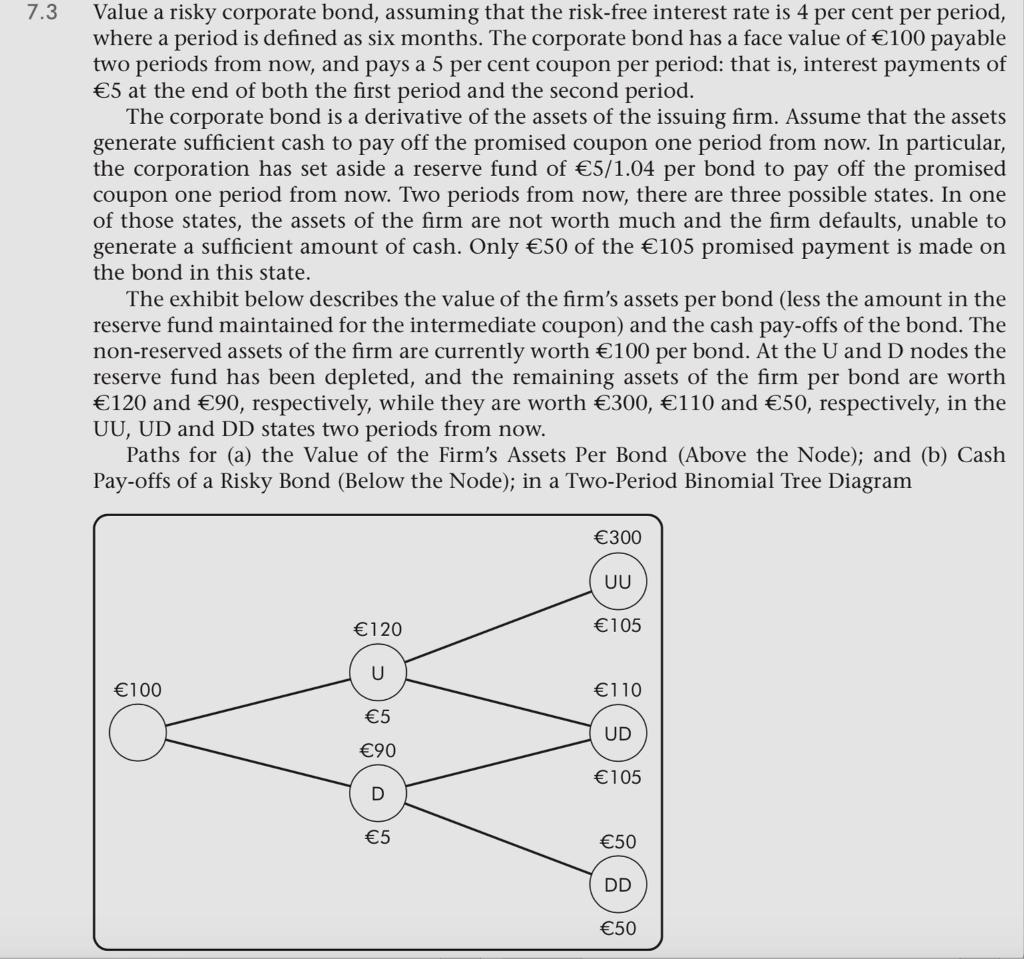

7.4 In many instances, whether a cash flow occurs early or not is a decision of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

students name institution instructors name course title due date Using the binomial option pricing m... View the full answer

Related Book For

Fundamentals of corporate finance

ISBN: 978-0470876442

2nd Edition

Authors: Robert Parrino, David S. Kidwell, Thomas W. Bates

Posted Date: