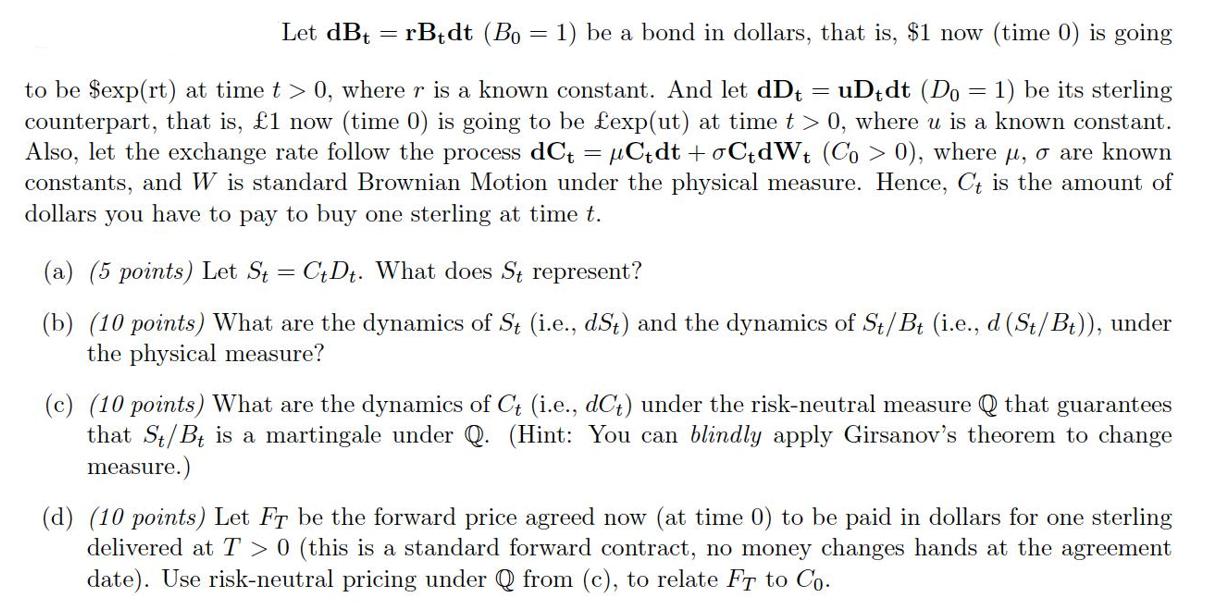

Let dBtrBedt (Bo = 1) be a bond in dollars, that is, $1 now (time 0)...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Probability And Statistics

ISBN: 9780321500465

4th Edition

Authors: Morris H. DeGroot, Mark J. Schervish

Posted Date: