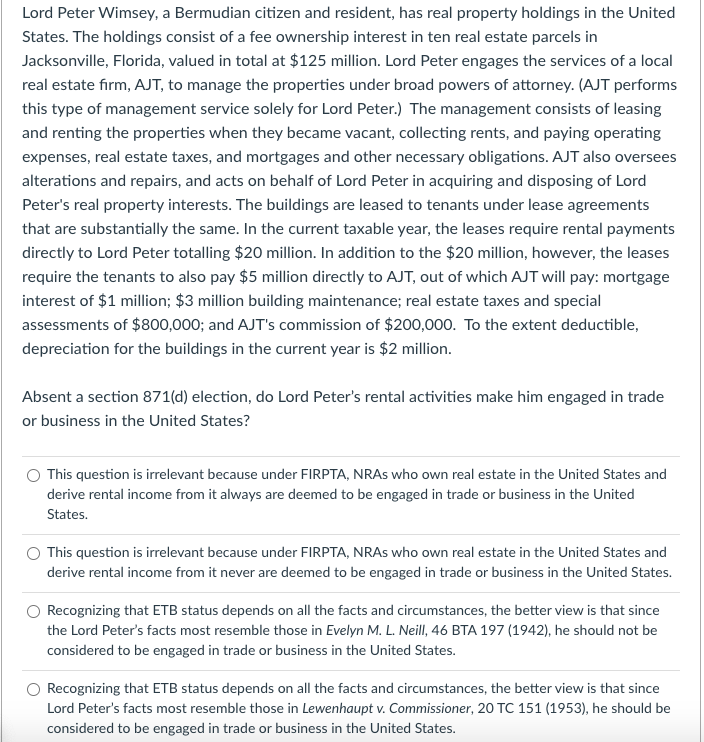

Lord Peter Wimsey, a Bermudian citizen and resident, has real property holdings in the United States....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

