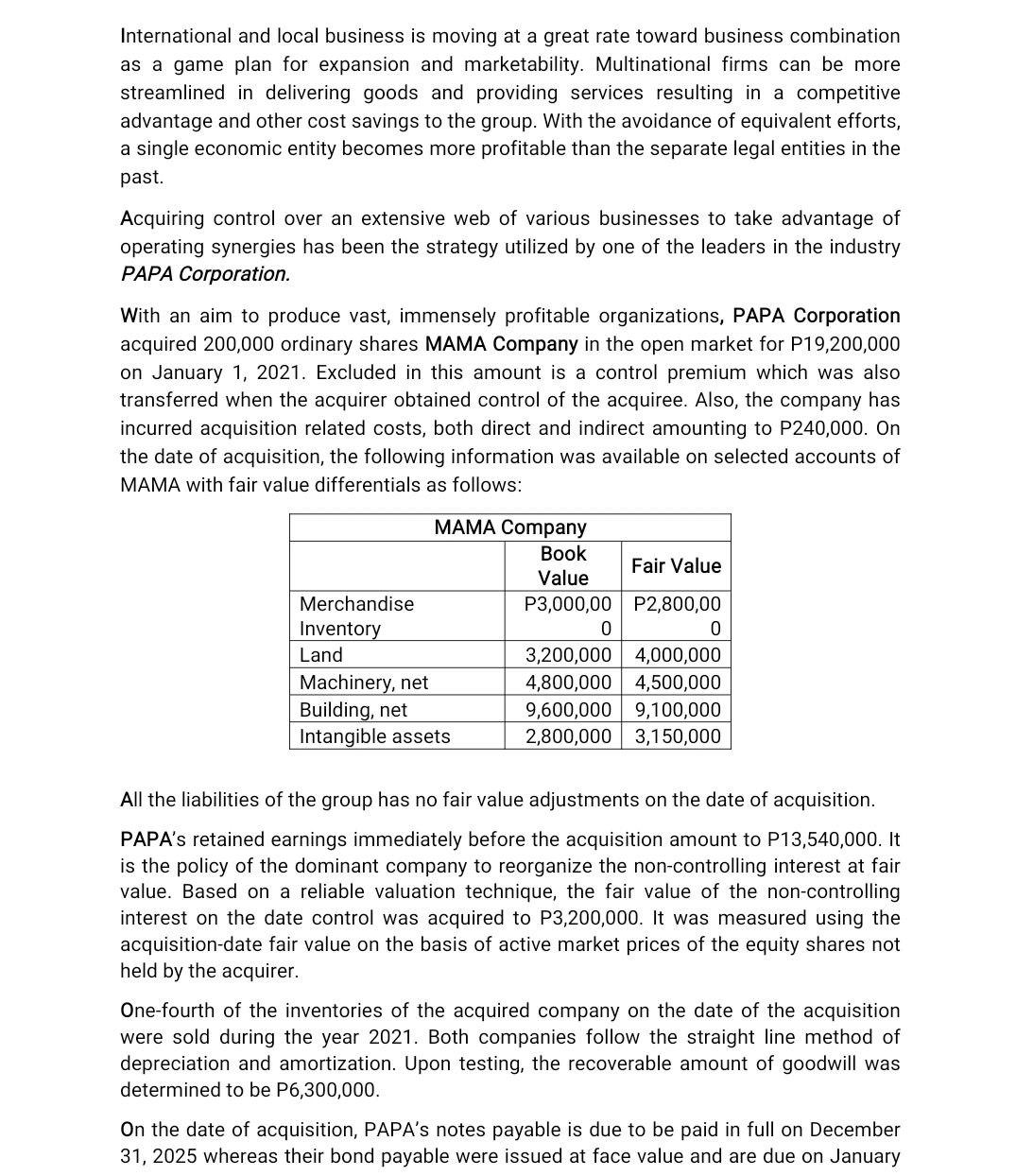

International and local business is moving at a great rate toward business combination as a game...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

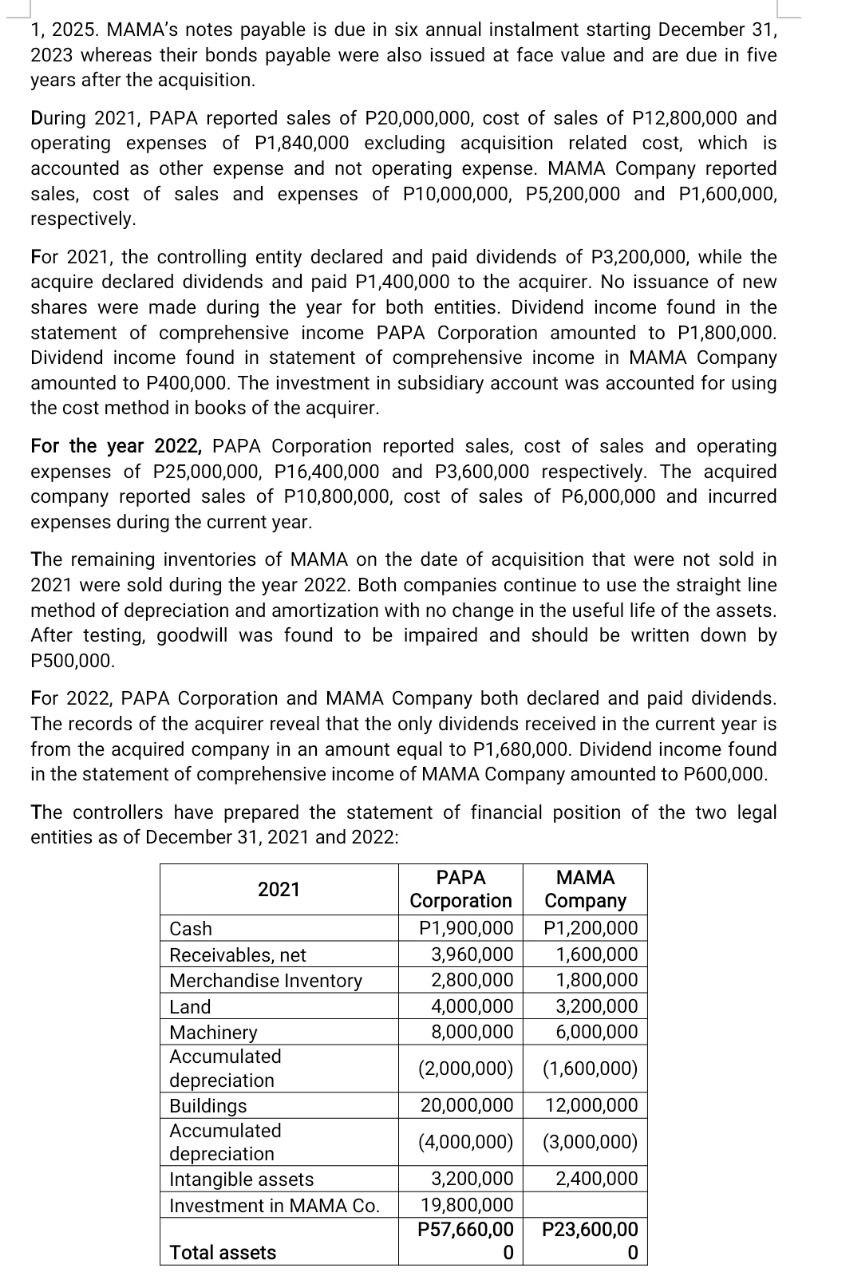

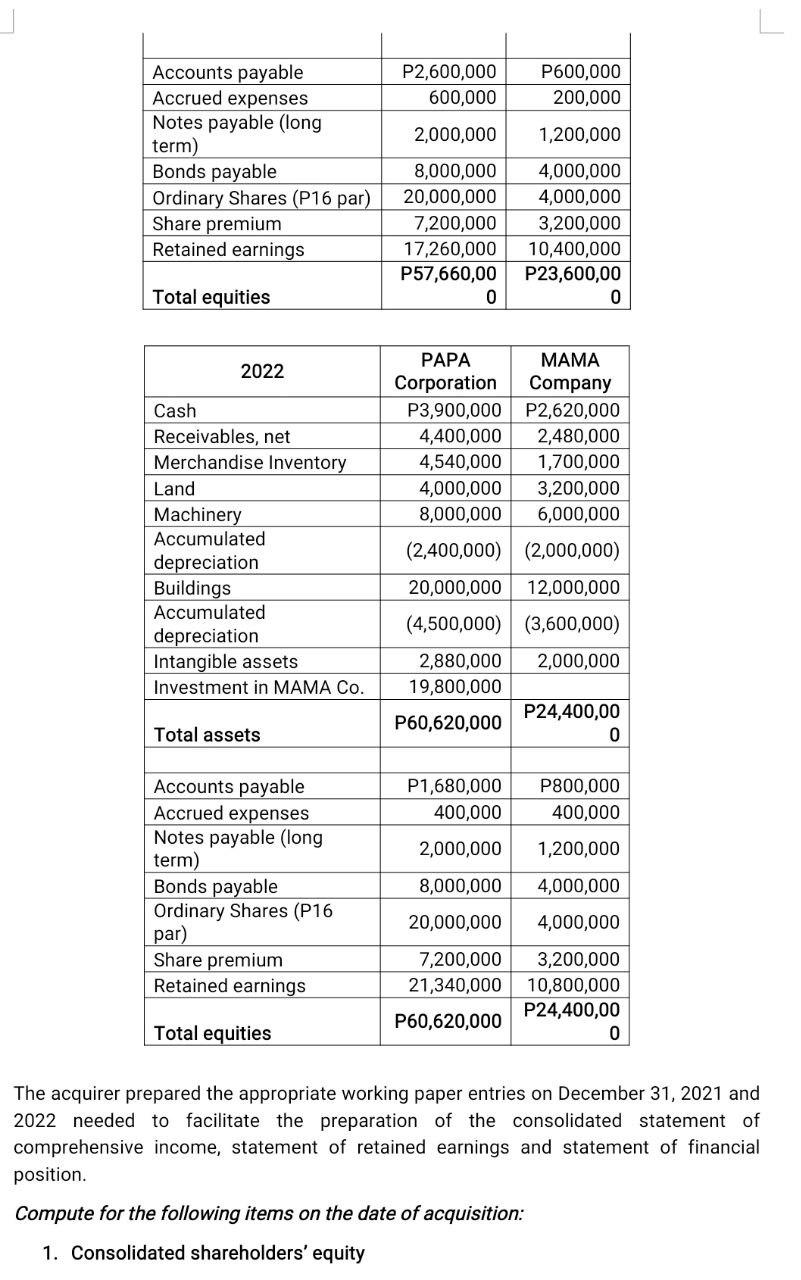

International and local business is moving at a great rate toward business combination as a game plan for expansion and marketability. Multinational firms can be more streamlined in delivering goods and providing services resulting in a competitive advantage and other cost savings to the group. With the avoidance of equivalent efforts, a single economic entity becomes more profitable than the separate legal entities in the past. Acquiring control over an extensive web of various businesses to take advantage of operating synergies has been the strategy utilized by one of the leaders in the industry PAPA Corporation. With an aim to produce vast, immensely profitable organizations, PAPA Corporation acquired 200,000 ordinary shares MAMA Company in the open market for P19,200,000 on January 1, 2021. Excluded in this amount is a control premium which was also transferred when the acquirer obtained control of the acquiree. Also, the company has incurred acquisition related costs, both direct and indirect amounting to P240,000. On the date of acquisition, the following information was available on selected accounts of MAMA with fair value differentials as follows: Merchandise Inventory Land MAMA Company Book Value P3,000,00 Machinery, net Building, net Intangible assets 0 Fair Value P2,800,00 0 3,200,000 4,000,000 4,800,000 4,500,000 9,600,000 9,100,000 2,800,000 3,150,000 All the liabilities of the group has no fair value adjustments on the date of acquisition. PAPA's retained earnings immediately before the acquisition amount to P13,540,000. It is the policy of the dominant company to reorganize the non-controlling interest at fair value. Based on a reliable valuation technique, the fair value of the non-controlling interest on the date control was acquired to P3,200,000. It was measured using the acquisition-date fair value on the basis of active market prices of the equity shares not held by the acquirer. One-fourth of the inventories of the acquired company on the date of the acquisition were sold during the year 2021. Both companies follow the straight line method of depreciation and amortization. Upon testing, the recoverable amount of goodwill was determined to be P6,300,000. On the date of acquisition, PAPA's notes payable is due to be paid in full on December 31, 2025 whereas their bond payable were issued at face value and are due on January 1, 2025. MAMA's notes payable is due in six annual instalment starting December 31, 2023 whereas their bonds payable were also issued at face value and are due in five years after the acquisition. During 2021, PAPA reported sales of P20,000,000, cost of sales of P12,800,000 and operating expenses of P1,840,000 excluding acquisition related cost, which is accounted as other expense and not operating expense. MAMA Company reported sales, cost of sales and expenses of P10,000,000, P5,200,000 and P1,600,000, respectively. For 2021, the controlling entity declared and paid dividends of P3,200,000, while the acquire declared dividends and paid P1,400,000 to the acquirer. No issuance of new shares were made during the year for both entities. Dividend income found in the statement of comprehensive income PAPA Corporation amounted to P1,800,000. Dividend income found in statement of comprehensive income in MAMA Company amounted to P400,000. The investment in subsidiary account was accounted for using the cost method in books of the acquirer. For the year 2022, PAPA Corporation reported sales, cost of sales and operating expenses of P25,000,000, P16,400,000 and P3,600,000 respectively. The acquired company reported sales of P10,800,000, cost of sales of P6,000,000 and incurred expenses during the current year. The remaining inventories of MAMA on the date of acquisition that were not sold in 2021 were sold during the year 2022. Both companies continue to use the straight line method of depreciation and amortization with no change in the useful life of the assets. After testing, goodwill was found to be impaired and should be written down by P500,000. For 2022, PAPA Corporation and MAMA Company both declared and paid dividends. The records of the acquirer reveal that the only dividends received in the current year is from the acquired company in an amount equal to P1,680,000. Dividend income found in the statement of comprehensive income of MAMA Company amounted to P600,000. The controllers have prepared the statement of financial position of the two legal entities as of December 31, 2021 and 2022: 2021 Cash Receivables, net Merchandise Inventory Land Machinery Accumulated depreciation Buildings Accumulated depreciation Intangible assets Investment in MAMA Co. Total assets PAPA Corporation MAMA Company P1,900,000 P1,200,000 3,960,000 1,600,000 2,800,000 1,800,000 4,000,000 3,200,000 8,000,000 6,000,000 (2,000,000) (1,600,000) 20,000,000 12,000,000 (4,000,000) (3,000,000) 3,200,000 2,400,000 19,800,000 P57,660,00 0 P23,600,00 0 Accounts payable Accrued expenses Notes payable (long term) Bonds payable Ordinary Shares (P16 par) Share premium Retained earnings Total equities 2022 Cash Receivables, net Merchandise Inventory Land Machinery Accumulated depreciation Buildings Accumulated depreciation Intangible assets Investment in MAMA Co. Total assets Accounts payable Accrued expenses Notes payable (long. term) Bonds payable Ordinary Shares (P16 par) Share premium Retained earnings Total equities P2,600,000 P600,000 600,000 200,000 2,000,000 1,200,000 8,000,000 4,000,000 20,000,000 4,000,000 3,200,000 10,400,000 P23,600,00 7,200,000 17,260,000 P57,660,00 0 0 PAPA Corporation MAMA Company P3,900,000 P2,620,000 4,400,000 2,480,000 4,540,000 1,700,000 4,000,000 3,200,000 8,000,000 6,000,000 (2,400,000) (2,000,000) 20,000,000 12,000,000 (4,500,000) (3,600,000) 2,880,000 2,000,000 19,800,000 P60,620,000 P24,400,00 0 P1,680,000 P800,000 400,000 400,000 2,000,000 1,200,000 8,000,000 4,000,000 20,000,000 4,000,000 7,200,000 3,200,000 21,340,000 10,800,000 P24,400,00 