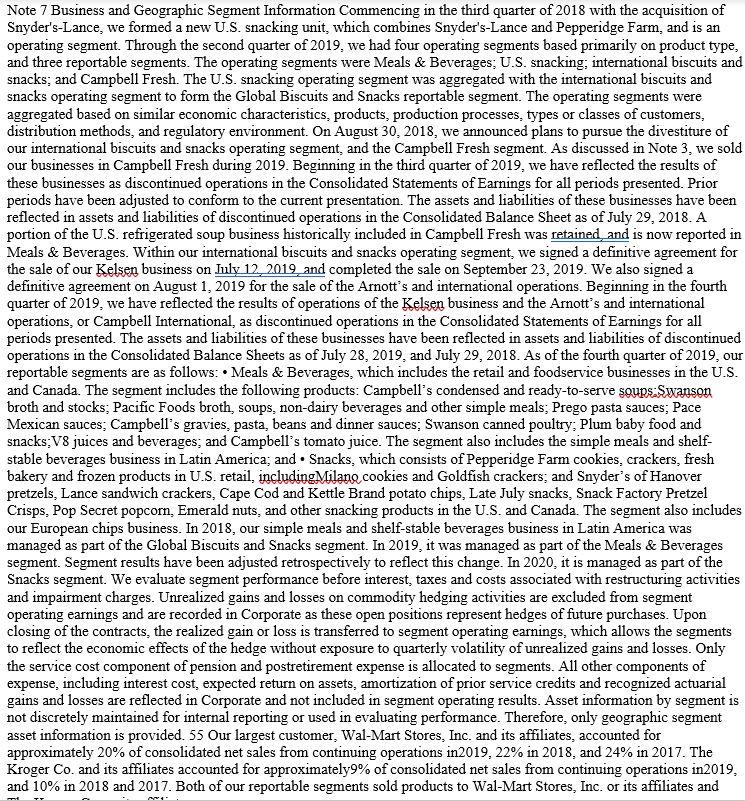

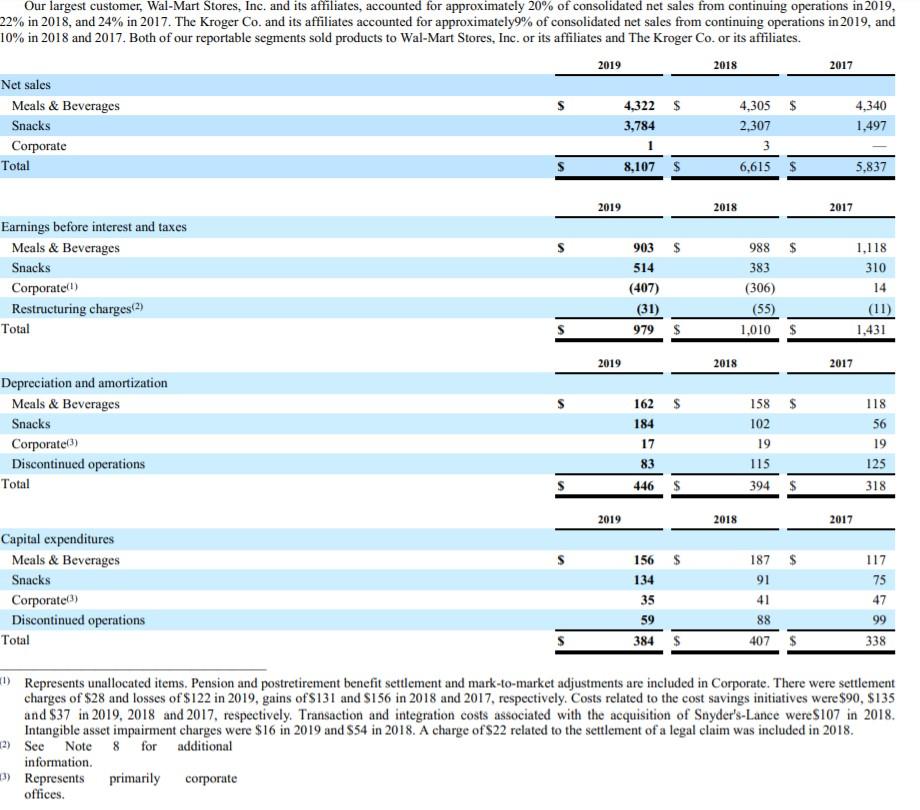

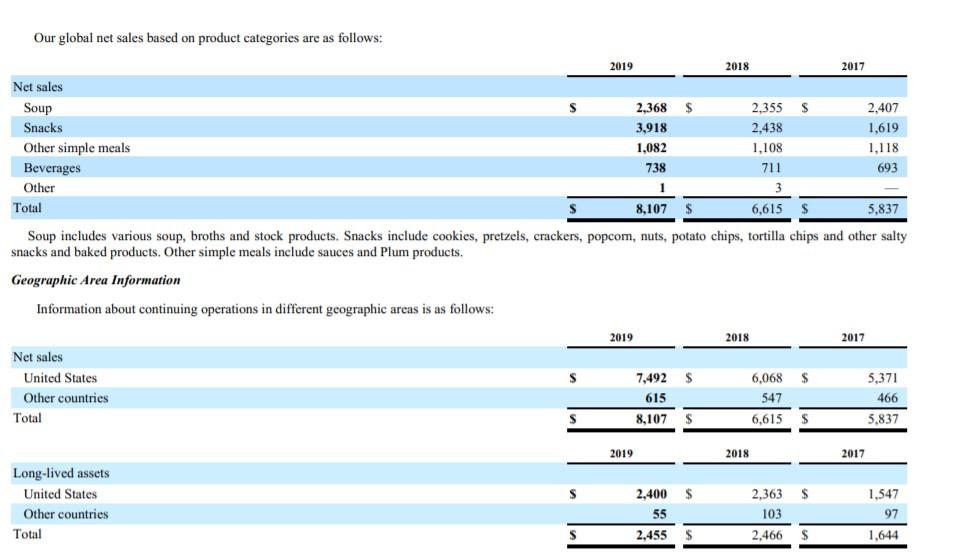

1. List the Reportable Segments for Campbell Soup Company. The reportable segments are developed using the management...

Question:

1. List the Reportable Segments for Campbell Soup Company. The reportable segments are developed using the management approach. A company reports segments based on how the company is managed. If your company has more than one reportable segment, are the segments product-based or geography-based?

2. What is the name of the Independent Auditor that audited the financial statements and produced the Report on Internal Control over Financial Reporting? Why is an independent audit critical to confidence in financial reporting?

3. Accounts Receivable:

- What is the total amount of outstanding Accounts Receivable at the end of the most recent year?

- How much of this does the company not expect to collect?

- What is the percent of projected uncollectible accounts to Accounts Receivable?

- How do the Balance Sheet and Income Statement change when a credit is ultimately written off?

4. Property, Plant, and Equipment:

Property, Plant and Equipment — Property, plant and equipment are recorded at historical cost and are depreciated over estimated useful lives using the straight-line method. Buildings and machinery and equipment are depreciated over periods not exceeding 45 years and 20 years, respectively. Assets are evaluated for impairment when conditions indicate that the carrying value may not be recoverable. Such conditions include significant adverse changes in business climate or a plan of disposal. Repairs and maintenance are charged to expense as incurred.

- What is the Gross PPE for the company, and what does it represent?

- Calculate the percent depreciated for the company’s Property and Equipment.

- Why is this percent depreciated of interest to financial statement readers?

5. Inventory:

- What is the inventory costing method used by the company?

- If there is a Lifo reserve, state how much it is and what it means for the company’s inventory cost.

- How much of the inventory consists of finished products?