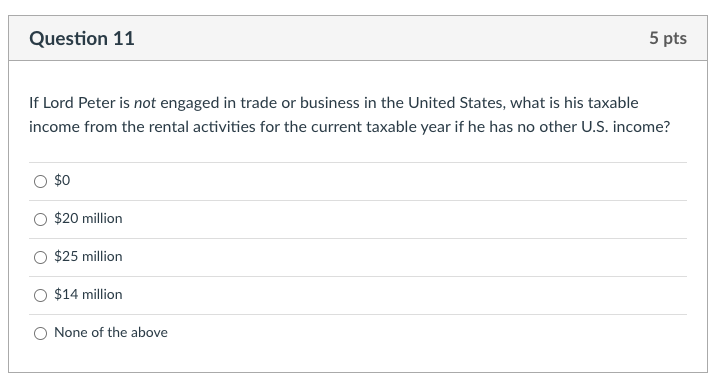

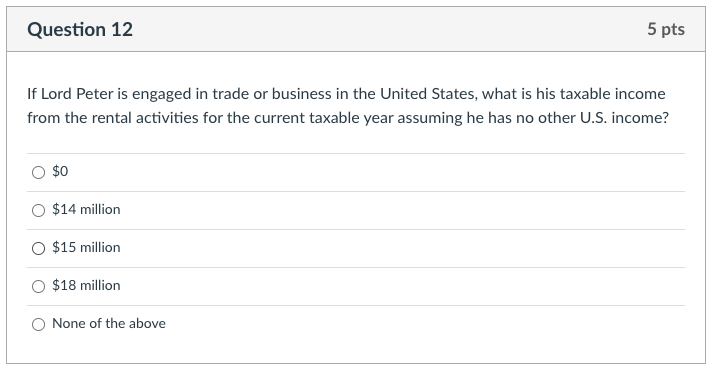

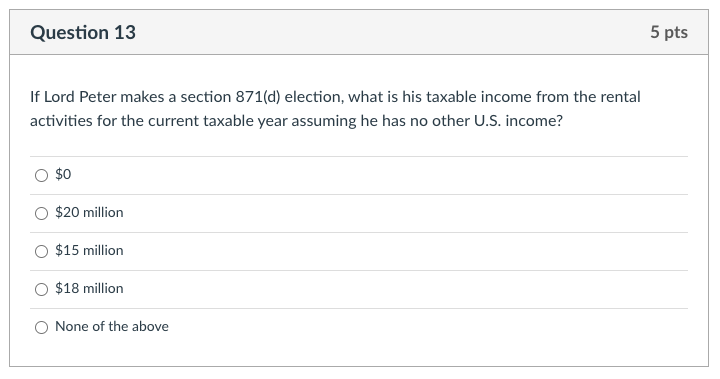

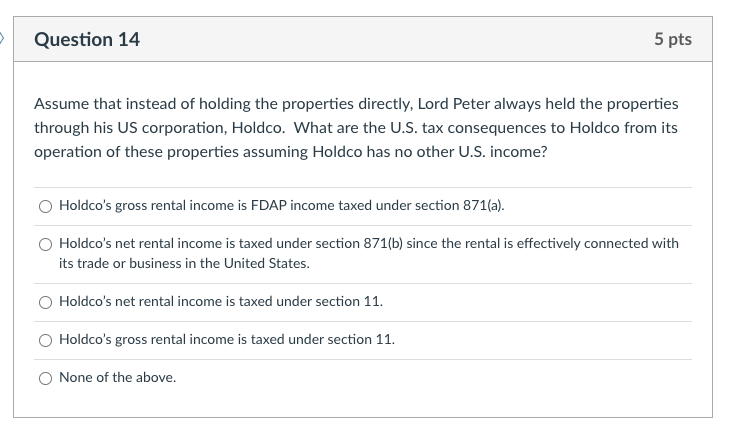

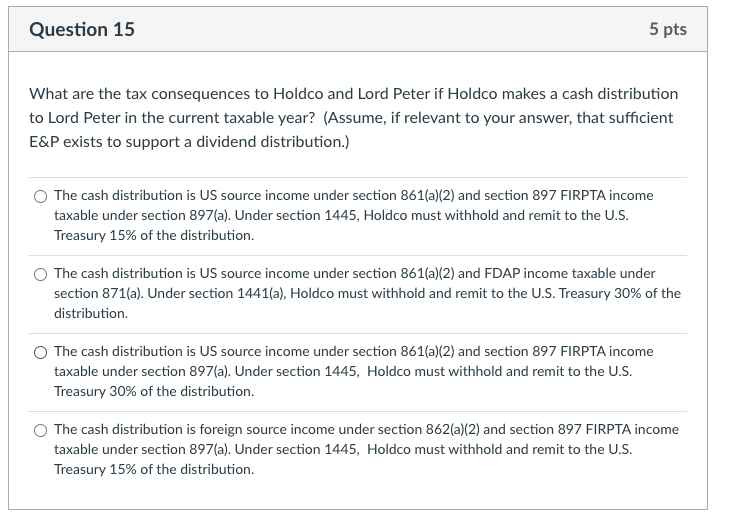

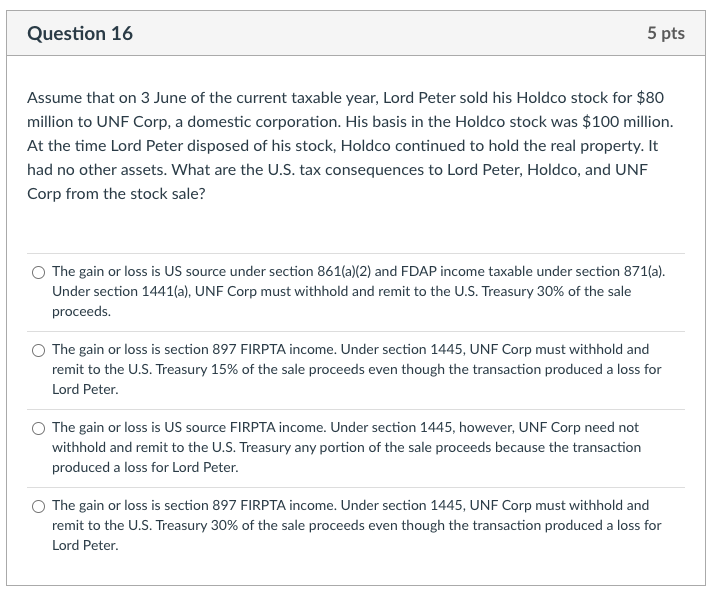

Lord Peter Wimsey, a Bermudian citizen and resident, has real property holdings in the United States. The holdings consist of a fee ownership interest in ten real estate parcels in Jacksonville, Florida, valued in total at $125 million. Lord Peter engages the services of a local real estate firm, AJT, to manage the properties under broad powers of attorney. (AJT performs this type of management service solely for Lord Peter.) The management consists of leasing and renting the properties when they became vacant, collecting rents, and paying operating expenses, real estate taxes, and mortgages and other necessary obligations. AJT also oversees alterations and repairs, and acts on behalf of Lord Peter in acquiring and disposing of Lord Peter's real property interests. The buildings are leased to tenants under lease agreements that are substantially the same. In the current taxable year, the leases require rental payments directly to Lord Peter totalling $20 million. In addition to the $20 million, however, the leases require the tenants to also pay $5 million directly to AJT, out of which AJT will pay: mortgage interest of $1 million; $3 million building maintenance; real estate taxes and special assessments of $800,000; and AJT's commission of $200,000. To the extent deductible, depreciation for the buildings in the current year is $2 million. Absent a section 871(d) election, do Lord Peter's rental activities make him engaged in trade or business in the United States? This question is irrelevant because under FIRPTA, NRAs who own real estate in the United States and derive rental income from it always are deemed to be engaged in trade or business in the United States. This question is irrelevant because under FIRPTA, NRAs who own real estate in the United States and derive rental income from it never are deemed to be engaged in trade or business in the United States. Recognizing that ETB status depends on all the facts and circumstances, the better view is that since the Lord Peter's facts most resemble those in Evelyn M. L. Neill, 46 BTA 197 (1942), he should not be considered to be engaged in trade or business in the United States. Recognizing that ETB status depends on all the facts and circumstances, the better view is that since Lord Peter's facts most resemble those in Lewenhaupt v. Commissioner, 20 TC 151 (1953), he should be considered to be engaged in trade or business in the United States. Question 11 If Lord Peter is not engaged in trade or business in the United States, what is his taxable income from the rental activities for the current taxable year if he has no other U.S. income? $0 $20 million $25 million $14 million 5 pts None of the above Question 12 If Lord Peter is engaged in trade or business in the United States, what is his taxable income from the rental activities for the current taxable year assuming he has no other U.S. income? $0 $14 million O $15 million $18 million 5 pts O None of the above Question 13 If Lord Peter makes a section 871(d) election, what is his taxable income from the rental activities for the current taxable year assuming he has no other U.S. income? $0 $20 million $15 million $18 million None of the above 5 pts 5 Question 14 Assume that instead of holding the properties directly, Lord Peter always held the properties through his US corporation, Holdco. What are the U.S. tax consequences to Holdco from its operation of these properties assuming Holdco has no other U.S. income? O Holdco's gross rental income is FDAP income taxed under section 871(a). O Holdco's net rental income is taxed under section 871(b) since the rental is effectively connected with its trade or business in the United States. Holdco's net rental income is taxed under section 11. 5 pts O Holdco's gross rental income is taxed under section 11. None of the above. Question 15 5 pts What are the tax consequences to Holdco and Lord Peter if Holdco makes a cash distribution to Lord Peter in the current taxable year? (Assume, if relevant to your answer, that sufficient E&P exists to support a dividend distribution.) The cash distribution is US source income under section 861(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 15% of the distribution. The cash distribution is US source income under section 861(a)(2) and FDAP income taxable under section 871(a). Under section 1441(a), Holdco must withhold and remit to the U.S. Treasury 30% of the distribution. The cash distribution is US source income under section 861(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 30% of the distribution. The cash distribution is foreign source income under section 862(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 15% of the distribution. Question 16 5 pts Assume that on 3 June of the current taxable year, Lord Peter sold his Holdco stock for $80 million to UNF Corp, a domestic corporation. His basis in the Holdco stock was $100 million. At the time Lord Peter disposed of his stock, Holdco continued to hold the real property. It had no other assets. What are the U.S. tax consequences to Lord Peter, Holdco, and UNF Corp from the stock sale? The gain or loss is US source under section 861(a)(2) and FDAP income taxable under section 871(a). Under section 1441(a), UNF Corp must withhold and remit to the U.S. Treasury 30% of the sale proceeds. The gain or loss is section 897 FIRPTA income. Under section 1445, UNF Corp must withhold and remit to the U.S. Treasury 15% of the sale proceeds even though the transaction produced a loss for Lord Peter. The gain or loss is US source FIRPTA income. Under section 1445, however, UNF Corp need not withhold and remit to the U.S. Treasury any portion of the sale proceeds because the transaction produced a loss for Lord Peter. The gain or loss is section 897 FIRPTA income. Under section 1445, UNF Corp must withhold and remit to the U.S. Treasury 30% of the sale proceeds even though the transaction produced a loss for Lord Peter. Lord Peter Wimsey, a Bermudian citizen and resident, has real property holdings in the United States. The holdings consist of a fee ownership interest in ten real estate parcels in Jacksonville, Florida, valued in total at $125 million. Lord Peter engages the services of a local real estate firm, AJT, to manage the properties under broad powers of attorney. (AJT performs this type of management service solely for Lord Peter.) The management consists of leasing and renting the properties when they became vacant, collecting rents, and paying operating expenses, real estate taxes, and mortgages and other necessary obligations. AJT also oversees alterations and repairs, and acts on behalf of Lord Peter in acquiring and disposing of Lord Peter's real property interests. The buildings are leased to tenants under lease agreements that are substantially the same. In the current taxable year, the leases require rental payments directly to Lord Peter totalling $20 million. In addition to the $20 million, however, the leases require the tenants to also pay $5 million directly to AJT, out of which AJT will pay: mortgage interest of $1 million; $3 million building maintenance; real estate taxes and special assessments of $800,000; and AJT's commission of $200,000. To the extent deductible, depreciation for the buildings in the current year is $2 million. Absent a section 871(d) election, do Lord Peter's rental activities make him engaged in trade or business in the United States? This question is irrelevant because under FIRPTA, NRAs who own real estate in the United States and derive rental income from it always are deemed to be engaged in trade or business in the United States. This question is irrelevant because under FIRPTA, NRAs who own real estate in the United States and derive rental income from it never are deemed to be engaged in trade or business in the United States. Recognizing that ETB status depends on all the facts and circumstances, the better view is that since the Lord Peter's facts most resemble those in Evelyn M. L. Neill, 46 BTA 197 (1942), he should not be considered to be engaged in trade or business in the United States. Recognizing that ETB status depends on all the facts and circumstances, the better view is that since Lord Peter's facts most resemble those in Lewenhaupt v. Commissioner, 20 TC 151 (1953), he should be considered to be engaged in trade or business in the United States. Question 11 If Lord Peter is not engaged in trade or business in the United States, what is his taxable income from the rental activities for the current taxable year if he has no other U.S. income? $0 $20 million $25 million $14 million 5 pts None of the above Question 12 If Lord Peter is engaged in trade or business in the United States, what is his taxable income from the rental activities for the current taxable year assuming he has no other U.S. income? $0 $14 million O $15 million $18 million 5 pts O None of the above Question 13 If Lord Peter makes a section 871(d) election, what is his taxable income from the rental activities for the current taxable year assuming he has no other U.S. income? $0 $20 million $15 million $18 million None of the above 5 pts 5 Question 14 Assume that instead of holding the properties directly, Lord Peter always held the properties through his US corporation, Holdco. What are the U.S. tax consequences to Holdco from its operation of these properties assuming Holdco has no other U.S. income? O Holdco's gross rental income is FDAP income taxed under section 871(a). O Holdco's net rental income is taxed under section 871(b) since the rental is effectively connected with its trade or business in the United States. Holdco's net rental income is taxed under section 11. 5 pts O Holdco's gross rental income is taxed under section 11. None of the above. Question 15 5 pts What are the tax consequences to Holdco and Lord Peter if Holdco makes a cash distribution to Lord Peter in the current taxable year? (Assume, if relevant to your answer, that sufficient E&P exists to support a dividend distribution.) The cash distribution is US source income under section 861(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 15% of the distribution. The cash distribution is US source income under section 861(a)(2) and FDAP income taxable under section 871(a). Under section 1441(a), Holdco must withhold and remit to the U.S. Treasury 30% of the distribution. The cash distribution is US source income under section 861(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 30% of the distribution. The cash distribution is foreign source income under section 862(a)(2) and section 897 FIRPTA income taxable under section 897(a). Under section 1445, Holdco must withhold and remit to the U.S. Treasury 15% of the distribution. Question 16 5 pts Assume that on 3 June of the current taxable year, Lord Peter sold his Holdco stock for $80 million to UNF Corp, a domestic corporation. His basis in the Holdco stock was $100 million. At the time Lord Peter disposed of his stock, Holdco continued to hold the real property. It had no other assets. What are the U.S. tax consequences to Lord Peter, Holdco, and UNF Corp from the stock sale? The gain or loss is US source under section 861(a)(2) and FDAP income taxable under section 871(a). Under section 1441(a), UNF Corp must withhold and remit to the U.S. Treasury 30% of the sale proceeds. The gain or loss is section 897 FIRPTA income. Under section 1445, UNF Corp must withhold and remit to the U.S. Treasury 15% of the sale proceeds even though the transaction produced a loss for Lord Peter. The gain or loss is US source FIRPTA income. Under section 1445, however, UNF Corp need not withhold and remit to the U.S. Treasury any portion of the sale proceeds because the transaction produced a loss for Lord Peter. The gain or loss is section 897 FIRPTA income. Under section 1445, UNF Corp must withhold and remit to the U.S. Treasury 30% of the sale proceeds even though the transaction produced a loss for Lord Peter.

