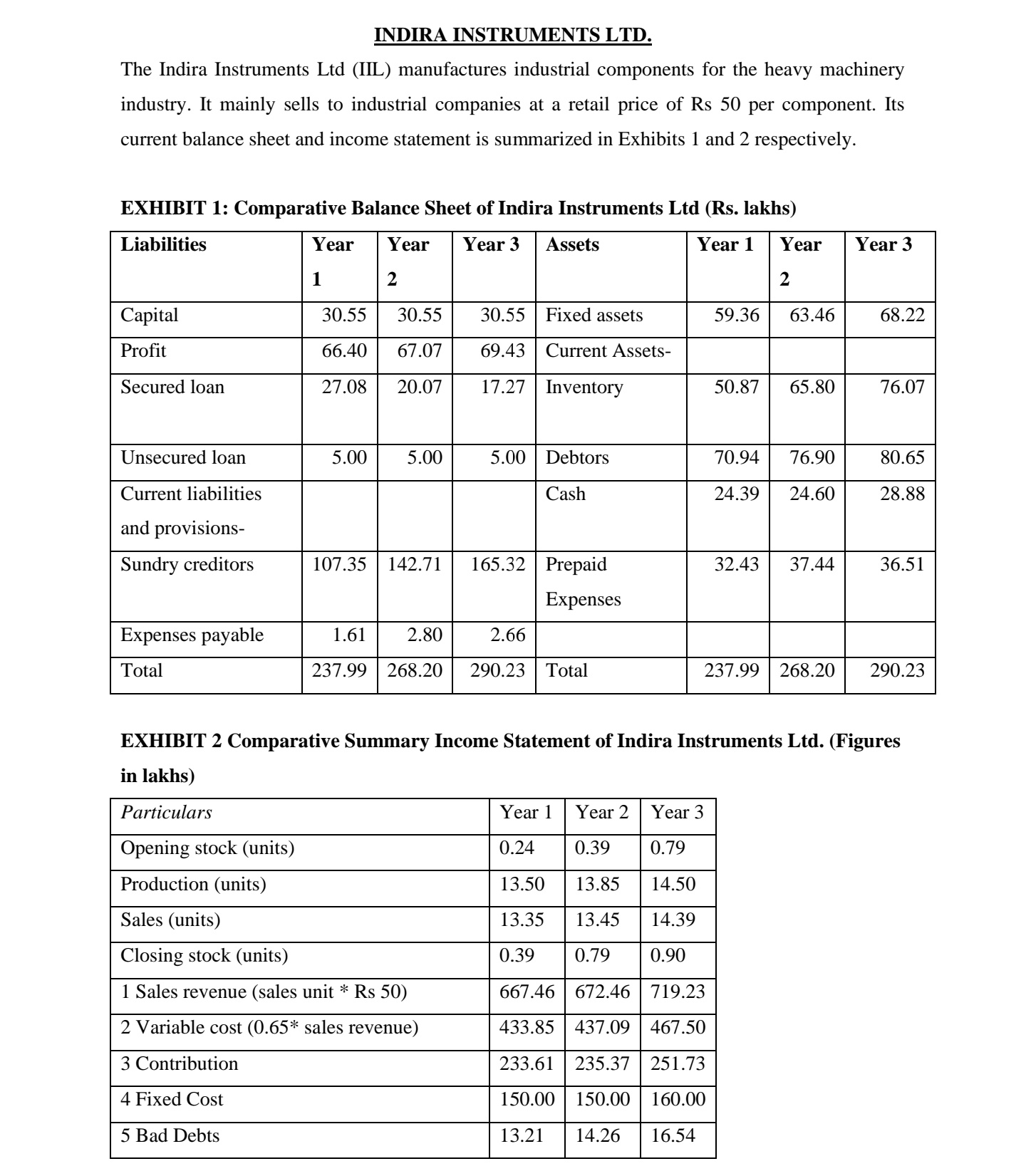

INDIRA INSTRUMENTS LTD. The Indira Instruments Ltd (IIL) manufactures industrial components for the heavy machinery industry....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

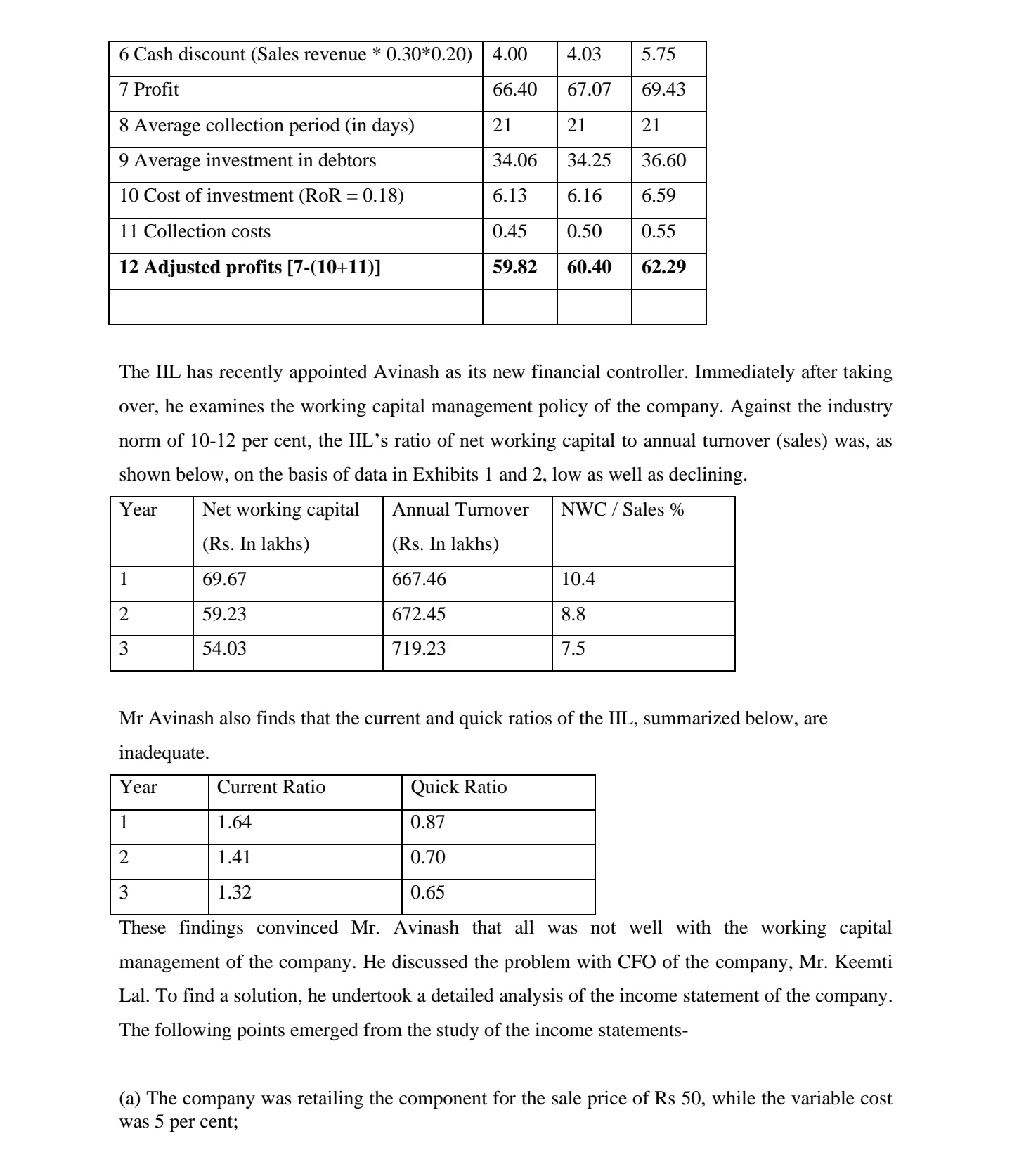

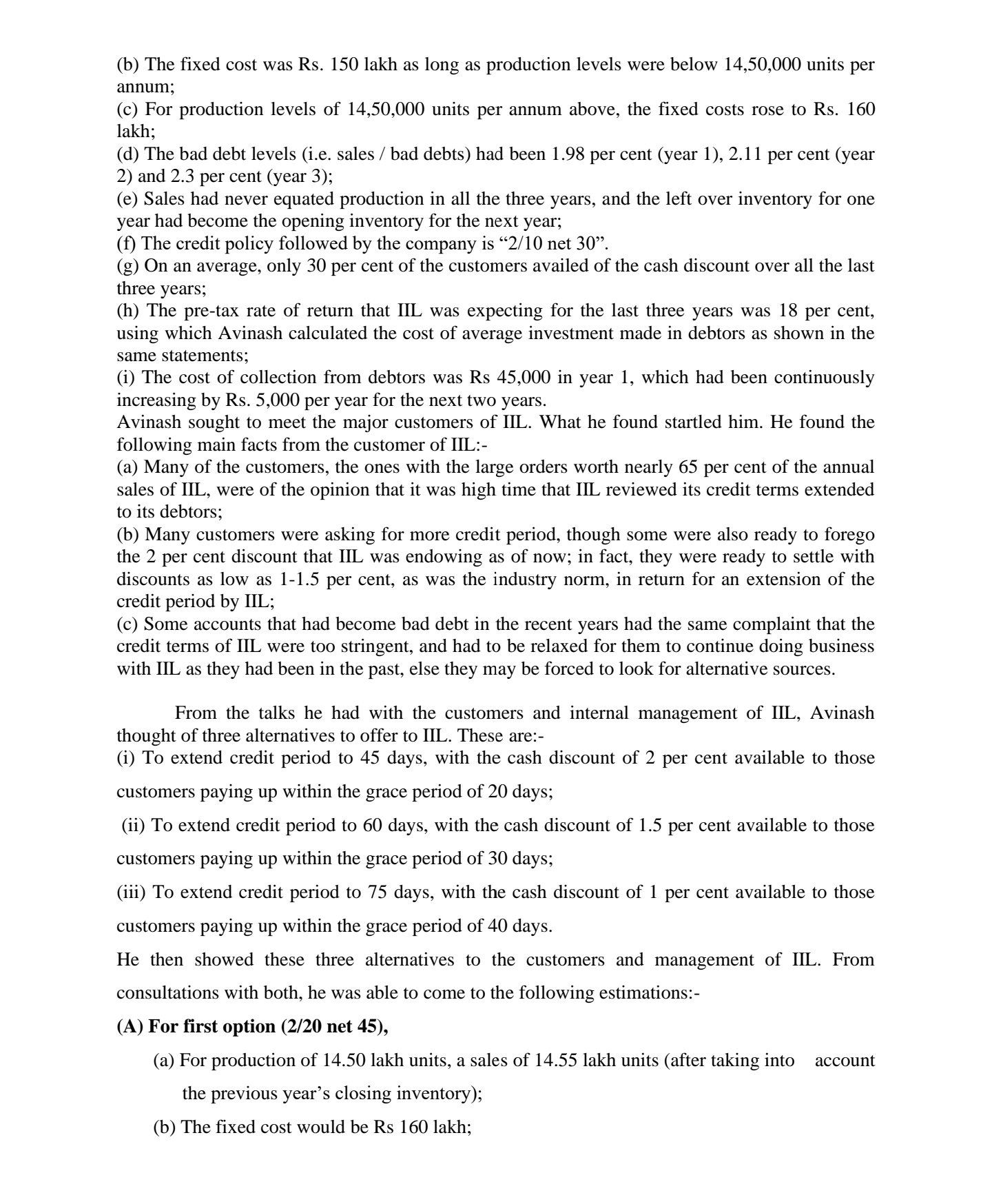

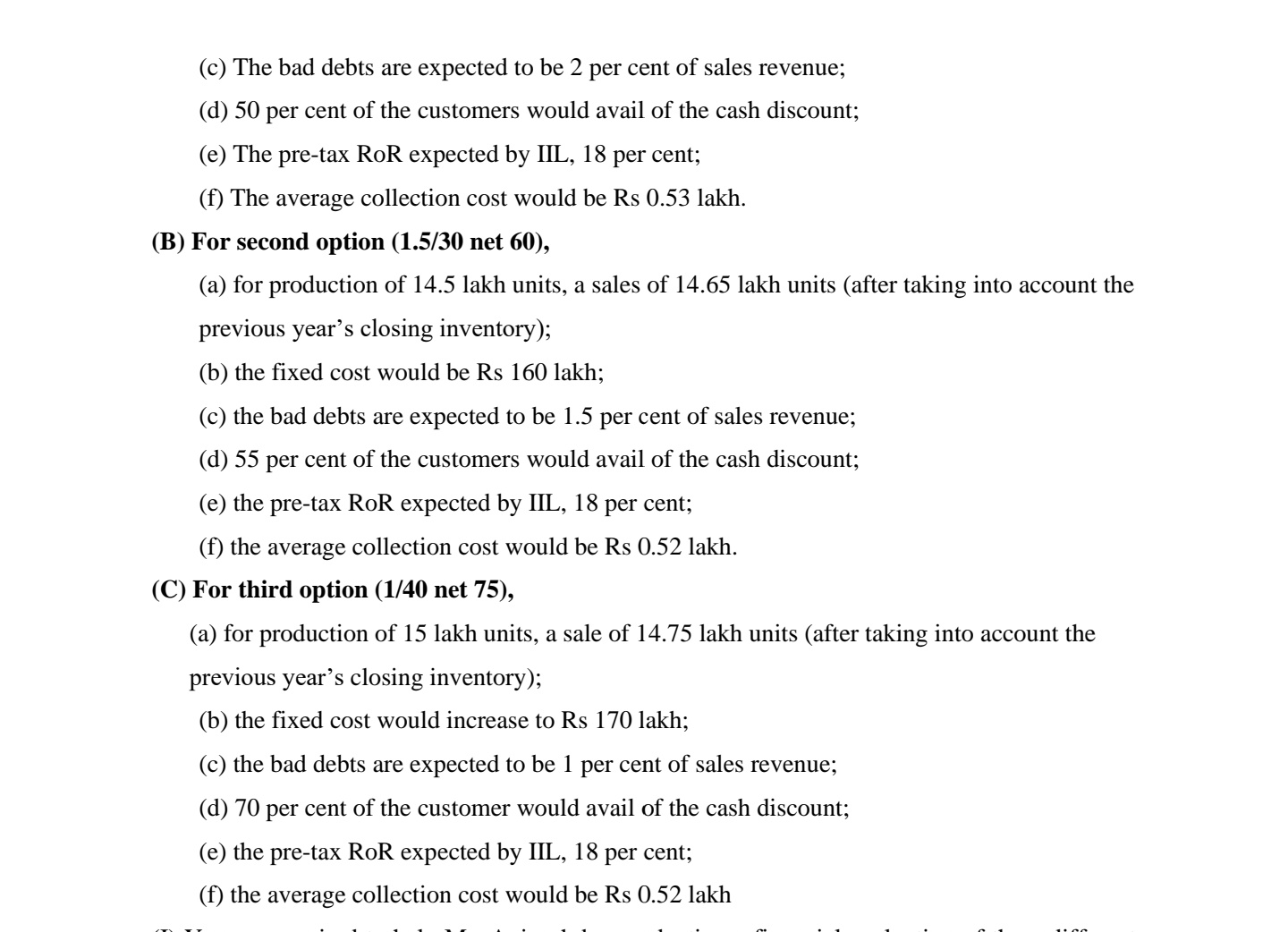

INDIRA INSTRUMENTS LTD. The Indira Instruments Ltd (IIL) manufactures industrial components for the heavy machinery industry. It mainly sells to industrial companies at retail price of Rs 50 per component. Its current balance sheet and income statement is summarized in Exhibits 1 and 2 respectively. EXHIBIT 1: Comparative Balance Sheet of Indira Instruments Ltd (Rs. lakhs) Liabilities Year Year Year 3 Year 1 1 2 Capital Profit Secured loan Unsecured loan Current liabilities and provisions- Sundry creditors Expenses payable Total 30.55 30.55 Fixed assets 67.07 69.43 Current Assets- Assets 30.55 66.40 27.08 20.07 17.27 Inventory 5.00 5.00 5.00 Debtors Cash 107.35 142.71 165.32 Prepaid Expenses 1.61 2.80 2.66 237.99 268.20 290.23 Total Sales (units) Closing stock (units) 1 Sales revenue (sales unit * Rs 50) 2 Variable cost (0.65* sales revenue) 3 Contribution 4 Fixed Cost 5 Bad Debts 59.36 Year 1 Year 2 Year 3 0.24 0.39 0.79 13.50 13.85 14.50 13.35 13.45 14.39 0.39 0.79 0.90 667.46 672.46 719.23 433.85 437.09 467.50 233.61 235.37 251.73 150.00 150.00 160.00 13.21 14.26 16.54 Year 2 63.46 50.87 65.80 32.43 70.94 76.90 24.39 24.60 37.44 Year 3 68.22 76.07 80.65 28.88 36.51 237.99 268.20 290.23 EXHIBIT 2 Comparative Summary Income Statement of Indira Instruments Ltd. (Figures in lakhs) Particulars Opening stock (units) Production (units) 6 Cash discount (Sales revenue * 0.30*0.20) | 4.00 7 Profit 66.40 21 34.06 6.13 0.45 59.82 8 Average collection period (in days) 9 Average investment in debtors 10 Cost of investment (RoR = 0.18) 11 Collection costs 12 Adjusted profits [7-(10+11)] The III has recently appointed Avinash as its new financial controller. Immediately after taking over, he examines the working capital management policy of the company. Against the industry norm of 10-12 per cent, the IIL's ratio of net working capital to annual turnover (sales) was, as shown below, on the basis of data in Exhibits 1 and 2, low as well as declining. Year Annual Turnover NWC/ Sales % Net working capital (Rs. In lakhs) (Rs. In lakhs) 69.67 667.46 59.23 672.45 54.03 719.23 1 2 3 4.03 5.75 67.07 69.43 21 21 34.25 36.60 6.16 6.59 0.50 0.55 60.40 62.29 Mr Avinash also finds that the current and quick ratios of the IIL, summarized below, are inadequate. Year 1 2 3 10.4 8.8 7.5 Current Ratio 1.64 1.41 1.32 Quick Ratio 0.87 0.70 0.65 These findings convinced Mr. Avinash that all was not well with the working capital management of the company. He discussed the problem with CFO of the company, Mr. Keemti Lal. To find a solution, he undertook a detailed analysis of the income statement of the company. The following points emerged from the study of the income statements- (a) The company was retailing the component for the sale price of Rs 50, while the variable cost was 5 per cent; (b) The fixed cost was Rs. 150 lakh as long as production levels were below 14,50,000 units per annum; (c) For production levels of 14,50,000 units per annum above, the fixed costs rose to Rs. 160 lakh; (d) The bad debt levels (i.e. sales / bad debts) had been 1.98 per cent (year 1), 2.11 per cent (year 2) and 2.3 per cent (year 3); (e) Sales had never equated production in all the three years, and the left over inventory for one year had become the opening inventory for the next year; (f) The credit policy followed by the company is "2/10 net 30". (g) On an average, only 30 per cent of the customers availed of the cash discount over all the last three years; (h) The pre-tax rate of return that IIL was expecting for the last three years was 18 per cent, using which Avinash calculated the cost of average investment made in debtors as shown in the same statements; (i) The cost of collection from debtors was Rs 45,000 in year 1, which had been continuously increasing by Rs. 5,000 per year for the next two years. Avinash sought to meet the major customers of IIL. What he found startled him. He found the following main facts from the customer of IIL:- (a) Many of the customers, the ones with the large orders worth nearly 65 per cent of the annual sales of IIL, were of the opinion that it was high time that IIL reviewed its credit terms extended to its debtors; (b) Many customers were asking for more credit period, though some were also ready to forego the 2 per cent discount that IIL was endowing as of now; in fact, they were ready to settle with discounts as low as 1-1.5 per cent, as was the industry norm, in return for an extension of the credit period by IIL; (c) Some accounts that had become bad debt in the recent years had the same complaint that the credit terms of IIL were too stringent, and had to be relaxed for them to continue doing business with IIL as they had been in the past, else they may be forced to look for alternative sources. From the talks he had with the customers and internal management of IIL, Avinash thought of three alternatives to offer to IIL. These are:- (i) To extend credit period to 45 days, with the cash discount of 2 per cent available to those customers paying up within the grace period of 20 days; (ii) To extend credit period to 60 days, with the cash discount of 1.5 per cent available to those customers paying up within the grace period of 30 days; (iii) To extend credit period to 75 days, with the cash discount of 1 per cent available to those customers paying up within the grace period of 40 days. He then showed these three alternatives to the customers and management of IIL. From consultations with both, he was able to come to the following estimations:- (A) For first option (2/20 net 45), (a) For production of 14.50 lakh units, a sales of 14.55 lakh units (after taking into account the previous year's closing inventory); (b) The fixed cost would be Rs 160 lakh; (c) The bad debts are expected to be 2 per cent of sales revenue; (d) 50 per cent of the customers would avail of the cash discount; (e) The pre-tax RoR expected by IIL, 18 per cent; (f) The average collection cost would be Rs 0.53 lakh. (B) For second option (1.5/30 net 60), (a) for production of 14.5 lakh units, a sales of 14.65 lakh units (after taking into account the previous year's closing inventory); (b) the fixed cost would be Rs 160 lakh; (c) the bad debts are expected to be 1.5 per cent of sales revenue; (d) 55 per cent of the customers would avail of the cash discount; (e) the pre-tax RoR expected by IIL, 18 (f) the average collection cost would be Rs 0.52 lakh. (C) For third option (1/40 net 75), (a) for production of 15 lakh units, a sale of 14.75 lakh units (after taking into account the previous year's closing inventory); (b) the fixed cost would increase to Rs 170 lakh; (c) the bad debts are expected to be 1 per cent of sales revenue; (d) 70 per cent of the customer would avail of the cash discount; (e) the pre-tax RoR expected by IIL, 18 per cent; (f) the average collection cost would be Rs 0.52 lakh per cent; INDIRA INSTRUMENTS LTD. The Indira Instruments Ltd (IIL) manufactures industrial components for the heavy machinery industry. It mainly sells to industrial companies at retail price of Rs 50 per component. Its current balance sheet and income statement is summarized in Exhibits 1 and 2 respectively. EXHIBIT 1: Comparative Balance Sheet of Indira Instruments Ltd (Rs. lakhs) Liabilities Year Year Year 3 Year 1 1 2 Capital Profit Secured loan Unsecured loan Current liabilities and provisions- Sundry creditors Expenses payable Total 30.55 30.55 Fixed assets 67.07 69.43 Current Assets- Assets 30.55 66.40 27.08 20.07 17.27 Inventory 5.00 5.00 5.00 Debtors Cash 107.35 142.71 165.32 Prepaid Expenses 1.61 2.80 2.66 237.99 268.20 290.23 Total Sales (units) Closing stock (units) 1 Sales revenue (sales unit * Rs 50) 2 Variable cost (0.65* sales revenue) 3 Contribution 4 Fixed Cost 5 Bad Debts 59.36 Year 1 Year 2 Year 3 0.24 0.39 0.79 13.50 13.85 14.50 13.35 13.45 14.39 0.39 0.79 0.90 667.46 672.46 719.23 433.85 437.09 467.50 233.61 235.37 251.73 150.00 150.00 160.00 13.21 14.26 16.54 Year 2 63.46 50.87 65.80 32.43 70.94 76.90 24.39 24.60 37.44 Year 3 68.22 76.07 80.65 28.88 36.51 237.99 268.20 290.23 EXHIBIT 2 Comparative Summary Income Statement of Indira Instruments Ltd. (Figures in lakhs) Particulars Opening stock (units) Production (units) 6 Cash discount (Sales revenue * 0.30*0.20) | 4.00 7 Profit 66.40 21 34.06 6.13 0.45 59.82 8 Average collection period (in days) 9 Average investment in debtors 10 Cost of investment (RoR = 0.18) 11 Collection costs 12 Adjusted profits [7-(10+11)] The III has recently appointed Avinash as its new financial controller. Immediately after taking over, he examines the working capital management policy of the company. Against the industry norm of 10-12 per cent, the IIL's ratio of net working capital to annual turnover (sales) was, as shown below, on the basis of data in Exhibits 1 and 2, low as well as declining. Year Annual Turnover NWC/ Sales % Net working capital (Rs. In lakhs) (Rs. In lakhs) 69.67 667.46 59.23 672.45 54.03 719.23 1 2 3 4.03 5.75 67.07 69.43 21 21 34.25 36.60 6.16 6.59 0.50 0.55 60.40 62.29 Mr Avinash also finds that the current and quick ratios of the IIL, summarized below, are inadequate. Year 1 2 3 10.4 8.8 7.5 Current Ratio 1.64 1.41 1.32 Quick Ratio 0.87 0.70 0.65 These findings convinced Mr. Avinash that all was not well with the working capital management of the company. He discussed the problem with CFO of the company, Mr. Keemti Lal. To find a solution, he undertook a detailed analysis of the income statement of the company. The following points emerged from the study of the income statements- (a) The company was retailing the component for the sale price of Rs 50, while the variable cost was 5 per cent; (b) The fixed cost was Rs. 150 lakh as long as production levels were below 14,50,000 units per annum; (c) For production levels of 14,50,000 units per annum above, the fixed costs rose to Rs. 160 lakh; (d) The bad debt levels (i.e. sales / bad debts) had been 1.98 per cent (year 1), 2.11 per cent (year 2) and 2.3 per cent (year 3); (e) Sales had never equated production in all the three years, and the left over inventory for one year had become the opening inventory for the next year; (f) The credit policy followed by the company is "2/10 net 30". (g) On an average, only 30 per cent of the customers availed of the cash discount over all the last three years; (h) The pre-tax rate of return that IIL was expecting for the last three years was 18 per cent, using which Avinash calculated the cost of average investment made in debtors as shown in the same statements; (i) The cost of collection from debtors was Rs 45,000 in year 1, which had been continuously increasing by Rs. 5,000 per year for the next two years. Avinash sought to meet the major customers of IIL. What he found startled him. He found the following main facts from the customer of IIL:- (a) Many of the customers, the ones with the large orders worth nearly 65 per cent of the annual sales of IIL, were of the opinion that it was high time that IIL reviewed its credit terms extended to its debtors; (b) Many customers were asking for more credit period, though some were also ready to forego the 2 per cent discount that IIL was endowing as of now; in fact, they were ready to settle with discounts as low as 1-1.5 per cent, as was the industry norm, in return for an extension of the credit period by IIL; (c) Some accounts that had become bad debt in the recent years had the same complaint that the credit terms of IIL were too stringent, and had to be relaxed for them to continue doing business with IIL as they had been in the past, else they may be forced to look for alternative sources. From the talks he had with the customers and internal management of IIL, Avinash thought of three alternatives to offer to IIL. These are:- (i) To extend credit period to 45 days, with the cash discount of 2 per cent available to those customers paying up within the grace period of 20 days; (ii) To extend credit period to 60 days, with the cash discount of 1.5 per cent available to those customers paying up within the grace period of 30 days; (iii) To extend credit period to 75 days, with the cash discount of 1 per cent available to those customers paying up within the grace period of 40 days. He then showed these three alternatives to the customers and management of IIL. From consultations with both, he was able to come to the following estimations:- (A) For first option (2/20 net 45), (a) For production of 14.50 lakh units, a sales of 14.55 lakh units (after taking into account the previous year's closing inventory); (b) The fixed cost would be Rs 160 lakh; (c) The bad debts are expected to be 2 per cent of sales revenue; (d) 50 per cent of the customers would avail of the cash discount; (e) The pre-tax RoR expected by IIL, 18 per cent; (f) The average collection cost would be Rs 0.53 lakh. (B) For second option (1.5/30 net 60), (a) for production of 14.5 lakh units, a sales of 14.65 lakh units (after taking into account the previous year's closing inventory); (b) the fixed cost would be Rs 160 lakh; (c) the bad debts are expected to be 1.5 per cent of sales revenue; (d) 55 per cent of the customers would avail of the cash discount; (e) the pre-tax RoR expected by IIL, 18 (f) the average collection cost would be Rs 0.52 lakh. (C) For third option (1/40 net 75), (a) for production of 15 lakh units, a sale of 14.75 lakh units (after taking into account the previous year's closing inventory); (b) the fixed cost would increase to Rs 170 lakh; (c) the bad debts are expected to be 1 per cent of sales revenue; (d) 70 per cent of the customer would avail of the cash discount; (e) the pre-tax RoR expected by IIL, 18 per cent; (f) the average collection cost would be Rs 0.52 lakh per cent;

Expert Answer:

Answer rating: 100% (QA)

Okay lets solve this problem without drawing a table Given the following data 3 4 Sales 2005 2006 2007 2050742 1789429 2248511 2008 2600000 2009 2010 ... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these finance questions

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

The 2017 comparative balance sheet and income statement of 4 Seasons Supply Corp. follow. 4 Seasons had no non-cash investing and financing transactions during 2017. During the year, there were no...

-

for a manufacturing company product costs include all of the following except direct material overhead costs research and development costs direct labor costs

-

Nervana Soy Products (NSP) buys soybeans and processes them into other soy products. Each ton of soybeans that NSP purchases for $350 can be converted for an additional $210 into 650 pounds of soy...

-

Custom Truck Builders frequently uses long-term lease contracts to finance the sale of its trucks. On November 1, 2015, Custom Truck Builders leased to Interstate Van Lines a truck carried in the...

-

Refer to the information from QS 21-18. Compute the variable overhead spending variance and the variable overhead efficiency variance and classify each as favorable or unfavorable. Data From QS 21-18...

-

Determining and interpreting flexible budget variances Use the standard price and cost data supplied in Problem 8-18A. Assume that Todhunter actually produced and sold 31,000 books. The actual sales...

-

A car traveling 87.0 km/h is 1500 m behind a truck traveling at 74.0 km/h. How far from its initial position does the car have to travel to catch up to the truck.

-

You, CPA, are working as the controller for a video game development company called All Starr Games Inc. (All Starr). The company develops sports-related games, and its recent virtual rugby game was...

-

Donor places $100,000 in trust for 11 years, income to be paid to A, remainder to Donor. The Donor is not the trustee. Indicate whether the transfer constitutes a complete gift or an incomplete gift...

-

-15x+10 divided by 5 6x2+10 DIVIDED BY 2 14X3+28X2-70 DIVIDED BY 7 USE DIVISION AND DISTRIBUTIVE PROPERTY TO SIMPLIFY

-

The hydraulic and sediment conditions of an alluvial channel are as follows: water discharge Q1000 ft/s, width W = 50 ft, depth D = 4 ft, velocity V = 5 ft/s, slope S=0.006, doo = 50 mm, dso = 25 mm,...

-

How do advanced practitioners of accountability leverage data analytics and performance metrics to monitor progress, identify areas for improvement, and drive continuous learning and growth within...

-

Qualitative Research Study Consider the following question: Discuss the 2 key roles of the researcher in Participant Observation research studies. How can each of them contribute to the success or...

-

In what ways can individuals and organizations navigate the complexities of cross-functional collaboration and interdependence while maintaining clarity and accountability for roles,...

-

You are provided with information on income and expenditure of domestic workers from a census of population and housing. Income (X) 60 80 100 120 140 Expenditure (Y) 50 79 80 110 120 41 50 95 115 140...

-

On 1 July 2018, Parent Ltd acquired all the shares of Son Ltd, on a cum-div. basis, for $2,057,000. At this date, the equity of Son Ltd consisted of: $ 1,000,000 Share capital 500 000 shares...

-

Exhibit 4.22 presents selected operating data for three retailers for a recent year. Macy??s operates several department store chains selling consumer products such as brand-name clothing, china,...

-

The concept of accounting quality has several dimensions, but two characteristics often dominate: the accounting information should be a fair representation of performance for the reporting period,...

-

The chapter describes how the dividends valuation approach measures value-relevant dividends to encompass various transactions between the firm and the common shareholders. What transactions should...

-

At January 1, 2015, Cheng Company reported retained earnings of 20,000,000. In 2015, Cheng discovered that 2014 depreciation expense was understated by 4,000,000. In 2015, net income was 9,000,000...

-

Cherokee Construction Company changed from the cost-recovery to the percentage-of-completion method of accounting for long-term construction contracts during 2015. For tax purposes, the company...

-

In 2015, Bailey Corporation discovered that equipment purchased on January 1, 2013, for 50,000 was expensed at that time. The equipment should have been depreciated over 5 years, with no residual...

Study smarter with the SolutionInn App