6. Income Tax

- What is the effective tax rate for your company?

- What amount of tax is payable based on the tax return?

We also recorded impairment charges on goodwill and intangible assets included in Noncurrent assets of discontinued operations. See Note 3 for additional information. The estimates of future cash flows used in determining the fair value of goodwill and intangible assets involve significant management judgment and are based upon assumptions about expected future operating performance, economic conditions, market conditions and cost of capital. Inherent in estimating the future cash flows are uncertainties beyond our control, such as changes in capital markets. The actual cash flows could differ materially from management’s estimates due to changes in business conditions, operating performance and economic conditions.

7. Goodwill and Intangible Assets:

- How much does the company report in Intangible Assets and Goodwill?

- What percent of total assets do they each comprise?

- Except for Discontinued Operations, were any of these deemed impaired last year? If so, how much was the total loss?

- Were there impairment charges included in the loss from discontinued operations? If so, how much was the impairment loss?

- Note 4 from 10k Did the company have an acquisition last year? If so, what was the amount of Goodwill generated? If there is more than one acquisition, just pick one.

8. Pension and Post-employment benefits:note 11 pg 60-66

- What is the funded status of the pension plan (over/under and by how much)?

- How do actual returns on plan assets affect the funding status of the plan?

- How much did the company contribute to its pension plan in the most recent year?

- Why are defined benefit pension liabilities included in a chapter about off-balance sheet liabilities?

Expert Answer:

1 Campbell Soup Company has four reportable segments US Simple Meals US Beverages International Simple Meals and International Beverages The segments are productbased as they are organized around the ... View the full answer

Financial Accounting: A Business Process Approach

ISBN: 978-0136115274

3rd edition

Authors: Jane L. Reimers