Expert Answer:

Answer rating: 100% (QA)

10 The correct answer is Recognizing that ETB status depends on all the facts and circumstances the better view is that since Lord Peters facts most r... View the full answer

Related Book For

International Marketing And Export Management

ISBN: 9781292016924

8th Edition

Authors: Gerald Albaum , Alexander Josiassen , Edwin Duerr

Posted Date:

Students also viewed these law questions

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Googles ease of use and superior search results have propelled the search engine to its num- ber one status, ousting the early dominance of competitors such as WebCrawler and Infos- eek. Even later...

-

What (if anything) is wrong with each of the following statements? a. if (a > b) then c = 0; b. if a > b { c = 0; } c. if (a > b) c = 0; d. if (a > b) c = 0 else b = 0;

-

Does Under Armour have any resource strengths or competitive capabilities that qualify as a distinctive competence?

-

Draw the shear and moment diagrams for the beam (a) In terms of the parameters shown; (b) Set P = 800 lb, a = 5ft, I =12ft. P

-

Can a magnet have more than two magnetic poles, one north and one south?

-

Certain underlying considerations have had an important impact on the development of generally accepted accounting principles. Following is a list of these underlying considerations, as well as a...

-

19 20 Assertion A compass needle is placed near a current carrying wire. The deflection of the compass needle decreases when the magnitude of the current in the wire is increased. Reason The strength...

-

3.20 Apply nodal analysis to the circuit of Figure P3.20 to find the power dissipated by the 2-2 resistance. Check your result. 12 V AS69 ewgit + A-C@oala obuloni io li F maldo 3sqo E ort to sbia...

-

When might a patients favorite color or high school alma mater be considered health information?

-

How would the following monetary decisions of the European Central Bank influence individuals? a. A decrease in interest rates b. An asset purchase program to support struggling member-states c. A...

-

You believe that cooperation between the clinic receptionists and HIM staff would improve if phone responsibilities were more clearly defined. To whom would you assign the task of defining roles and...

-

The HIM staff tally information about the causes of complaints. What improvement tool would you use to prioritize the problems? Imagine you are the supervisor of the health information management...

-

After redesigning the process for investigating insurance denials, you want to monitor the effectiveness of your actions. What improvement tool would you use to determine whether the number of...

-

23.Describe the procedure of BP test and White test.

-

The area of square PQRS is 100 ft2, and A, B, C, and D are the midpoints of the sides. Find the area of square ABCD. B A

-

GG Farm Machinery Company is a French manufacturer of a specialized piece of machinery. Marcel Ger, the managing director of GG, was convinced there was a market in Australia for his machine and he...

-

Explain the meaning of the following statement: Managing multiculturalism within the international marketing organization and within the markets it serves is what makes international marketing...

-

Boeing, the Chicago-based aerospace giant, is known for its commercial aircraft. The 93- year-old company is the no. 2 manufacturer in the world of such planes, behind Blagnac, France-based Airbus....

-

You plan a survey to estimate the proportion of students on your campus who carry an iPad regularly. How many students should be in the sample if you want (with 95% confidence) a margin of error of...

-

A poll by Yankelovich Partners concluded that 61% of all households have a computer, with a margin of error of 3.5 percentage points. Approximately what sample size must have been used in this poll?

-

What is a hypothesis test?

Study smarter with the SolutionInn App