"), expected to take place in the next 4 to 6 years. Meanwhile, King is projected to be highly profitable and dividends are expected to be paid to its shareholders annually. Soda Crush is considering financing the purchase of the above investments through: . • (i) (111) Share capital injection Bank loans Partial disposal of shares in Queen, a public listed company in Country Y. The investment has been held since financial year 2016 and it was purchased for long-term holding purposes as the dividend retums were deemed to be attractive. Soda Crush did not dispose of any of its shareholdings when Queen was listed on the stock exchange. Its current shareholding is 10% and Soda Crush does not intend to sell more than 5% of its current holdings. Explain the Singapore income tax implications of each of the above mode of financing. You are to address the income tax implications of the receipt of funds from each mode as well as the expense or outlay in relation to each mode. (25 marks) Discuss the merits or disadvantages of using each mode of financing to purchase the proposed investment. (17 marks) Provide your recommendations of the most tax efficient way in which Soda Crush should finance each of the above investment and explain the basis of your recommendations. (8 marks)

Expert Answer:

Answer rating: 100% (QA)

The following are the adjustments needed to calculate the taxable income for Soda Crush Media Pte Ltd for the financial year ended 30 September 2022 1 ... View the full answer

Related Book For

Business Statistics A Decision Making Approach

ISBN: 9780133021844

9th Edition

Authors: David F. Groebner, Patrick W. Shannon, Phillip C. Fry

Posted Date:

Students also viewed these accounting questions

-

CANMNMM January of this year. (a) Each item will be held in a record. Describe all the data structures that must refer to these records to implement the required functionality. Describe all the...

-

Julie Phillips is the Little Pear Administration Pty Ltd Managing Director. She has been in the company for 8 years but her position is no longer needed due to a recent outsourcing strategy. She...

-

= Adobe Reader Touch Type here to search Active Research: Toyota's Hybrid Offer One of the most successful hybrid cars (cars that run on both battery and gasoline) is the Prius by Toyota. Visit...

-

Look at Table 25.1. How would the initial break-even operating lease rate change if rapid technological change in limo manufacturing reduces the costs of new limos by 5% per year? Table 25.1 Tear 2 3...

-

In this exercise, you modify the Savings Account application from this chapters Apply lesson. Use Windows to make a copy of the Savings Solution folder. Rename the copy Savings Solution-Advanced....

-

What stakeholder affected by their behavior was Gilead weighting very lightly when it decided what to tell the FDA about the medicines it wished to have permission to sell?

-

Partnership Income and Basis Adjustments. Mark and Pamela are equal partners in MP partnership. The partnership, Mark, and Pamela are calendar year taxpayers. The partnership incurred the following...

-

Even method: 1- Algorithm Compare between recursion and iteration 2- Memory representation (Ex: EVEV (0,10)) recursion iteration

-

This question will ask you to use the Specific factor model to analyse how a change in the relative price of textiles and IT services affects income inequality. Assume that there are two consumption...

-

Sapphire Ltd has a complex capital structure that includes both ordinary shares and potential ordinary shares. Sapphire Ltd reported the following net profit and dividends information for the current...

-

The following unadjusted trial balance is for Power Demolition Company at its April 30 current fiscal year-end. The credit balance of the Retained Earnings account was $76,900 on April 30 of the...

-

The following unadjusted trial balance is for Ace Construction Co. at its June 30 current fiscal year-end. The credit balance of the Retained Earnings account was $78,660 on June 30 of the prior...

-

On 1 January 20x1, ACE Corporation introduced a share appreciation rights (SARs) plan for 20 selected senior managers. Under the plan, each manager was granted 10,000 share appreciation rights, which...

-

Star Corporation is a provider of computer software and IT services in two large regions of Easter Europe. The company uses 12 percent to evaluate investments; however, due to latest developments it...

-

Why does the study of international economics usually begin with the presentation of international trade theory? Why must we discuss theories before examining policies? Which aspects of international...

-

Organizations are increasing their use of personality tests to screen job applicants. What are some of the advantages and disadvantages of this approach? What can managers do to avoid some of the...

-

The housing market in the United States saw a major decrease in value between 2007 and 2008. The file titled House contains the data on average and median housing prices between November 2007 and...

-

You are given the following data: a. Construct a frequency distribution for these data. b. Based on the frequency distribution, develop a histogram. c. Construct a relative frequency distribution. d....

-

Suppose a random sample of 137 households in Detroit was selected to determine the average annual household spending on food at home for Detroit residents. The sample results are contained in the...

-

Example In January 2004, a Mars Exploration Rover touched down on the surface of Mars and rolled out for exploration ( Figure

-

A battery-operated wall clock no longer keeps timeneither hand moves. Develop a hypothesis explaining why it fails to work, and then make a prediction that permits you to test your hypothesis....

-

Does the snowflake have rotational symmetry in Figure 1.6? If yes, describe the ways in which the flake can be rotated without changing its appearance. Does it have reflection symmetry? If yes,...

Study smarter with the SolutionInn App