P60,620,000 0 The acquirer prepared the appropriate working paper entries on December 31, 2021 and 2022 needed to facilitate the preparation of the consolidated statement of comprehensive income, statement of retained earnings and statement of financial position. Compute for the following items on the date of acquisition: 1. Consolidated shareholders' equity 2. Goodwill in Statement of Financial Position of PAPA Corporation as a separate legal entity 3. Investment in MAMA Company in the Statement of Financial Position of the group Compute for the following items in the Consolidated Financial Statements as of (for the year) Decemebr 31, 2021: 4. Cost of sales 5. Gross profit 6. Dividend revenue 7. Operating expenses 8. Net income attributable 9. Non-controlling interest in net income 10. Current assets 11. Property, plant and equipment, net 12. Noncurrent liabilities. 13. Current liabilities 14. Noncurrent liabilities 15. Dividends declared 16. Retained earnings 17. Shareholders' equity 18. Non-controlling interest in net assets. Compute for the following items in the Consolidated Financial Statements as of (for the year) December 31, 2022: 19. Sales 20. Cost of sales 21. Operating expenses 22. Net income 23. Non-controlling interest in net income 24. Current assets 25. Property, plant and equipment, net 26. Noncurrent liabilities 27.Dividends declared 28. Retained earnings 29. Shareholders' equity 30. Non-controlling interest in net assets 31. Goodwill In the preparation of the Working Paper Entries, compute the following: (indicate whether debit or credit) 32. The amount of Investment in MAMA Company account (debited/credited) in eliminating the shareholders' equity of the acquired company. 41 Page 33. The amount of Non-controlling Interest account (debited/credited) in recognizing the acquisition date fair value differentials in the identifiable assets of the acquired company. (net debit/net credit) 34. The total amount (debited/credited) to Merchandise Inventory account in amortizing its fair value differential in the 2022 working paper. and 35. The amount (debited/credited) to Retained Earnings account on December 31, 2021 regarding the impairment of goodwill. 36. The amount of Non-controlling Interest account (debited/credited) in eliminating the intercompany dividends on the second year. 37. The amount (debited/credited) to Operating expense account in amortizing the fair value differential of intangible asset in 2022. 38. The amount (debited/credited) to Cost of Goods Sold account in amortizing the fair value differential of an asset of the acquiree on first year. 39. The amount (debited/credited) to Operating Expense account in amortizing the fair value differential of the property, plant and equipment in 2022. 