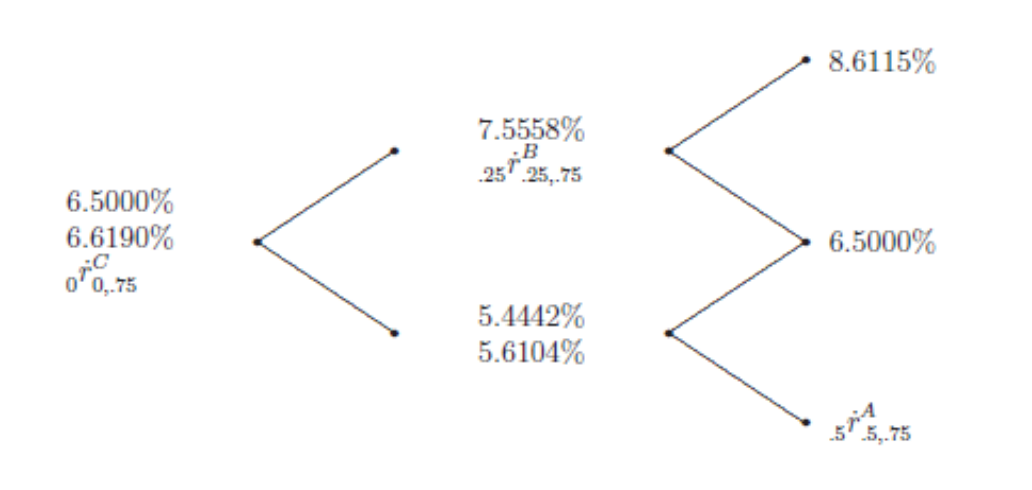

Let T be the total amount of time to be modeled with the tree, and h be

Question:

Let T be the total amount of time to be modeled with the tree, and h be the length

of time between each time period on the tree. Assuming the following parameter

values: 0r0,.25 = 6.5%, h = .25, T = .5, ? = 8.0%, ? = 2.5%, ? = .70, and ? = 0.20,

the following tree emerges.

(graph)

At each node the first number is the yield on a zero coupon bond with a 3 month

maturity; the second number (when present) is the yield on a zero coupon bond

with a 6 month maturity; and the third number (when present) is the yield on a

zero coupon bond with a 9 month maturity. For example, 0r0,.75 is the yield of a 9

month zero coupon bond, i.e. covering time 0 to .75 years from now, observed

today. All the yields are annualized with continuous compounding. Can you find

the three missing values?

Aside: Inferring yields of long-term bonds from a tree is an important exercise, in

particular if investors require a risk premium. A step-by-step description about

how to solve for the term structure given such a tree can also be found in the

technical notes, pages 703 - 715.

Expert Answer:

Data Analysis and Decision Making

ISBN: 978-0538476126

4th edition

Authors: Christian Albright, Wayne Winston, Christopher Zappe