40. The amount (debited/credited) to Retained Earnings account on December 31, 2022 to assign to the non-controlling shareholders their share of the increase in the acquired company's adjusted and undistributed earnings that occurred between the acquisition date and the beginning of the current period. International and local business is moving at a great rate toward business combination as a game plan for expansion and marketability. Multinational firms can be more streamlined in delivering goods and providing services resulting in a competitive advantage and other cost savings to the group. With the avoidance of equivalent efforts, a single economic entity becomes more profitable than the separate legal entities in the past. Acquiring control over an extensive web of various businesses to take advantage of operating synergies has been the strategy utilized by one of the leaders in the industry PAPA Corporation. With an aim to produce vast, immensely profitable organizations, PAPA Corporation acquired 200,000 ordinary shares MAMA Company in the open market for P19,200,000 on January 1, 2021. Excluded in this amount is a control premium which was also transferred when the acquirer obtained control of the acquiree. Also, the company has incurred acquisition related costs, both direct and indirect amounting to P240,000. On the date of acquisition, the following information was available on selected accounts of MAMA with fair value differentials as follows: Merchandise Inventory Land MAMA Company Book Value P3,000,00 Machinery, net Building, net Intangible assets 0 Fair Value P2,800,00 0 3,200,000 4,000,000 4,800,000 4,500,000 9,600,000 9,100,000 2,800,000 3,150,000 All the liabilities of the group has no fair value adjustments on the date of acquisition. PAPA's retained earnings immediately before the acquisition amount to P13,540,000. It is the policy of the dominant company to reorganize the non-controlling interest at fair value. Based on a reliable valuation technique, the fair value of the non-controlling interest on the date control was acquired to P3,200,000. It was measured using the acquisition-date fair value on the basis of active market prices of the equity shares not held by the acquirer. One-fourth of the inventories of the acquired company on the date of the acquisition were sold during the year 2021. Both companies follow the straight line method of depreciation and amortization. Upon testing, the recoverable amount of goodwill was determined to be P6,300,000. On the date of acquisition, PAPA's notes payable is due to be paid in full on December 31, 2025 whereas their bond payable were issued at face value and are due on January 1, 2025. MAMA's notes payable is due in six annual instalment starting December 31, 2023 whereas their bonds payable were also issued at face value and are due in five years after the acquisition. During 2021, PAPA reported sales of P20,000,000, cost of sales of P12,800,000 and operating expenses of P1,840,000 excluding acquisition related cost, which is accounted as other expense and not operating expense. MAMA Company reported sales, cost of sales and expenses of P10,000,000, P5,200,000 and P1,600,000, respectively. For 2021, the controlling entity declared and paid dividends of P3,200,000, while the acquire declared dividends and paid P1,400,000 to the acquirer. No issuance of new shares were made during the year for both entities. Dividend income found in the statement of comprehensive income PAPA Corporation amounted to P1,800,000. Dividend income found in statement of comprehensive income in MAMA Company amounted to P400,000. The investment in subsidiary account was accounted for using the cost method in books of the acquirer. For the year 2022, PAPA Corporation reported sales, cost of sales and operating expenses of P25,000,000, P16,400,000 and P3,600,000 respectively. The acquired company reported sales of P10,800,000, cost of sales of P6,000,000 and incurred expenses during the current year. The remaining inventories of MAMA on the date of acquisition that were not sold in 2021 were sold during the year 2022. Both companies continue to use the straight line method of depreciation and amortization with no change in the useful life of the assets. After testing, goodwill was found to be impaired and should be written down by P500,000. For 2022, PAPA Corporation and MAMA Company both declared and paid dividends. The records of the acquirer reveal that the only dividends received in the current year is from the acquired company in an amount equal to P1,680,000. Dividend income found in the statement of comprehensive income of MAMA Company amounted to P600,000. The controllers have prepared the statement of financial position of the two legal entities as of December 31, 2021 and 2022: 2021 Cash Receivables, net Merchandise Inventory Land Machinery Accumulated depreciation Buildings Accumulated depreciation Intangible assets Investment in MAMA Co. Total assets PAPA Corporation MAMA Company P1,900,000 P1,200,000 3,960,000 1,600,000 2,800,000 1,800,000 4,000,000 3,200,000 8,000,000 6,000,000 (2,000,000) (1,600,000) 20,000,000 12,000,000 (4,000,000) (3,000,000) 3,200,000 2,400,000 19,800,000 P57,660,00 0 P23,600,00 0 Accounts payable Accrued expenses Notes payable (long term) Bonds payable Ordinary Shares (P16 par) Share premium Retained earnings Total equities 2022 Cash Receivables, net Merchandise Inventory Land Machinery Accumulated depreciation Buildings Accumulated depreciation Intangible assets Investment in MAMA Co. Total assets Accounts payable Accrued expenses Notes payable (long. term) Bonds payable Ordinary Shares (P16 par) Share premium Retained earnings Total equities P2,600,000 P600,000 600,000 200,000 2,000,000 1,200,000 8,000,000 4,000,000 20,000,000 4,000,000 3,200,000 10,400,000 P23,600,00 7,200,000 17,260,000 P57,660,00 0 0 PAPA Corporation MAMA Company P3,900,000 P2,620,000 4,400,000 2,480,000 4,540,000 1,700,000 4,000,000 3,200,000 8,000,000 6,000,000 (2,400,000) (2,000,000) 20,000,000 12,000,000 (4,500,000) (3,600,000) 2,880,000 2,000,000 19,800,000 P60,620,000 P24,400,00 0 P1,680,000 P800,000 400,000 400,000 2,000,000 1,200,000 8,000,000 4,000,000 20,000,000 4,000,000 7,200,000 3,200,000 21,340,000 10,800,000 P24,400,00 P60,620,000 0 The acquirer prepared the appropriate working paper entries on December 31, 2021 and 2022 needed to facilitate the preparation of the consolidated statement of comprehensive income, statement of retained earnings and statement of financial position. Compute for the following items on the date of acquisition: 1. Consolidated shareholders' equity 2. Goodwill in Statement of Financial Position of PAPA Corporation as a separate legal entity 3. Investment in MAMA Company in the Statement of Financial Position of the group Compute for the following items in the Consolidated Financial Statements as of (for the year) Decemebr 31, 2021: 4. Cost of sales 5. Gross profit 6. Dividend revenue 7. Operating expenses 8. Net income attributable 9. Non-controlling interest in net income 10. Current assets 11. Property, plant and equipment, net 12. Noncurrent liabilities. 13. Current liabilities 14. Noncurrent liabilities 15. Dividends declared 16. Retained earnings 17. Shareholders' equity 18. Non-controlling interest in net assets. Compute for the following items in the Consolidated Financial Statements as of (for the year) December 31, 2022: 19. Sales 20. Cost of sales 21. Operating expenses 22. Net income 23. Non-controlling interest in net income 24. Current assets 25. Property, plant and equipment, net 26. Noncurrent liabilities 27.Dividends declared 28. Retained earnings 29. Shareholders' equity 30. Non-controlling interest in net assets 31. Goodwill In the preparation of the Working Paper Entries, compute the following: (indicate whether debit or credit) 32. The amount of Investment in MAMA Company account (debited/credited) in eliminating the shareholders' equity of the acquired company. 41 Page 33. The amount of Non-controlling Interest account (debited/credited) in recognizing the acquisition date fair value differentials in the identifiable assets of the acquired company. (net debit/net credit) 34. The total amount (debited/credited) to Merchandise Inventory account in amortizing its fair value differential in the 2022 working paper. and 35. The amount (debited/credited) to Retained Earnings account on December 31, 2021 regarding the impairment of goodwill. 36. The amount of Non-controlling Interest account (debited/credited) in eliminating the intercompany dividends on the second year. 37. The amount (debited/credited) to Operating expense account in amortizing the fair value differential of intangible asset in 2022. 38. The amount (debited/credited) to Cost of Goods Sold account in amortizing the fair value differential of an asset of the acquiree on first year. 39. The amount (debited/credited) to Operating Expense account in amortizing the fair value differential of the property, plant and equipment in 2022. 40. The amount (debited/credited) to Retained Earnings account on December 31, 2022 to assign to the non-controlling shareholders their share of the increase in the acquired company's adjusted and undistributed earnings that occurred between the acquisition date and the beginning of the current period.

Expert Answer:

Answer rating: 100% (QA)

SOLUTION 1 Goodwill in Statement of Financial Position of PAPA Corporation as a separate legal entity as of December 31 2021 is P6300000 2 Investment in MAMA Company in the Statement of Financial Posi... View the full answer

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date:

Students also viewed these accounting questions

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Kennedy Company reported the following amounts for the year 2020. Required: Prepare the Cost of Goods Manufactured Schedule for Kennedy Company. Direct materials used $30,000 Finished goods...

-

Determine the normal force, shear force, and moment in the curved rod as a function of ?.

-

You are a consultant to the marketing department of a business preparing to launch an ad campaign for a new product. The company can afford to run ads during one TV show, and has decided not to...

-

Birds have hollow bones, an adaptation for flight. How do hollow bones help birds fly?

-

Dillip Corp., a wholesaler of office equipment, issued $45,000,000 of 10-year, 10% callable bonds on March 1, 2012, with interest payable on March 1 and September 1. The fiscal year of the company is...

-

1. If you have the following binary image and structure element, find the outer and inner object boundary (show the steps). 0 0 0 0 0 0 0 0 0 0 0 0 0 0 011110 0 0 0 0 1 1 1 10 0 0 0 1 1 1 1 0 0 0 0 0...

-

Pam Corporation purchased 75 percent of the outstanding voting stock of Sun Corporation for $4,800,000 on January 1, 2016. Sun's stockholders' equity on this date consisted of the following (in...

-

Many organizations require that a prospective employee allow access to social media by company representatives to follow. Some companies will be upfront and let the potential new hire know that it is...

-

Sedki earned $180,480 in 2017. How much did he pay in Social Security taxes? In Medicare taxes? In total FICA taxes? (Hint: Don't forget the annual Social Security earnings cap.) The amount Sedki...

-

Suppose people with 15 years of schooling average earnings of $60,000 while people with 16 years of education average $66,000. Suppose the skills acquired in school depreciate over time, perhaps...

-

Provide complete solution. A +15 microC charge is located 40 cm from a +3.0 microC charge. The magnitude of the electrostatic force on the larger charge and on the smaller charge (in N) is,...

-

Implement a priority queue capable of holding objects of an arbitrary type T. Implement the queue using ArrayList as an underlying data structure. A priority queue is a type of list where every item...

-

Suppose a parabola has the x-intercept s (-7,0) and (-2,0). a. Write the quadratic function as a product of two factors. b. Multiply the factors to write the quadratic function in y=ax^(2)+bx+c form.

-

The next question deals with the December 31, 2019 Balance Sheet of Horan Industries. Horan Industries began 2019 with $30,000 in inventory. In 2019, its inventory purchases amounted to $50,000, and...

-

1. Which of the four major types of information systems do you think is the most valuable to an organization? 2. How do you critically associate the ideas of business agility and business efficiency...

-

The articles of partnership of the firm of Wilson and Company provide the following: William Smith to contribute $50,000; to receive interest thereon at 13 percent per annum and to devote such time...

-

Civil Code 1719, subdivision (a) provides in part that any person who draws a check that is dishonored due to insufficient funds shall be liable to the payee for the amount owing upon the check and...

-

List and explain the constitutional amendments affecting criminal procedure.

-

An ideal classical gas composed of \(N\) particles, each of mass \(m\), is enclosed in a vertical cylinder of height \(L\) placed in a uniform gravitational field (of acceleration \(g\) ) and is in...

-

Show that the quantum-mechanical partition function of a system of \(N\) interacting particles approaches the classical form \[Q_{N}(V, T)=\frac{1}{N ! h^{3 N}} \int e^{-\beta E(\boldsymbol{q},...

-

Show that the entropy of an ideal gas in thermal equilibrium is given by the formula \[ S=k \sum_{\varepsilon}\left[\left\langle n_{\varepsilon}+1ightangle \ln \left\langle...

Study smarter with the SolutionInn App